Paul HO from www.iCompareLoan.com

Central provident fund (CPF) was originally introduced in 1955 by the British Colonial authority to help workers save for their retirement. Over the years, CPF has developed many different uses. One of the main reasons these days for dipping into the CPF is to use their savings to buy an HDB flat or a private property.

CPF savings consistently makes up 30 to 40% of a person’s gross salary, this has provided much liquidity for property purchases and potentially one of the reasons for the inflated property prices.

Most people in Singapore would rely on CPF to fund all or part of their housing loan installment way into 65, 70, 75 years old.

The CPF savings is meant to enable contributors to have a secure retirement. However it could also be CPF that is hindering your retirement plans.

Can You Really Retire At 60 or 65?

When you think of retirement, most would conjure images of sitting back and relaxing, “doing things you enjoy”.

In fact most Singaporeans do not enjoy this luxury when they hit age 65.

With the rising cost of staying alive, it is common for Singaporeans to work beyond the official retirement age, especially if you have yet to pay off your home loan and expensive medical care.

And do not count on hoping to unlock all your savings with The Central Provident Fund (CPF) as there are withdrawal limits and other restrictions. (Reference 2)

Amount Credited into CPF Ordinary Account shrinks

Once you reach 60, the percentage of wages credited into your CPF ordinary account is reduced from 12% to 3.5%.

When you reach 65 years old, while you contribute 5% of your monthly wages to CPF, only 1% of your monthly wages gets credited into your ordinary account. (Table 1)

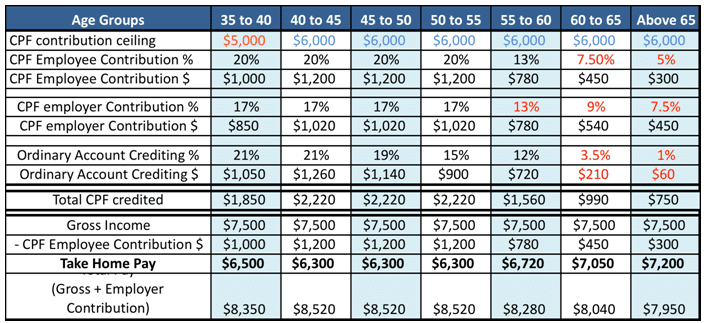

Table 1: Ministry of Finance, Singapore Budget 2015, New CPF Contribution and Allocation Rates from 1 January 2016 for Employees (Note: the Underlined figures are from 1st Jan 2016 onwards)

This compares to 12% for those in the age bracket “Above 55-60” (Table 1). This means that the inflow into your Ordinary Account shrinks over time, all else being equal. This would be a problem for those still servicing home loans and with tight finances.

Those falling into the bottom 20% percentile may be eligible for the Silver Support Scheme, which assists them with payouts of $300 to $750 quarterly starting around first quarter of 2016.

Money stuck in Medisave Account – Never to be seen?

As you age, a growing percentage of your CPF contributions goes into your Medisave Account – starting from age 55 (reference 2), which is allocated to meet your healthcare needs. For those 65 and above, 10.5% of your wages goes into your Medisave Account.

Do note that there are limits as to how much you can withdraw from Medisave.

This means that the savings in your Medisave Account are basically stuck and cannot be used to pay off your housing loans or for other emergencies.

There is a maximum to the savings in your Medisave account, which is known as the Medisave Contribution Ceiling (MCC), of $48,500. Amounts above the MCC will be automatically transferred to your Retirement account not Ordinary Account.

The MCC will be renamed as Basic Healthcare Sum (BHS) and rise to $49,800 with effect from 1 January 2016. The BHS will be held constant when you reach the age of 65.

Also, with effect from Jan 2016, the Medisave Minimum Sum (MMS) will be removed. CPF members do not need to meet the MMS of $43,500. (Source: CPF)

More Cash Payment needed for your Housing loan after 60 years old

Let us investigate whether there is any extra cash out-of-pocket for people as they grow older.

