With the opening of Singapore’s borders, and the expansion of the Vaccinated Travel Lane scheme to 11 countries, more Singaporeans are looking forward to travel. But comparing to the pre-pandemic era, there are many more considerations to take into account. The largest one being COVID-19 Travel Insurance Coverage. This article will discuss the many options available, and the many things to look out for.

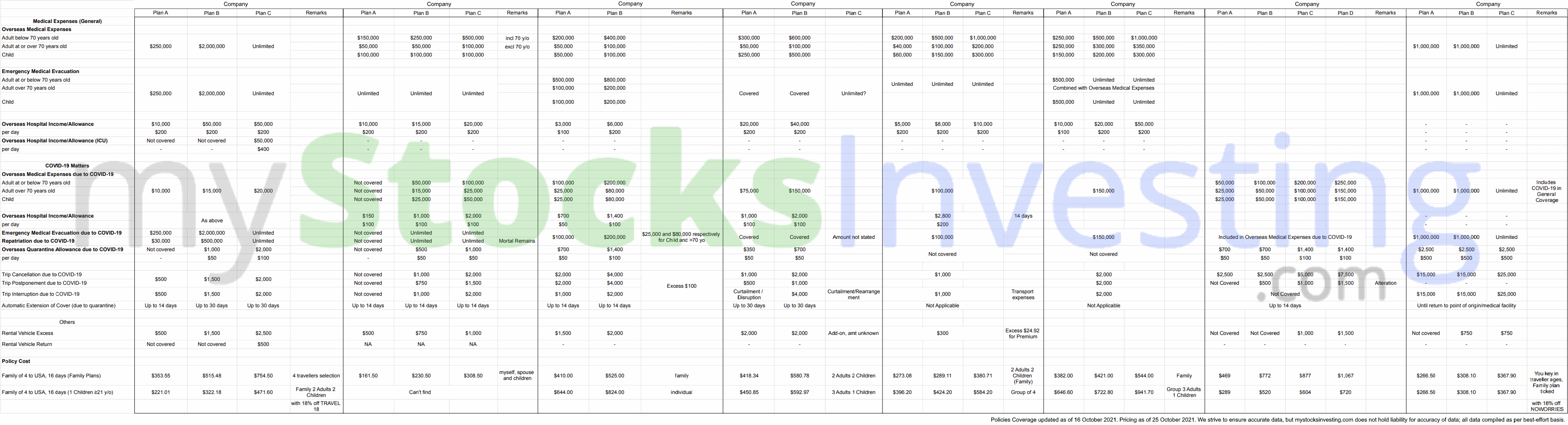

Overview of Plans: Table of Policies

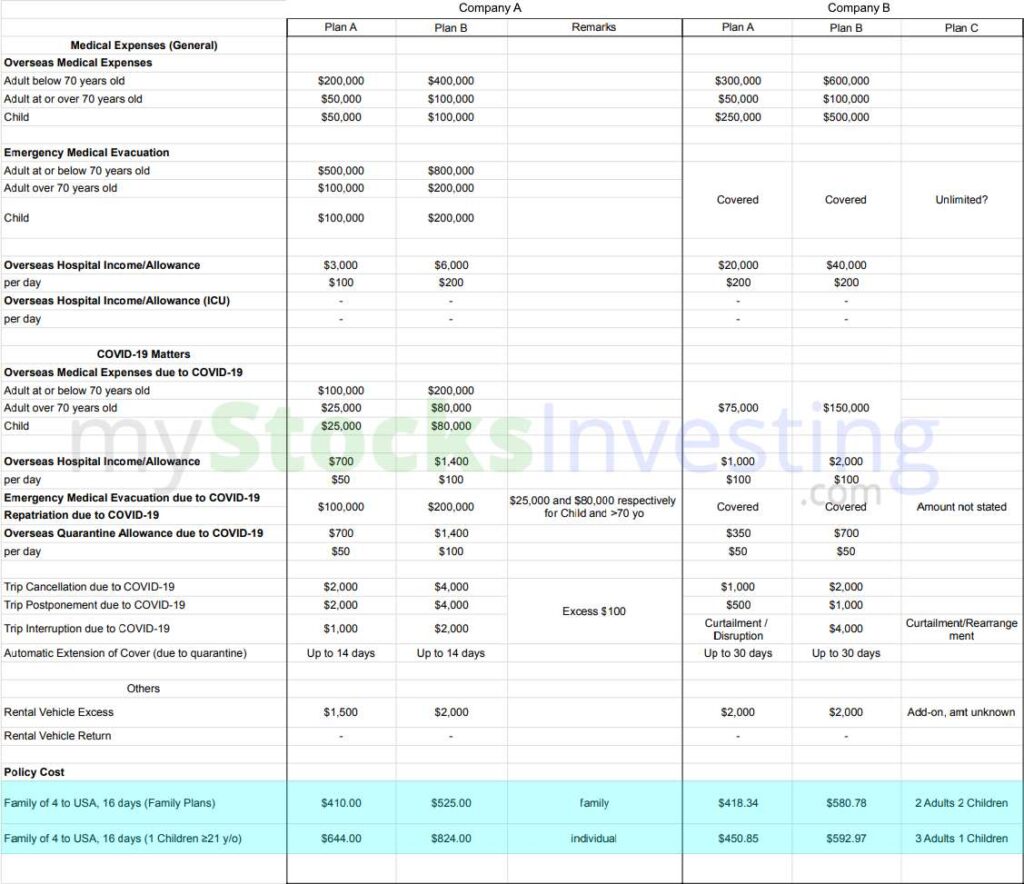

The following table details the many plans on offer, from 8 different insurers. Only Travel Insurance policies that are offering plans with COVID-19 coverage are shown below.

An example of a Family of 4 planning a 16-day trip to the United States of America is shown below.

This comparison table includes each travel insurance policy for 8 different insurance companies. There are significant differences between them, so you should keep a look out for them. If you are really unsure on which would be the best single trip insurance during this era of COVID-19 travel, do look for me to discuss on which plan suits you and your family the best.

