By Sani Hamid, Director (Economy & Market Strategy)

Rising Risks

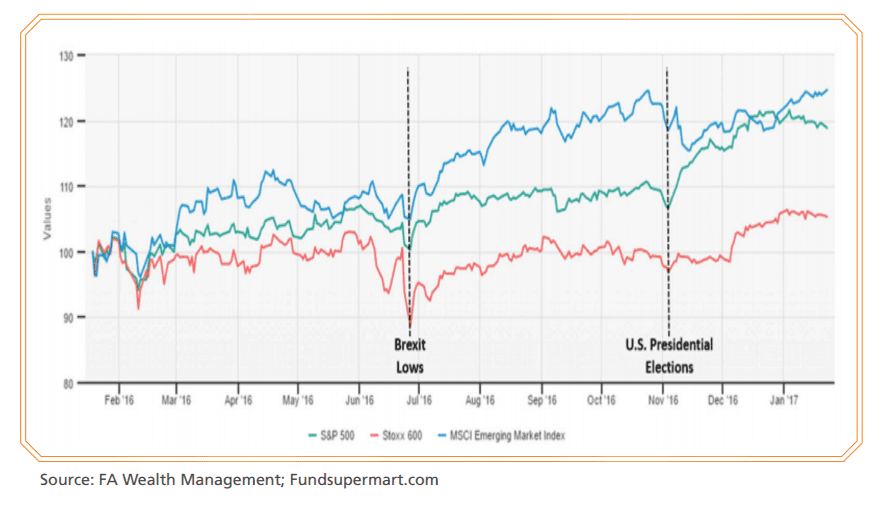

At the moment, we feel there is a sense of “lingering optimism” that the rally we saw in the second half of last year – from the June Brexit lows which continued and even got a boost from Trump’s November electoral win – is merely taking a breather. It’s hard to fault such thinking. After all, markets are higher today – the S&P500 is up 18.5%, Stoxx 600 +18.8% and MSCI Emerging Market +19.8 – than where they were from the Brexit lows despite going through two of the most turbulent events in recent political history.

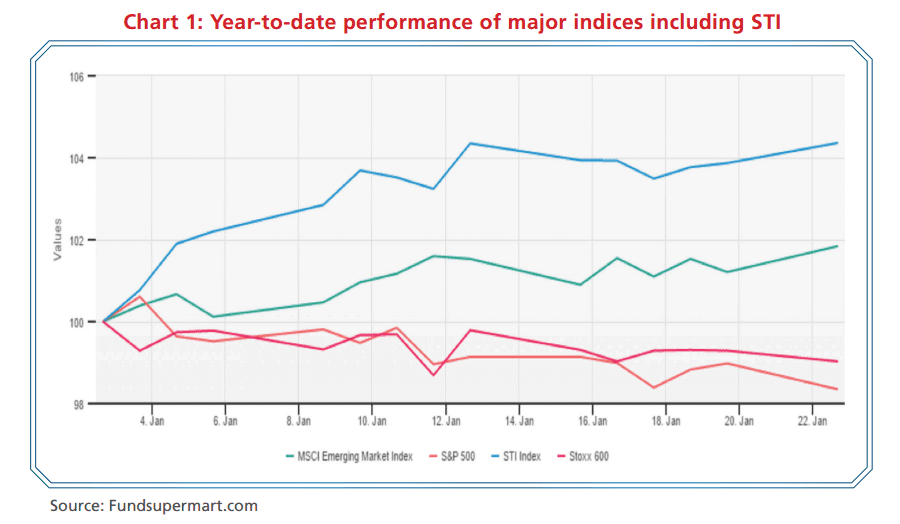

As mentioned earlier, the rally seems to be taking a breather at the moment. Markets are generally holding up and, in some cases, apparently doing well. For example, take the Dow which crossed the psychological 20,000 for the first time in its history. Year-to-date, in Singapore dollar terms, the STI has also rallied sharply by just over 4%, while Asia is up 2.2% and Emerging Markets up 1.8%, based on their respective MSCI indices. Both Europe and the US are down a tad at 1.0% and 1.6% respectively based on the Stoxx 600 & S&P500 (see Chart 1).

