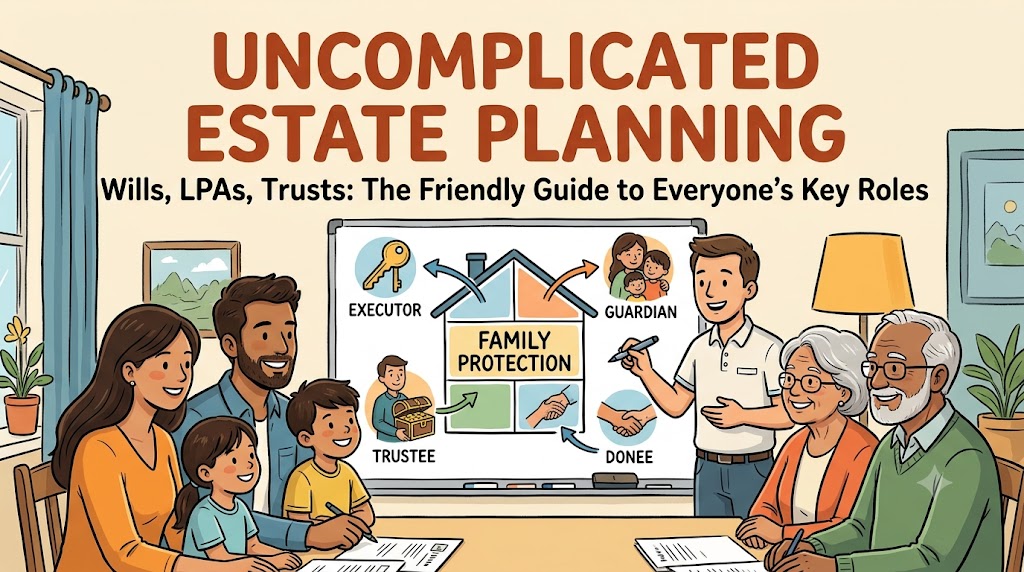

The Ultimate Guide to Estate Planning: Demystifying Wills, LPAs, and Trusts

Taking the first step toward estate planning is one of the most selfless acts of love you can perform for your family. It ensures your hard-earned assets are protected, your wishes are respected, and your loved ones are spared from administrative chaos and family disputes during an already painful time.

However, entering the world of estate planning can feel like trying to learn a foreign language. What is a “Donee”? Who needs a “Protector”? And what on earth does an “Estate Planner” actually do?

This educational guide breaks down the key appointments, roles, and critical considerations you need to know to secure your family’s future.

1. The Conductor: The Estate Planner

Before diving into the legal documents, you need an architect. Many people make the mistake of rushing to draft a Will without looking at the bigger picture. This is where an Estate Planner comes in.

- The Role: An Estate Planner is a professional who evaluates your entire financial and personal situation (assets, liabilities, insurance, family dynamics) to create a holistic legacy blueprint.

- What They Do: They facilitate tough family conversations, identify potential legal or tax vulnerabilities, and coordinate with lawyers and trust companies to ensure your plan is airtight.

- Key Consideration: Choose a qualified planner who looks at your estate holistically, rather than someone simply trying to sell a one-off financial product.