Scenario 1: Mr. Lim’s Property Purchase of 1.25m

Property Price : 1.25m

80% loan : 1m

Age of borrower : 35

Loan Tenure : 30 years

Salary : $7500

Interest rate : 2%, 3% and 4%

Assumption : CPF OA is emptied into installment servicing each month.

Note: CPF Contribution ceiling is $5000 in 2015, $6000 from 1 Jan 2016.

Table 2: CPF Contribution and Take Home Pay of a Person earning $7500 a month. (Source: CPF, iCompareLoan.com)

From the table 2, we can see that the biggest impact is when Mr. Lim reaches 60 years old. The Ordinary account crediting goes from $720 to $210. This is a drop of $510. This means that there would be a bigger cash outlay for installment. This would then easily cause hardship for lower income earners. However in this case, the impact seems to be manageable provided that the person continues to be employed at $7500 a month. In fact, as if to mask the issues, the take home pay actually increases. Hence it is important to take a look at the net pay. (Table 3)

Table 3: Net Pay after paying for Installment. (Source: CPF, iCompareLoan.com)

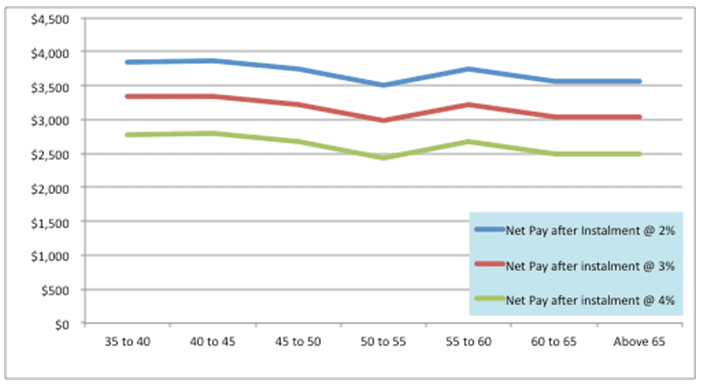

The net pay @ 2% interest rate drops from $3744 to $3564 when Mr. Lim reaches the age group 60 to 65. This drop causes some hardship, but may not be sufficient to cause distress. It becomes critical when interest rate reaches 4% when Mr. Lim is at age group of 60 to 65. Chart 1 illustrates the Net Pay at various mortgage interest rates versus age.

Chart 1: Net Pay of a person earning $7500 after factoring installment assuming all CPF OA is used for installment.

Hence a take home pay of $3564 (2% mortgage interest rate) in 30 years time @ 2% inflation will be equivalent to $1,967 in net present value.

And a take home pay of $3044 (3% mortgage interest rate) in 30 years time @ 3% inflation will be equivalent to $1254 in net present value.

As a general rule of thumb (with some exceptions) (reference 5), higher interest rates correspond to higher inflation.

Payouts from Retirement Account mitigate CPF Ordinary Account woes

For those who took up housing loan before 2013 and with tenures up to ages of 70 to 75, payout from the Retirement account which starts at 65 will slightly cushion your housing loan woes.

At 65, you can withdraw up to 20% of Retirement Account savings (includes first $5,000 withdrawn at age 55. (Reference 3, 4)

Those on the CPF LIFE Plan, a national annuity plan, would also have the option to receive monthly payouts when they hit 65, ranging from $650 to $1,900 (Reference 4) or opt to defer their payout start age up to 70. Deferring the payout start age will allow you to earn a higher interest rate of up to 7% for every year that the payout from CPF LIFE is deferred.

Conclusion

When Mr. Lim hits age group 60 to 65, he starts to see higher Cash outlay to pay for his housing loan due to the drop in CPF crediting into ordinary account. Though the reduction in net take home income is marginal, it is masking the issue of a reduction in incomes and over-funding of Medisave and other accounts. (Appendix A2)

As long as Mr. Lim continues to be employed at $7500 per month until age 65, he should still draw a decent net take home pay of $3564 @ 2% mortgage Interest rate, $3044 @ 3% mortgage interest rate or $2486 @ 4% mortgage interest rate and should be able to withstand a crisis.