1. Some Travel Insurance policies DO NOT include COVID-19 coverage!

If you are looking for a travel insurance plan during this pandemic, take note of this! Below is an example of a travel insurance plan that does not have COVID-19 coverage.

Meaning if you do get COVID-19 abroad, you will NOT be covered! Be sure to look at each policy in-depth, and read the fine print.

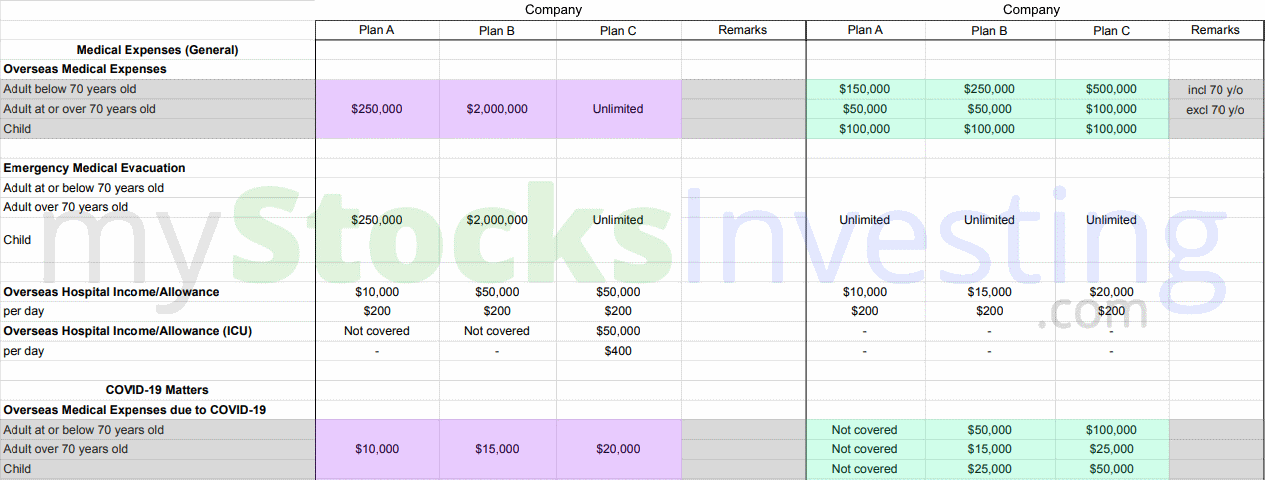

2. Overseas Medical Expenses Coverage ≠ COVID-19 Overseas Medical Expenses Coverage

Look closely at these 2 companies’ travel insurance policy. The following image will show that the coverage for non-COVID medical expenses and COVID-related medical expenses are vastly different.

Let’s say you subscribe to Plan B in the first example. If you incur Overseas Medical Expenses due to COVID-19, instead of $2,000,000 in coverage, your coverage will only actually be $15,000. Is $15,000 coverage in Overseas Medical Expenses really enough?