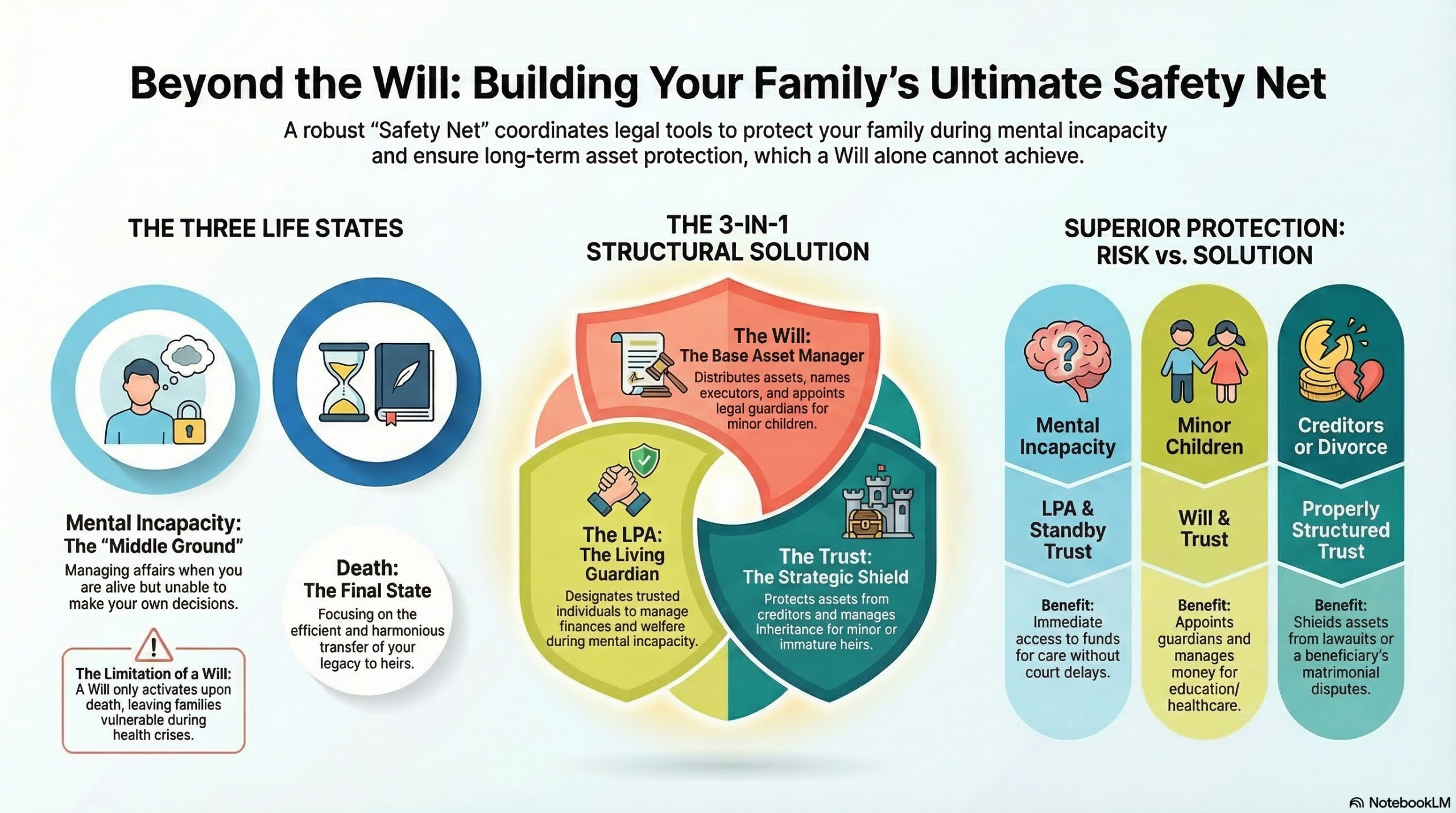

2. The Will: Managing Your Estate After Death

A Will is a legal document that dictates how your assets will be distributed and who will look after your minor children after you pass away. Without one, the state decides who gets what based on default laws.

Key Appointments to Know:

- Testator: This is you—the person making the Will and owning the assets.

- Executor: The person (or professional institution) you appoint to carry out the instructions in your Will. They locate your assets, pay off your debts, and distribute the remainder to your loved ones.

- Beneficiary: The individuals, family members, or charities chosen to receive your assets.

- Guardian: The person appointed to take legal custody of your children if they are minors when you pass away.

- Witness: Two independent individuals who must watch you sign the Will to make it legally valid.

Key Considerations:

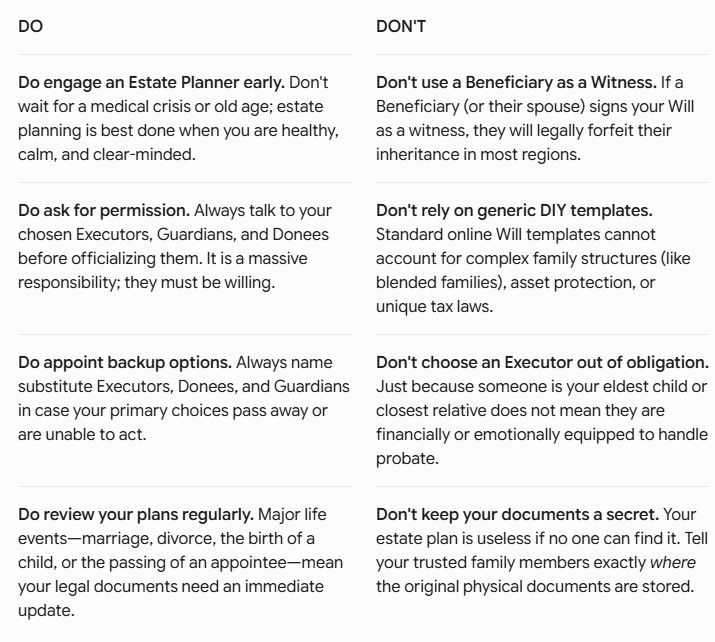

Choosing an Executor: This is a heavy administrative burden involving legal processes (probate). Choose someone who is highly organized, financially literate, and trustworthy. Always name a backup Executor.

