As we celebrate the Lunar New Year, I wanted to share a fun caricature that sums up my “why.” Many people ask how a Master’s in Electrical Engineering leads to a career in Wealth Advisory.

The answer is simple: I don’t just pick products; I engineer systems.

Just like the “REITs Engine” in this drawing, retirement shouldn’t be left to luck. It requires:

⚙️ Precision: Data-driven portfolio construction. 🛡️ Protection: An airtight 3-in-1 legacy plan (Will, LPA, Trust). 📸 Perspective: Remembering to capture the moments that matter most with the ones we love.

May your Year of the Horse be filled with steady yields, resilient legacies, and the “sleep well” factor!

If you’re looking to fine-tune your financial engine for 2026, let’s connect at:

With the opening of Singapore’s borders, and the expansion of the Vaccinated Travel Lane scheme to 11 countries, more Singaporeans are looking forward to travel. But comparing to the pre-pandemic era, there are many more considerations to take into account. The largest one being COVID-19 Travel Insurance Coverage. This article will discuss the many options available, and the many things to look out for.

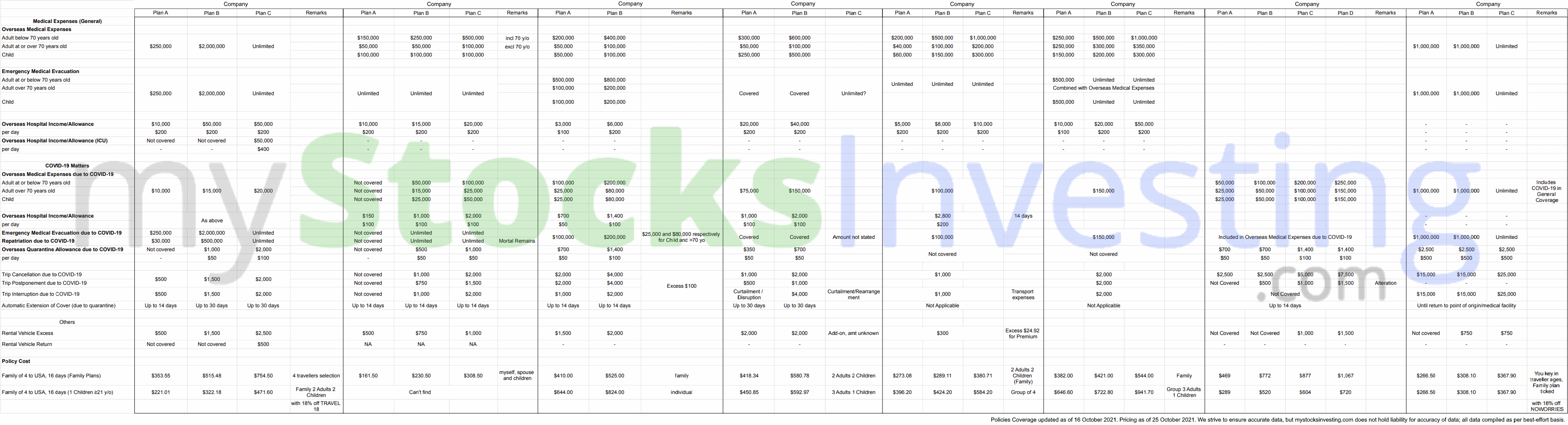

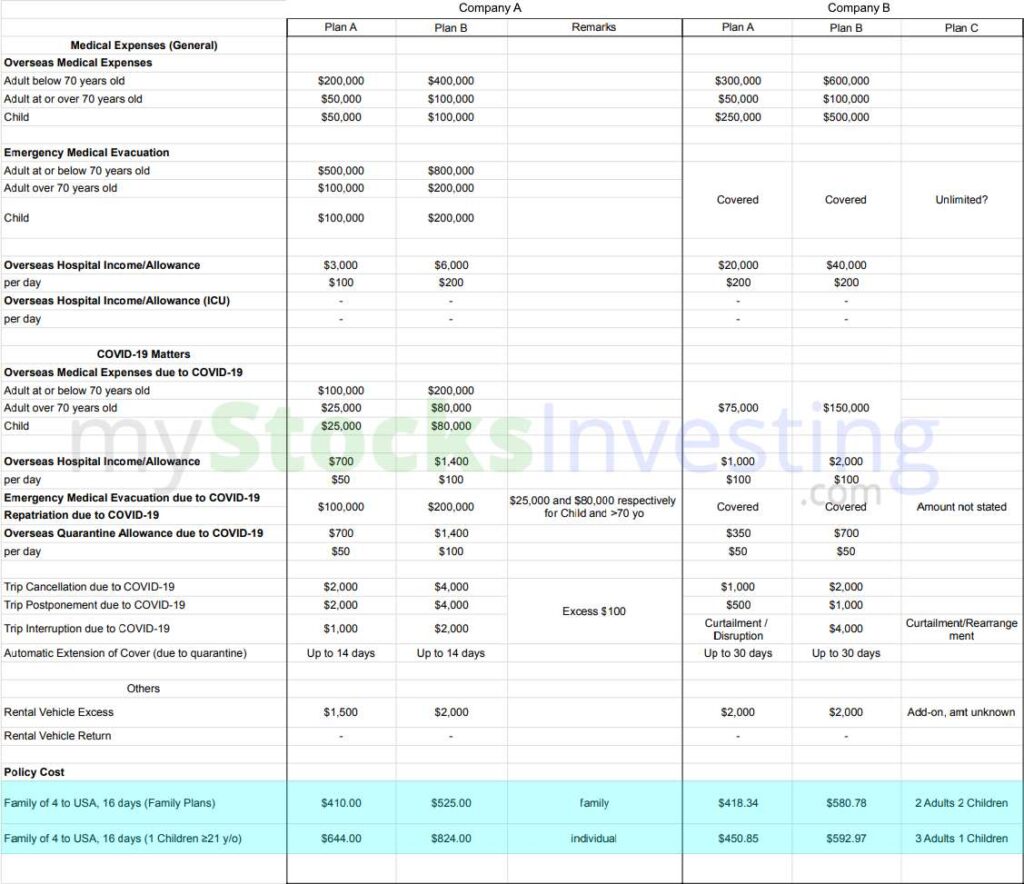

Overview of Plans: Table of Policies

The following table details the many plans on offer, from 8 different insurers. Only Travel Insurance policies that are offering plans with COVID-19 coverage are shown below.

An example of a Family of 4 planning a 16-day trip to the United States of America is shown below.

Travel Insurance policies, with COVID-19 coverage.

1. Some Travel Insurance policies DO NOT include COVID-19 coverage!

If you are looking for a travel insurance plan during this pandemic, take note of this! Below is an example of a travel insurance plan that does nothave COVID-19 coverage.

Some policies do not have COVID-19 coverage.

Meaning if you do get COVID-19 abroad, you will NOT be covered! Be sure to look at each policy in-depth, and read the fine print.

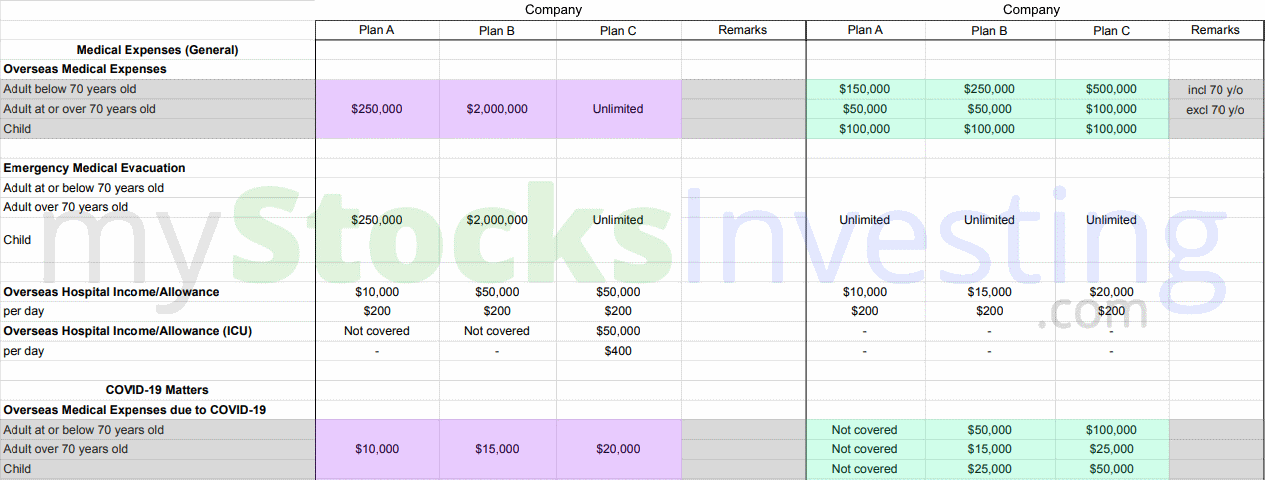

2. Overseas Medical Expenses Coverage ≠ COVID-19 Overseas Medical Expenses Coverage

Look closely at these 2 companies’ travel insurance policy. The following image will show that the coverage for non-COVID medical expenses and COVID-related medical expenses are vastly different.