In the second example, subscribing to Plan A will not cover you for any COVID-19 related medical expenses. This reinforces the first point where some policies do not include COVID-19 related medical expenses.

These differences in COVID-related and non-COVID related coverages also apply other aspects such as Emergency Medical Evacuation, Repatriation and Trip Cancellation.

3. COVID-19 Medical Expenses Coverage can vary by age

Depending on your age, coverage for COVID-19 related Overseas Medical Expenses can vary from plan to plan. Differences are highlighted in red. In the example below, some policies offer lesser coverage for Children and/or Adults aged >70 then Adults aged <70 (Company A’s plans), while some offer the same coverage, regardless of age. (Company B and C’s plans) Ensure that the policy you choose to purchase suits your needs.

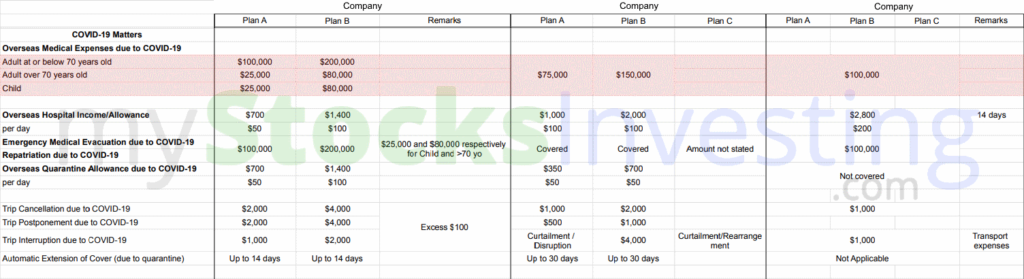

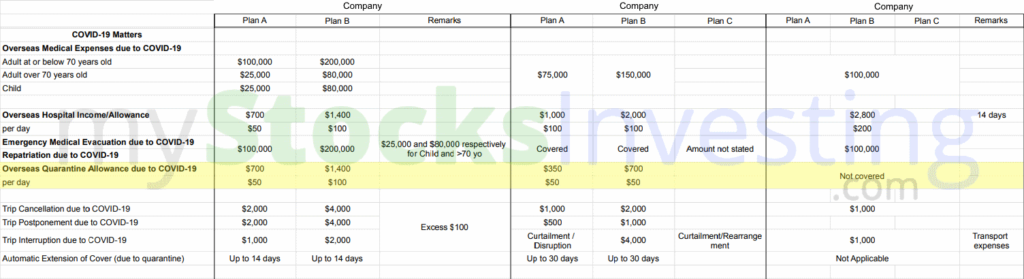

4. Does your policy include Overseas Quarantine Allowance?

If you test positive for COVID-19 prior to your departure for your return flight, chances are you will not be allowed to board the flight back to Singapore. (Highlighted in yellow below) In that case, you will be subject to overseas quarantine, whether it be at a hospital, a government facility, or remaining at your place of residence. For example, in the United States, you are to isolate for at least 10 days.

The cost of quarantine isn’t small. For example, in the USA, one night of accomodation in Los Angeles can cost upwards of $200 per night per room/apartment. Multiply that by 14 days, and that will set you back more than $2,800.

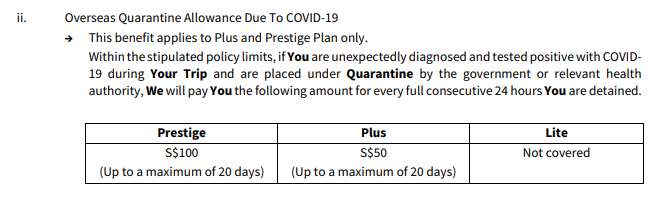

Highlighted in yellow is the Quarantine Allowance due to COVID-19. First row shows total coverage, while the second row shows the coverage per day. Note that depending on the cost of accomodation in your chosen country, it may not cover the cost of quarantine completely. $100 per day can help soften the blow to your finances should you be subject to overseas quarantine.

If you subscribe to the third insurer’s plan in this example, you will not have any COVID-19 quarantine allowance should you be subject to quarantine and isolation overseas! Be sure to check if your policy will cushion the financial repurcussions of testing positive for COVID-19 overseas.

5. How many days will your policy cover for Overseas Quarantine?

Most policies offer Automatic Extension of Cover, due to quarantine. Do read the policies in detail! Different companies offer different lengths of automatic extension. For example, this is a snapshot of a policy taken from one of the plans. This policy offers up to 20 days of coverage due to overseas quarantine. Meaning if you have to quarantine >20 days due to COVID-19, you won”t be covered after 20 days.

