Money and Me: Which Billion-Dollar REIT Bets Will Pay Off?

Segment 1: Industrial REITs (Questions 1–3)

Q1: Industrial REITs have once again been highlighted as one of the more resilient sectors. What continues to set them apart from office and retail REITs today?

• “While retail relies on consumer footfall and office adapts to flexible work, industrial REITs are the backbone of the structural economy—e-commerce, advanced manufacturing, and supply chains. You can delay a shopping trip or work from home, but a logistics hub or a data center cannot be replicated virtually.”

• They benefit from longer leases (longer WALE) and sticky tenants who invest heavy capital into fitting out the spaces (like cleanrooms or cold-chain logistics), making it highly disruptive for them to move.

Q2: Many industrial REITs have been actively rejuvenating their portfolios. What does that involve, and why is it important for long-term returns?

• “Portfolio rejuvenation is basically real estate asset surgery. It means selling off old, single-user factories that have low ceiling heights and poor floor loading, and using that cash to build or buy modern, multi-story ramp-up logistics hubs or high-spec facilities.”• It is vital because industrial land in Singapore has shorter lease tenures (often 30 years). If a manager sits on an aging asset, its value decays to zero. By redeveloping or recycling, they boost the net property income (NPI) yield and defend the long-term Net Asset Value (NAV) of the REIT.

Q3: Which segments within industrial real estate are seeing the strongest opportunities today – traditional factories, logistics, data centres or business parks?

• “Logistics and AI-ready data centers are running away with the trophy right now. Traditional factories face cost pressures, and business parks are seeing a bit of supply overhang, but modern logistics facilities near our ports are enjoying near-full occupancy and very strong positive rental reversions.”

Segment 2: OUE REIT & Crowne Plaza Divestment (Questions 4–6)

Q4: Selling a well-known asset can sometimes surprise investors. How do you decide whether a divestment is creating value rather than shrinking the portfolio?

• “Investors often fall into the trap of thinking ‘bigger is always better.’ It’s not. You measure value creation by looking at capital efficiency. If a manager sells an asset at a premium to valuation, uses the cash to lower high leverage, and avoids huge upcoming repair costs, that is value creation—even if the total portfolio size shrinks temporarily.”

• Crowne Plaza’s master lease expires by 2028. OUE REIT is essentially selling the asset before they have to shell out massive capital expenditures (CapEx) for a major hotel refurbishment. They passed that future bill to the buyer.

Q5: This transaction includes a special distribution for unitholders. Beyond the immediate payout, what should investors really be looking at when assessing a deal like this?

• “Don’t just look at the short-term ‘sugar rush’ of a special payout. Look at the permanent structural repair of the balance sheet. In OUE REIT’s case, their aggregate leverage drops beautifully from a tight 41.5% down to a very comfortable 36.6%. That gives them the debt headroom to hunt for better, higher-yielding assets later.”

Q6: More broadly, do you think we’ll see more REIT managers recycling mature assets over the next year instead of simply pursuing new acquisitions?

• “Absolutely. The era of ‘cheap debt-funded buying’ is over. With interest rates staying higher for longer, the best way for a REIT to grow without diluting investors via massive rights issues is capital recycling—selling the old to fund the new.”

