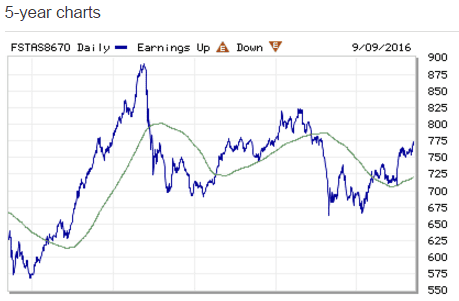

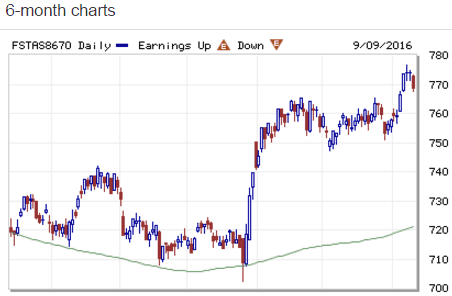

FTSE ST Real Estate Investment Trusts (FTSE ST REIT Index) increases from 756.17 to 768.70 (+1.66%) compare to last post on Singapore REIT Fundamental Comparison Table on August 8, 2016. The index is rejected at the declining trend line resistance with an Evening Doji Star reversal pattern. Base on chart pattern, upside is limited although the index is still in bullish territory. SGX S-REIT (REIT.SI) Index increases from 1162.02 to 1183.53 (+1.85%)

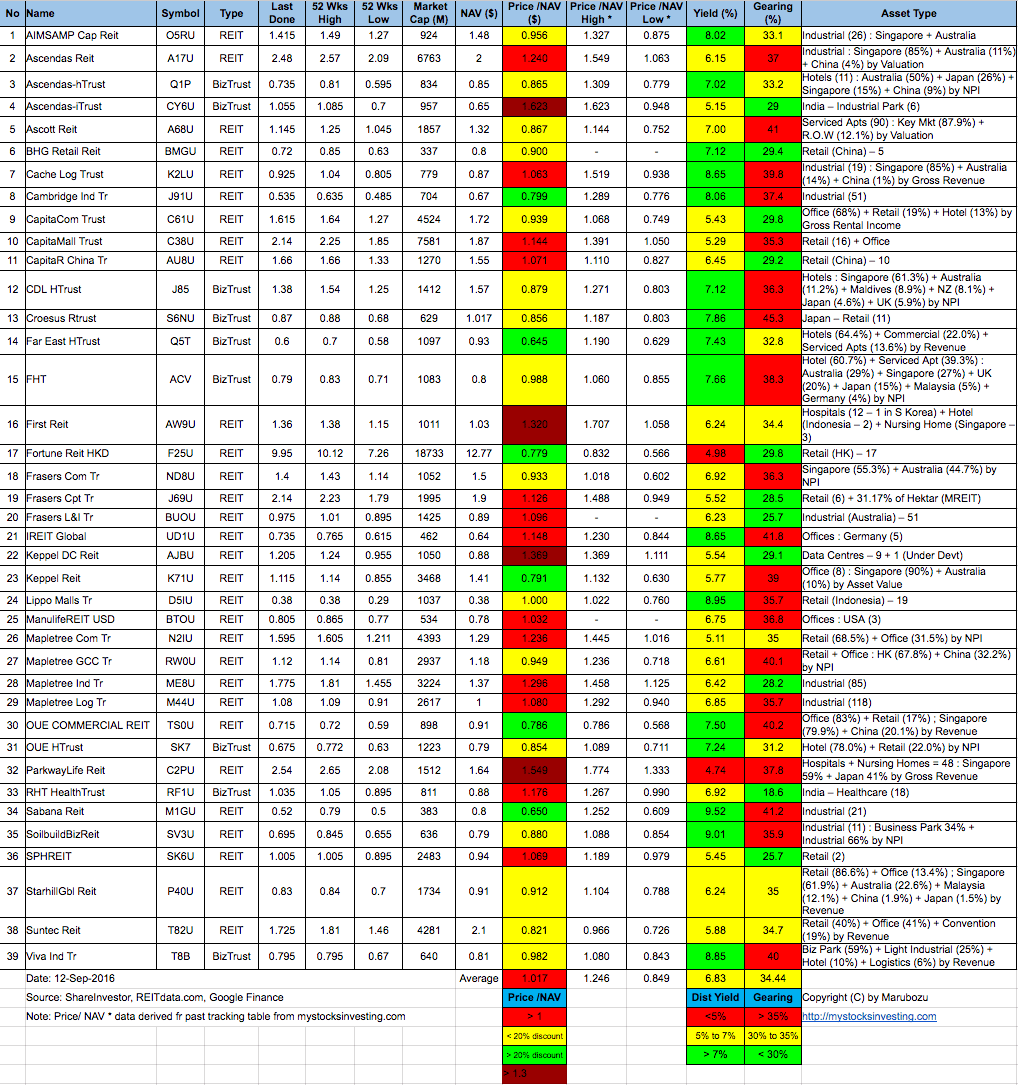

- Price/NAV increases from 1.003 to 1.017 (Singapore Overall REIT sector is slightly over value now)