Example of travel insurance policies of 2 companies, and their plans.

Let’s say you subscribe to Plan B in the first example. If you incur Overseas Medical Expenses due to COVID-19, instead of $2,000,000 in coverage, your coverage will only actually be $15,000. Is $15,000 coverage in Overseas Medical Expenses really enough?

In the second example, subscribing to Plan A will not cover you for any COVID-19 related medical expenses. This reinforces the first point where some policies do not include COVID-19 related medical expenses.

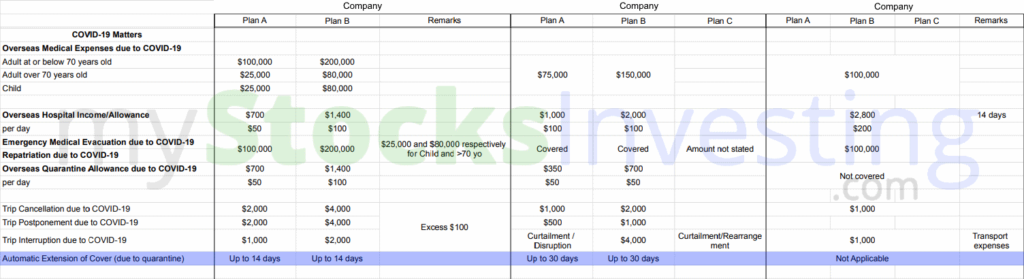

These differences in COVID-related and non-COVID related coverages also apply other aspects such as Emergency Medical Evacuation, Repatriation and Trip Cancellation.

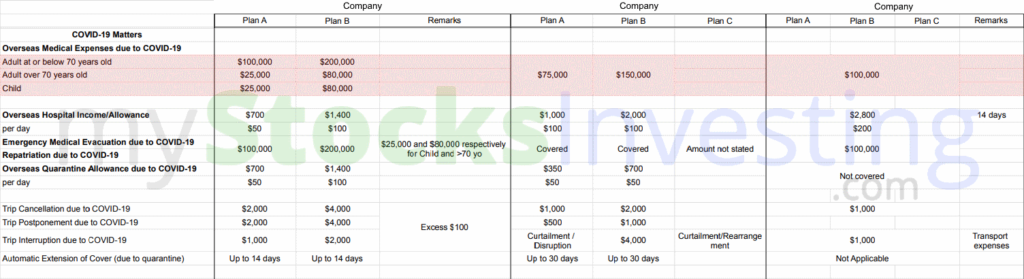

3. COVID-19 Medical Expenses Coverage can vary by age

Depending on your age, coverage for COVID-19 related Overseas Medical Expenses can vary from plan to plan. Differences are highlighted in red. In the example below, some policies offer lesser coverage for Children and/or Adults aged >70 then Adults aged <70 (Company A’s plans), while some offer the same coverage, regardless of age. (Company B and C’s plans) Ensure that the policy you choose to purchase suits your needs.

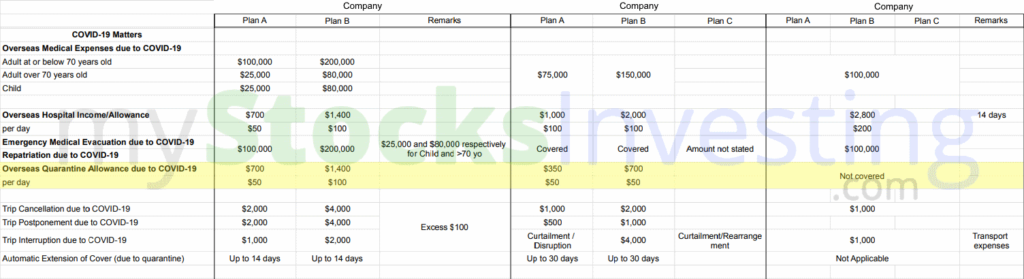

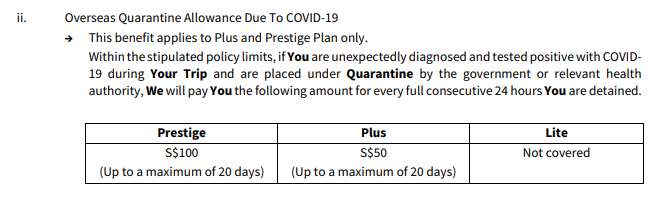

4. Does your policy include Overseas Quarantine Allowance?

You will not be allowed to travel back to Singapore for 14 days if you test positive on your pre-departure COVID-19 test.