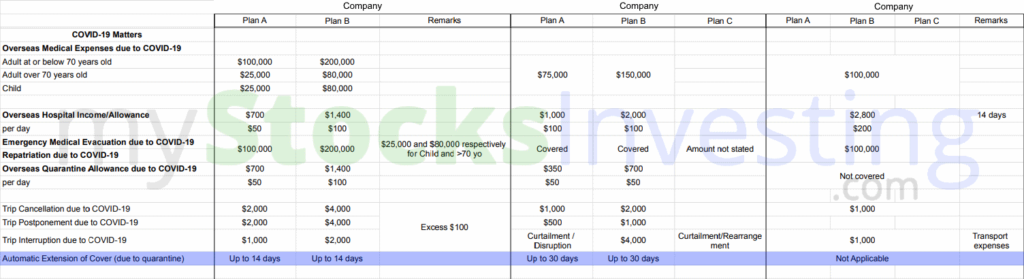

Below is a comparison table of the number of days each policy covers for quarantine length. One good way to check if your policy’s maximum quarantine allowance length is enough, is to check your chosen countries’ health advisories’ COVID-19 quarantine/isolation length.

Different policies offer different additional lengths of quarantine coverage. (See highlight in blue) Do look through each policy to see if it fits your needs.

6. Will your policy cover cancellation/postponement/interruption of your trip due to COVID-19 related issues?

Border closures? Sudden VTL cancellation? Ensure that your policy covers these events. The last thing you want is any of these events happening, and not being able to get back your money.

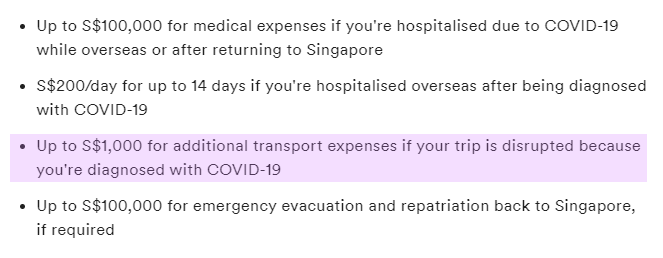

Highlighted in green are the trip cancellation/postponement/interruption policy differences. Do study each policy differently, as each policy’s fine print is different. For example, Company C’s Trip Interruption has coverage for $1,000 in additional transport expenses. (Highlighted in purple)

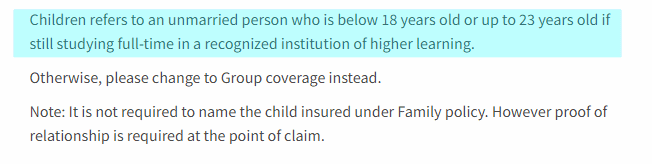

7. (For families) Check whether your child is actually a child!

According to the insurer, is your child really a child? In a sense, this depends from insurer to insurer. If your child does not fit the criteria of being a child, use the “group” option while purchasing your insurance plan, not the families option. This is to prevent complications, in case you need to perform a claim. Which in the COVID-19 era, is more common due to the possbility of getting quarantined overseas.

Some insurers charge about the same, regardless of whether you select the “group” option (if your child does not fit the definition of a child) or the “family” option. Some insurers charge a lot more, simply because your child is one year too old (e.g 22 years old instead of 21).

If your child is between the ages of 18-25, depending on the insurer, one might classify them as a child while another might not. Be sure to compare insurance plans according to the insurer’s definition of your children.

Highlighted in blue is an example. Policy costs alone, Company B does not charge you a lot more if you select a “group” plan instead of a “family” plan. Company A’s family plans are more affordable as a family, but if your child is not a child (according to definition), the price is increased by a considerable amount.

Kenny Loh is a Senior Financial Advisory Manager and REITs Specialist of Singapore’s top Independent Financial Advisor. He helps clients construct diversified portfolios consisting of different asset classes from REITs, Equities, Bonds, ETFs, Unit Trusts, Private Equity, Alternative Investments, Digital Assets and Fixed Maturity Funds to achieve an optimal risk adjusted return. Kenny is also a CERTIFIED FINANCIAL PLANNER, SGX Academy REIT Trainer, Certified IBF Trainer of Associate REIT Investment Advisor (ARIA) and also invited speaker of REITs Symposium and Invest Fair. You can join my Telegram channel #REITirement – SREIT Singapore REIT Market Update and Retirement related news. https://t.me/REITirement