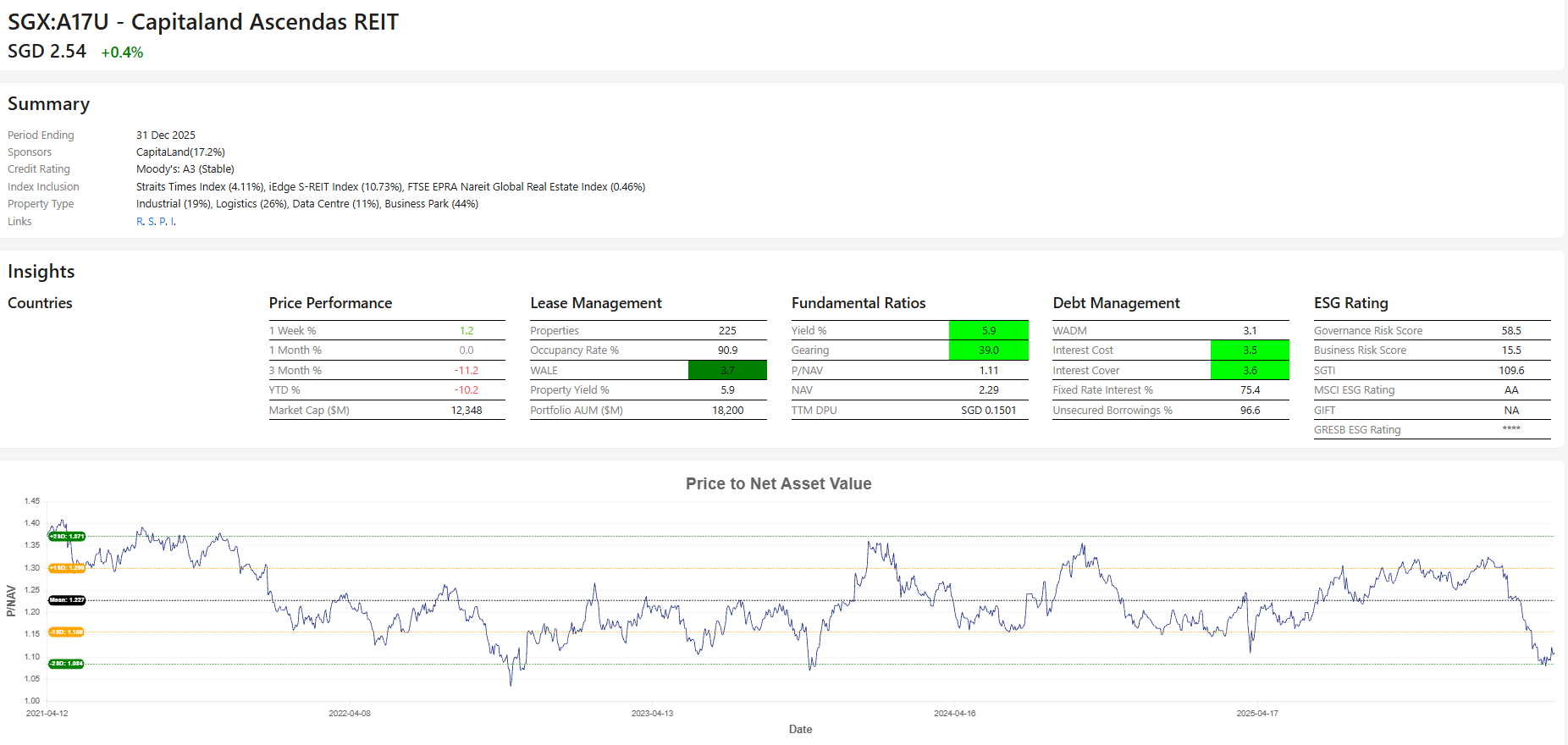

Segment 3: CapitaLand Ascendas REIT (CLAR) Tuas Acquisition (Questions 7–9)

Q7: CapitaLand Ascendas REIT says this acquisition will enhance distributions while strengthening its logistics exposure. What stands out to you about this deal?

• “Three things stand out: Location, Specifications, and Certainty. It’s a modern 2021 ramp-up facility right next to the upcoming Tuas Mega Port. It comes 100% occupied with a 5-year lease and a built-in 2% annual rent escalation. It is an immediate cash-flow generator.”

Q8: When REIT managers describe an acquisition as “DPU-accretive”, what questions should investors ask before taking that at face value?

• “Investors must ask: ‘Is it accretive because of real property performance, or is it just financial engineering?'”•

Key Questions to Highlight:

1. What is the funding mix? Are they taking on cheap short-term debt that will reset at higher rates later?2. Is the Net Property Income (NPI) yield higher than the cost of funding? (For CLAR, the 6.5% NPI yield comfortably beats their funding costs, making it genuinely accretive).

Q9: With logistics assets remaining in demand, are valuations becoming stretched, or do you still see attractive opportunities in this space?

• “Valuations are tight, but they are justified by the scarcity of prime land. In Singapore, you can’t just build another logistics hub anywhere. The demand from multinational companies wanting to anchor themselves in Singapore ensures that while you pay a premium, the defensive nature of the income is worth it.”

Segment 4: CICT’s S$3.9 Billion Paragon Acquisition (Questions 10–12)

Q10: This is one of the biggest REIT transactions we’ve seen this year. What was your first reaction when the deal was announced?

• “My first thought was: ‘Wow, this is a massive, bold chess move.’ Swapping Asia Square Tower 2 for Paragon is Asia’s largest REIT showing everyone how to pivot out of a stabilised office asset into a flagship, freehold retail asset with a massive medical tourism tailwind.”