However owing to inflation, the present value of his take home pay is small. Mr. Lim cannot hope to retire until he at least pays off his housing loan at 65 as his net take home income will be hardly enough. And he cannot afford to lose his job or get a reduction in pay or he will be in trouble.

While there is probably no immediate crisis within sight, the increased CPF contribution being locked up into Medisave account is worrisome coupled with the escalating medical fees which then empties the Medisave account. The Singapore government should really look at Singapore more as a country than as Singapore Inc., and allocate more resources to our underfunded healthcare system, which by and large are funded by us.

Can Singaporeans really retire at 60 or 65?

References: –

1. Ministry of Finance, Singapore Budget 2015, New CPF Contribution and Allocation Rates from 1 January 2016 for Employees (increases are underlined) http://www.singaporebudget.gov.sg/data/budget_2015/download/annexb1.pdf

2. Buying a Property – use up CPF before it vanishes into retirement account at 55, http://www.icompareloan.com/resources/buying-a-property-use-up-cpf-before-it-vanishes-into-retirement-account-at-55/

3. Source: Central Provident Fund, www.cpf.gov.sg

4. Based on estimates from the CPF LIFE Standard Plan as of April 2015, Source: Central Provident Fund, http://mycpf.cpf.gov.sg/Members/Gen-Info/CPFChanges/COS2015_CPF.htm

5. Mortgage Interest Rates – Key factors that impacts it, http://www.icompareloan.com/resources/mortgage-interest-rates-key-factors-that-impacts-it/

Notes: –

Definition of “Net Take home income” = Gross income – Employee CPF Contribution – Cash Outlay required for housing loan (after factoring CPF-OA being used)

APPENDIX

A1. Installment matrix, (source: http://www.icompareloan.com/calculator/interest-rate-sensitivity-calculator)

A2. Chart 2, Total CPF Contribution of a person earning $7500. (Source, HDB, iCompareLoan.com)

What does iCompareLoan.com do?

www.iCompareLoan.com is a Loan Portal and a Mortgage & Loan broker, helping property buyers and home owners to get the best fit home loan and business owners obtain Business loans for business expansion.

Home Loan Report ™ is Singapore’s first Cloud based Home Loan Report ™ platform to be used by Property agents, financial advisors as well as other Mortgage brokers to prepare reports for their customers.

Home Loan Report ™ – Enterprise allows a property agent’s website to immediately add a loan section. Improve your Google Ranking, let’s viewers increase Time-on-site. Property or Finance sites that deployed Home Loan Report ™ – Enterprise loan section sees viewers stay on their site longer by between 30% to 350% after 4 to 8 weeks of installing the Embedded Loan Plugins.

About PAUL HO:

Paul holds an a B.Eng(Hons) Aberdeen University (UK) and a Masters of Business Administration (MBA) from a Macquarie Graduate School of Business (MGSM) Australia and has distinctions in finance and economics. He also serves as current President of Macquarie University Alumni Association of Singapore.

He is founder of www.iCompareLoan.com, his articles have been syndicated/featured on STproperty, iProperty, BTInvest, TheEdgeProperty, Propwise, Propquest and Yahoo amongst many other sites. He is passionate about helping people enhance their wealth and in making money work harder for them.

Pingback: MP Chen Show Mao 八字 analysis - - - - - - - - - - - - - - - - - - - - Part 92 - Page 235 - www.hardwarezone.com.sg

Hello,

I agree with your last statement. The government knows the short fall but yet slow in countering it, and yet not only once assuring the public that no one will be left un-affordable on their medical bills (with the 3 Ms).

Medical cost: Why need a world-class structure to house various classes, why can’t just has only one and only one “C-class” across all restructured hospital.

Kent