The cost of quarantine isn’t small. For example, in the USA, one night of accomodation in Los Angeles can cost upwards of $200 per night per room/apartment. Multiply that by 14 days, and that will set you back more than $2,800.

Some travel insurance polices include Quarantine Allowance, while some do not!

Highlighted in yellow is the Quarantine Allowance due to COVID-19. First row shows total coverage, while the second row shows the coverage per day. Note that depending on the cost of accomodation in your chosen country, it may not cover the cost of quarantine completely. $100 per day can help soften the blow to your finances should you be subject to overseas quarantine.

If you subscribe to the third insurer’s plan in this example, you will not have any COVID-19 quarantine allowance should you be subject to quarantine and isolation overseas! Be sure to check if your policy will cushion the financial repurcussions of testing positive for COVID-19 overseas.

5. How many days will your policy cover for Overseas Quarantine?

Most policies offer Automatic Extension of Cover, due to quarantine. Do read the policies in detail! Different companies offer different lengths of automatic extension. For example, this is a snapshot of a policy taken from one of the plans. This policy offers up to 20 days of coverage due to overseas quarantine. Meaning if you have to quarantine >20 days due to COVID-19, you won”t be covered after 20 days.

This policy offers up to 20 days of coverage due to overseas quarantine.

Below is a comparison table of the number of days each policy covers for quarantine length. One good way to check if your policy’s maximum quarantine allowance length is enough, is to check your chosen countries’ health advisories’ COVID-19 quarantine/isolation length.

Comparison of Automatic Extension of Cover (in days)

Different policies offer different additional lengths of quarantine coverage. (See highlight in blue) Do look through each policy to see if it fits your needs.

6. Will your policy cover cancellation/postponement/interruption of your trip due to COVID-19 related issues?

Border closures? Sudden VTL cancellation? Ensure that your policy covers these events. The last thing you want is any of these events happening, and not being able to get back your money.

Comparison of Trip Cancellation/Postponement/Interruption coverage due to COVID-19 related issues

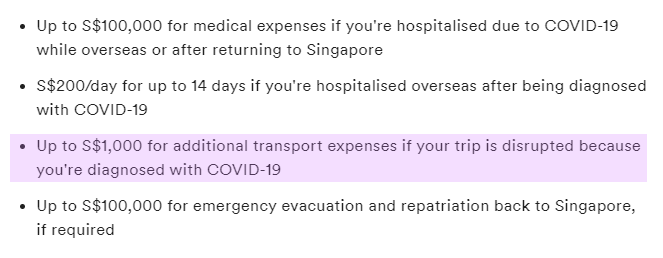

Highlighted in green are the trip cancellation/postponement/interruption policy differences. Do study each policy differently, as each policy’s fine print is different. For example, Company C’s Trip Interruption has coverage for $1,000 in additional transport expenses. (Highlighted in purple)

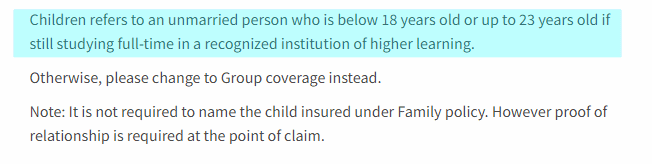

7. (For families) Check whether your child is actually a child!

According to the insurer, is your child really a child? In a sense, this depends from insurer to insurer. If your child does not fit the criteria of being a child, use the “group” option while purchasing your insurance plan, not the families option. This is to prevent complications, in case you need to perform a claim. Which in the COVID-19 era, is more common due to the possbility of getting quarantined overseas.

An example of an insurer’s definition of children

Some insurers charge about the same, regardless of whether you select the “group” option (if your child does not fit the definition of a child) or the “family” option. Some insurers charge a lot more, simply because your child is one year too old (e.g 22 years old instead of 21).

If your child is between the ages of 18-25, depending on the insurer, one might classify them as a child while another might not. Be sure to compare insurance plans according to the insurer’s definition of your children.

Highlighted in blue is an example. Policy costs alone, Company B does not charge you a lot more if you select a “group” plan instead of a “family” plan. Company A’s family plans are more affordable as a family, but if your child is not a child (according to definition), the price is increased by a considerable amount.