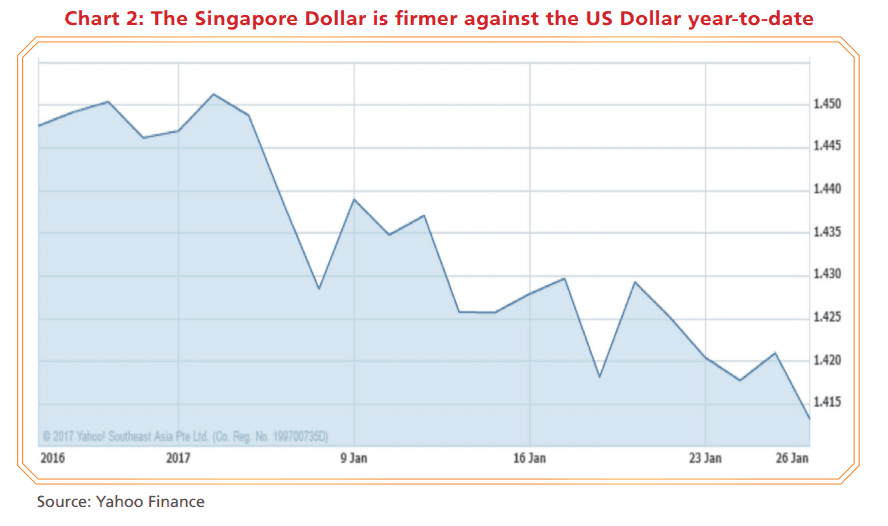

An interesting point to note is that in local currency terms, both Europe and the US indices are in positive territory at 1.8% & 1.5% respectively but because of a stronger Singapore dollar, in local currency terms, these two indices are in negative territory as mentioned earlier. For example, year to-date, the Singapore dollar has appreciated against the US dollar by about 2% (see Chart 2).

“…the Trump administration to adopt an aggressive protectionism, anti-globalisation stance and a tough “American First” approach. Under this scenario, we could see U.S. markets rising by another 5%, while buoyed by stronger domestic-centric policies but off-set by weaker international trade. With a higher cost-of-production, there will a rise in inflationary expectations (+50bp) and the U.S. dollar will strengthen further by 10%. Emerging Markets would likely get hammered, declining by 20% as protectionism and trade wars break out, impacting exports severely. We attribute a 15% probability of this scenario taking place.”

We now believe that the odds of this scenario unfolding has increased to around 20-30% from our original estimate of 15%. Why? Because since taking office on January 20, 2017, the Trump administration has taken such a hardline stance that a lot of the rhetoric, which some argued would be toned down once he takes office, is now becoming actual policy. These include the building of a wall at the Mexican border and issues relating to immigration.

Such callous actions, to us, is going to be the hallmark of the Trump administration where “Everything is strictly business and if it doesn’t benefit America directly, we’re not spending our money and it’s not our problem”. And little wonder that China has already offered herself by saying recently that it is prepared to assume the global leadership role if necessary.

So what we have seen so far (a mere 10 days into the new administration!) tells us that the odds for the worst case is building up.

So what can we expect for the rest of 2017?

We can expect a whole lot more uncertainty, and the financial markets cannot remain immune to this. While presently driven by the excess liquidity in the system and a T.I.N.A. (There Is No Alternative) mentality, eventually, the increasingly socio-political-economic storm that is being kicked-up by the Trump administration will eventually have its repercussions. As such we continue to advocate investors take an overall defensive stance. Are there still opportunities out there? Of course. But one has to be selective and most importantly, nimble enough to get risk off the table when needed in a timely manner. One key development to look out for is the Trump administration’s relationship with the press. This seems to be at an all-time low and is set to go even lower with the White House chief strategist, Stephen Bannon, calling the press the “opposition party” of the current administration, that it should “keep its mouth shut” and that the media has “zero integrity, zero intelligence, and no hard work”.

Unlike Watergate, where it took a blotched burglary to unravel Washington’s biggest scandal at that time to lead to President Nixon’s resignation, we believe the press will have a field day finding reasons to put President Trump on the back foot.

Comment from Blog Owner of My Stocks Investing Journey:

Markets are expected to be volatile after Trump takes office. Interested to know where are the investment risks and opportunities? I manage to convince Sani Hamid (often seen on CNBC) to share with us on Trump Era; Where are the Risks & Opportunities?

Come join me to learn from him at this free workshop I’m organising on 13 Feb and share with / bring some friends: Register here https://msi170213.eventbrite.sg/