Q11: CICT is effectively selling one major asset and buying another. What should investors focus on when deciding whether this is a smart capital allocation move?

• “Focus on the yield spread and the land tenure. They sold an asset yielding around 3% (Asia Square Tower 2) and bought an asset yielding 3.9% (Paragon). That’s an immediate yield pickup. Furthermore, they are unlocking the freehold value of Paragon, which gives the REIT generational resilience.”

• Also point out the “secret weapon” of Paragon—the medical center next to Mount Elizabeth. It’s not just fashion retail; it’s a defensive healthcare play.

Q12: Looking beyond this transaction, do you think we’re entering a period where successful REITs will be defined less by interest rates and more by management’s ability to buy, sell and recycle assets effectively?

• “100%. We are moving from a macro-driven REIT market to a manager-driven REIT market. When interest rates were 1%, any manager could look smart just by buying properties. Today, the winners will be defined by their surgical skill in asset management—knowing exactly when to harvest value from an old asset and where to plant the capital for tomorrow’s growth.”

Kenny Loh is a distinguished Wealth Advisory Director (RNF# LKK300389588 Representing Financial Alliance) with a specialization in holistic investment planning and estate management. He excels in assisting clients to grow their investment capital and establish passive income streams for retirement. Kenny also facilitates tax-efficient portfolio transfers to beneficiaries, ensuring tax-efficient capital appreciation through risk mitigation approaches and optimized wealth transfer through strategic asset structuring.

In addition to his advisory role, Kenny is an esteemed SGX Academy trainer specializing in S-REIT investing and regularly shares his insights on MoneyFM 89.3. He holds the titles of Certified Estate & Legacy Planning Consultant and CERTIFIED FINANCIAL PLANNER (CFP).

With over a decade of experience in holistic estate planning, Kenny employs a unique “3-in-1 Will, LPA, and Standby Trust” solution to address clients’ social considerations, legal obligations, emotional needs, and family harmony. He holds double master’s degrees in Business Administration and Electrical Engineering, and is an Associate Estate Planning Practitioner (AEPP), a designation jointly awarded by The Society of Will Writers & Estate Planning Practitioners (SWWEPP) of the United Kingdom and Estate Planning Practitioner Limited (EPPL), the accreditation body for Asia.

Arrange for a non-obligatory one-to-one free consultation here!

You can join his Telegram channel #REITirement – SREIT Singapore REIT Market Update and Retirement related news. https://t.me/REITirement

If you need any financial advice, please contact kennyloh@fapl.sg

2026

- Money and Me: Should you use your CPF to buy a newly included REIT? (June 2026)

- Money and Me: REIT Opportunity & the Mid-Cap Alpha Hunt (April 2026)

- Money and Me: Is Headline DPU Hiding the Truth About Your REIT? (March 2026)

2025

- Money and Me: Are S-REITs Still Worth the Climb? (October 2025)

- Money and Me: S-REITs vs Banks – Is It Time to Rotate? (August 2025)

- Money and Me: Are S-REITs Still Worth the Risk in 2025? (July 2025)

- Money and Me: REITs Among Upcoming IPO’s and what you need to know (June 2025)

- Money and Me: S-REITs Bounce Back? China’s REIT Game-Changer and the hunt for yield of up to 8% (May 2025)

- Money and Me: How are S-REIT’s doing amidst the Tariffs Turnaround? (April 2025)

- 𝗠𝗼𝗻𝗲𝘆 𝗮𝗻𝗱 𝗠𝗲: 𝗦-𝗥𝗘𝗜𝗧𝘀 𝗥𝗮𝗹𝗹𝘆, 𝗧𝗿𝗲𝗮𝘀𝘂𝗿𝘆 𝗬𝗶𝗲𝗹𝗱𝘀 𝗗𝗿𝗼𝗽, 𝗮𝗻𝗱 𝗖𝗗𝗟’𝘀 𝗙𝗮𝗺𝗶𝗹𝘆 𝗗𝗿𝗮𝗺𝗮 (March 2025)

- Money and Me: CPF Special Account Closure, Retirement Planning, and Investment Strategies with Kenny Loh (February 2025)

- Money and Me: What is your T-Bill to S-REIT allocation? (January 2025)

2024

- Money and Me: Trump’s Second Term, Bitcoin, Tesla, AI, and Suntec REIT Mandatory Cash Offer (December 2024)

- Money and Me: Data Centered S-REITs; here is what you need to know (November 2024)