Kenny Loh is a Senior Financial Advisory Manager and REITs Specialist of Singapore’s top Independent Financial Advisor. He helps clients construct diversified portfolios consisting of different asset classes from REITs, Equities, Bonds, ETFs, Unit Trusts, Private Equity, Alternative Investments, Digital Assets and Fixed Maturity Funds to achieve an optimal risk adjusted return. Kenny is also a CERTIFIED FINANCIAL PLANNER, SGX Academy REIT Trainer, Certified IBF Trainer of Associate REIT Investment Advisor (ARIA) and also invited speaker of REITs Symposium and Invest Fair. You can join my Telegram channel #REITirement – SREIT Singapore REIT Market Update and Retirement related news. https://t.me/REITirement

One must have a certain amount of grit, willpower, and determination to adapt if they work in the insurance industry today. In the past decade alone, insurance carriers have been extra challenged to align their legacy values and systems with extremely modern consumer sensibilities. In the wake of the health-related and socioeconomic impact of the COVID-19 pandemic, customers’ attitudes about life and annuity insurance have also changed. They may be more cautious about enrolling in insurance programs than members of the previous generation were. If they do sign up for either insurance or annuity, they seek higher standards of service and engagement than what was once asked from carriers.

A question worth asking yourselves is this: do you want your insurance brand to keep succeeding in the long haul? If your answer is a resounding yes, then the first move that you should make towards securing your future is pursuing life insurance innovation. The time is ripe for you to revisit your life and annuity policy administration system and optimize it for the delivery of digital insurance services. Here are four advantages of exploring new technologies, like a cloud-based life insurance platform, and leveraging them to meet the insurance challenges of the future.

You’ll Equip Your Company to Do Business in the New Insurance Landscape

The first thing you should know about delivering life and annuity products in this era is that your customers value technological prowess in their carriers. The new insurance landscape is one in which many carriers have invested resources into digital insurance delivery. Do you want to be left behind by your peers, or do you want to remain the carrier of choice?

It’s in your best interest to find a platform that can cushion you from the initial stresses of modernization and prepare you for further innovation. There will also be less of a need to keep adapting and re-adapting processes from your legacy system if you choose to optimize now.

You’ll Reduce Your Steep Operating and Compliance-Related Costs

Another strong argument for optimizing your current life insurance system for digital delivery is the amount of money you’ll save from operations. With a new platform, your operations won’t be as dependent on work done in business headquarters. Since vital insurance data will be on the cloud, that technically means that you can operate your business from anywhere. It also means that you won’t lose money from the threat of service interruption, even if you aren’t at HQ.

Modernizing your insurance system will also optimize processes like underwriting. You’ll spend even less time and labor arriving at the correct policy prices for your customers. You may also end up having a better grip over your compliance since it will be easy to manage huge swathes of compliance-related data. Ultimately, you will worry less about paying steep penalties for gaps in your compliance and stay in the good graces of your regulators.

You’ll Synergize with Other Partners in the Delivery of Your Insurance Products

It isn’t only insurers who feel the pressure to innovate. The same goes for other parties in the life insurance and annuity provider network, such as hospitals and clinics that accept health insurance. These institutions are doing their part to modernize their services for your shared clientele. Doing the same will enhance your synergy with them in rolling out your insurance program.

There are several specific advantages to getting on the same page, tech-wise, as your partners in the provider network. An optimized system can help you smoothly advertise and implement bancassurance products with a partner bank. You may also be able to use information technology, like APIs or application programming interfaces, to link up with a healthcare provider’s patient portal. Because of that linkage, it may be easier for your patients to cover their healthcare expenses through your policy online. The possibilities are extremely promising and, most importantly, extremely helpful to your clients.

Your Brand Will Resonate with a New Generation of Policyholders

If you’re looking for a way to reinvent your insurance business as the ideal partner for a new generation of policyholders, optimization is the answer. Optimizing your system gives you the chance to develop new insurance products or rework old ones in a fraction of the time it took before. That means that you may be able to simplify or unbundle all-in-one insurance programs and manage piecemeal policies instead. You may also consider offering the insurance product catalog as a service on its own and launching it through a digital campaign.

Actions like these will attract the attention of a new breed of policyholders, many of whom are tech-savvy millennials who value experiences and investments. You can make insurance look less intimidating than it did for their parents’ generation while also presenting it as something worth spending on given current times. If your brand can resonate with this demographic of policyholders, much of the battle to stay relevant will have been won.

Conclusion

The economy that drives the insurance system may not let up anytime soon, but carriers can choose to be tough, smart, and resilient regardless. The insurance business that stays ahead of the times has the best chances of living on and serving hopeful new generations. If you take the steps to optimize your life insurance system for the current landscape of the industry, you won’t regret it. Explore your options and upgrade to a system that can serve your current and future needs!