Choosing a Guardian: Ensure your chosen guardian shares similar parenting values and lifestyle choices. Most importantly, ask them for permission before naming them in your Will.

3. The Lasting Power of Attorney (LPA): Protecting Your Lifetime Welfare

While a Will handles things after you die, an LPA protects you while you are alive but mentally incapacitated (e.g., due to advanced dementia, a severe stroke, or a coma).

Key Appointments to Know:

- Donor: This is you—the person giving away the decision-making power.

- Donee: The trusted person (or persons) you appoint to step into your shoes and make decisions on your behalf. Donees can manage two main areas:

- Personal Welfare: Making medical decisions, choosing nursing homes, and managing daily care.

- Property & Affairs: Managing your bank accounts, paying your bills, or selling your property to fund your medical needs.

- Replacement Donee: A backup person who steps in only if your primary Donee passes away or loses mental capacity themselves.

Key Considerations:

You can appoint multiple Donees to act “jointly” (they must agree unanimously on everything) or “jointly and severally” (they can make decisions independently). For urgent medical situations, “jointly and severally” is often preferred to prevent delays.

4. The Trust: Long-Term Control and Asset Protection

A Trust is a legal arrangement where you transfer assets to a third party to hold and manage for the benefit of your loved ones. It is highly effective for protecting spendthrift heirs, minor children, or preserving wealth across generations.

Key Appointments to Know:

- Settlor: This is you—the creator of the trust who funds it with assets.

- Trustee: The legal owner and manager of the trust assets. They must manage and distribute the funds strictly according to your “Letter of Wishes.”

- Beneficiary: The people who receive the financial benefits of the trust (e.g., receiving a monthly allowance for education or living expenses).

- Protector: An optional, independent “watchdog” who monitors the Trustee. They can be given the power to fire the Trustee or veto certain decisions to ensure your original intentions are honored.

- Investment Advisor: A financial professional appointed to manage the trust’s investment portfolio, ensuring the wealth grows over time.

Key Considerations:

If you have complex assets or major wealth to protect, appointing a Professional Trust Company as your Trustee is often safer than appointing a family member. It removes emotional bias and ensures professional competency.

5. Other Crucial Figures: Nominees

- Nominee: In many jurisdictions, assets like life insurance policies and government retirement accounts (such as CPF in Singapore or 401ks/IRAs in the US) cannot be distributed via a Will. You must explicitly name a Nominee directly with the respective institution to ensure the money goes to the right person.

Summary: The Ultimate Legacy “Do’s and Don’ts”

To kickstart your estate planning journey successfully, keep this essential checklist in mind:

Final Thoughts

Estate planning isn’t just for the ultra-wealthy—it is for anyone who wants to protect their family from unnecessary heartache, financial strain, and legal battles. Now that you know who the key players are, reach out to a professional Estate Planner to start drafting your family’s safety net today.

Kenny Loh is a distinguished Wealth Advisory Director (RNF# LKK300389588 Representing Financial Alliance) with a specialization in holistic investment planning and estate management. He excels in assisting clients to grow their investment capital and establish passive income streams for retirement. Kenny also facilitates tax-efficient portfolio transfers to beneficiaries, ensuring tax-efficient capital appreciation through risk mitigation approaches and optimized wealth transfer through strategic asset structuring.

In addition to his advisory role, Kenny is an esteemed SGX Academy trainer specializing in S-REIT investing and regularly shares his insights on MoneyFM 89.3. He holds the titles of Certified Estate & Legacy Planning Consultant and CERTIFIED FINANCIAL PLANNER (CFP).

With over a decade of experience in holistic estate planning, Kenny employs a unique “3-in-1 Will, LPA, and Standby Trust” solution to address clients’ social considerations, legal obligations, emotional needs, and family harmony. He holds double master’s degrees in Business Administration and Electrical Engineering, and is an Associate Estate Planning Practitioner (AEPP), a designation jointly awarded by The Society of Will Writers & Estate Planning Practitioners (SWWEPP) of the United Kingdom and Estate Planning Practitioner Limited (EPPL), the accreditation body for Asia.

Arrange for a non-obligatory one-to-one free consultation here!

You can join his Telegram channel #REITirement – SREIT Singapore REIT Market Update and Retirement related news. https://t.me/REITirement

If you need any financial advice, please contact kennyloh@fapl.sg