- Money and Me: Finding attractive S-REITs in a rate cutting environment (October 2024)

- Money and Me: What’s behind the S-REIT Rally? Fed Rate Cuts, and should Finfluencers be managed? (September 2024)

- Money and Me: Navigating S-REITs Amid Earnings Season and Potential US Rate Cuts (August 2024)

- Money and Me: Navigating Challenges for Mapletree REITs and REITs related to Changi Business Park

(June 2024) - Money and Me: Winners and Losers Among S-REITs, Frasers Property’s Profit Plunge, and the Impact of Sustained High Interest Rates (May 2024)

- Money and Me: Manulife US REIT where could it be heading? Are we at the tail end of the down cycle for S-Reits? (April 2024)

- Money and Me: Will more S-REIT’s suspend distributions? (March 2024)

- Money and Me: US Office Reits – the immediate outlook is bleak but there are opportunities for investors (February 2024)

- Money and Me: Why S-REIT investors are focused on valuations in 2024? (January 2024)

2023

- Money and Me: Can Manulife US REIT be saved? (December 2023)

- Money and Me: Finding bargains in the S-REITs sector today (November 2023)

- Money and Me: How a contrarian investor reads a sell-off (October 2023)

- Money and Me: Finding bargains in the S-REITs sector today (September 2023)

- Money and Me: S-REITs earning stars and landscape quakes (August 2023)

- Money and Me: 3 Singapore REITs to watch (July 2023)

- Money and Me: Are S-REITs in for a promising 2H2023? (June 2023)

- Money and Me: How might the expectations of an impending recession affect S-REITs? (May 2023)

- Money and Me: S-REITs’ 2023 1st quarter report card review (April 2023)

- Money and Me: S-REITs that will hold up well in an increasing interest rate environment (March 2023)

- Money and Me: Winners and losers of latest S-REITs earnings season (February 2023)

- Money and Me: S-REITs’ 2023 outlook (January 2023)

2022

- Money & Me: Is 2023 the year of recovery for S-REITs? (December 2022)

- Money & Me: What happens after the recent S-REIT crash? (November 2022)

- Money & Me: Further Interest Rate Hikes, FHT’s failed Privatization bid (September 2022)

- Money & Me: Q3 2022 SREIT winners (August 2022)

- Money and Me: REIT picking in an inflationary environment (July 2022)

- Money and Me: Are Hospitality REITs the clear way to play the reopening trade in Singapore? (June 2022)

- Money and Me: Can S-REITs maintain its upswing from Q1? (May 2022)

- Money & Me: The case for being bullish on S-REITs amid the Ukraine crisis (March 2022)

- Money & Me: Optimism for S-REIT’s given earnings signals and mapping the possibilities for shareholders in the Mapletree merger (February 2022)

- Money & Me: Mapletree merger, growth in commercial S-Reits and the potential return of Reit IPOs in 2022 (January 2022)

2021

- Money & Me: First Reit, CapitaLand, Daiwa, Digital Core Reit and the best of the S-Reit pivots (December 2021)

- Money and Me: VTL’s and hospitality and retail, a new Reit ETF and Making sense of offers for SPH (November 2021)

- Money and Me: Who benefits from the ESR – ARA Logos Logistics Trust merger? (October 2021)

- Money and Me: China’s Evergrande Group property and the spillover in the property market, breaking down what CapitaLand Invest means for the investor and global REITs to watch (September 2021)

- Money and Me: Are retail and hospitality aggressive plays given the pace of reopening? (August 2021)

- Money and Me: Which REITs have seen a limited impact on occupancy during COVID? (July 2021)

- Money and Me: An overview of the REIT performance (June 2021)

- Money and Me: S-REIT’s: which are most likely and which least likely to be affected by new social restrictions? (May 2021)

- Money and Me: What’s the link between bond yields and S-REITs? (April 2021)

2020

- Money and Me: REITS that did well in 2020 (December 2020)

- Money and Me: An overview of S-REITS, value rotations and REITS paying out higher dividends (November 2020)

- Money and Me: Yield Generating Asset Classes (October 2020)

- Money and Me: The REIT outlook within and beyond Singapore (August 2020)

- Money and Me: Ugly Duckling Earnings turning into Beautiful S- Reit swans? (July 2020)

- Money and Me: V for S-REITs? (June 2020)

- Money and Me: Will revenge spending help REITs? (May 2020)

- Money and Me: What REITs to Look out for? (April 2020)

- Money and Me: Crazy REIT Sales (March 2020)