- Distribution Yield decreases from 6.96% to 6.83% (take note that this is lagging number). Less than half of Singapore REITs (16 out of 39) have Distribution Yield > 7%. Not all the REITs have attractive yield now. A number of REITs like Capita Comm Trust, Capitaland Mall Trust, Frasers Centrepoint Trust, Keppel DC REIT, Mapletree Comm Trust, SPH REIT have less than 6% distribution yield. Selection of Singapore REITs have become much more important now because not all the high yield REIT has strong fundamental.

- Gearing Ratio decreases from 34.50% to 34.44%. 20 out of 39 have Gearing Ratio more than 35%.

- Most overvalue is Ascendas iTrust (Price/NAV = 1.623), followed by Parkway Life (Price/NAV = 1.549) and Keppel DC REIT (Price/NAV = 1.369)

- Most undervalue (base on NAV) is Far East HTrust (Price/NAV = 0.645), followed by Sabana REIT (Price/NAV = 0.65) and Fortune REIT (Price/NAV = 0.779).

- Highest Distribution Yield is Sabana REIT (9.52%), followed by Soilbuild Biz REIT (9.01%) and Lippo Malls Indonesia Retail Trust (8.95%)

- Highest Gearing Ratio is Croesus Retail Trust (45.3%), iREIT Global (41.8%) and Sabana REIT (41.2%)

Disclaimer: The above table is best used for “screening and shortlisting only”. It is NOT for investing (Buy / Sell) decision. To learn how to use the table and make investing decision, Sign up next REIT Investing Seminar here to learn how to choose a fundamentally strong REIT for long term investing for passive income generation.

- Singapore Interest Rate increases from 0.37% to 0.38%.

- 1 month decreases 0.63458% to 0.62233%

- 3 month decreases from 0.87630% to 0.87192%

- 6 month decreases from 1.15072% to 1.15071%

- 12 month decreases from 1.31250% to 1.31183%

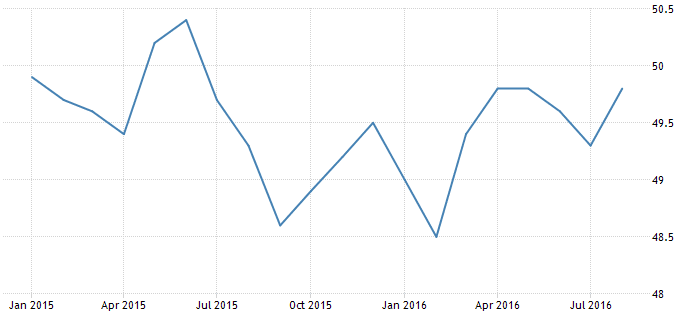

The Singapore PMI increased to 49.8 in August of 2016 from 49.3 in the previous month. Although the reading pointed to the fourteenth consecutive month of contraction, new orders, new export orders, production and employment declined at a slower pace. Also, electronics sector expanded for the first time in 14 months (50.2 from 49.7 in July). Manufacturing PMI in Singapore averaged 50.13 from 2012 until 2015, reaching an all time high of 51.90 in October of 2014 and a record low of 48.30 in October of 2012. Manufacturing PMI in Singapore is reported by the Singapore Institute of Purchasing & Materials Management, SIPMM.

Singapore REITs in general is slightly over value now. Distribution yield for some Singapore REITs with bigger market capitalization is not very attractive. However, there are still opportunities in Singapore REITs with smaller market capitalization. The high distribution yield of these REITs are caused by huge drop in share price due to weak fundamental instead of strong DPU growth. Technically Singapore REITs sector is in bullish territory and on uptrend but facing immediate declining trend line resistance. US Fed is now starting to talk about the interest rate hike which may put pressure on Singapore REITs moving forward. Nevertheless, not all the REIT are affected by the rate hike due to the different debt profile. This may present an opportunity to pick up some fundamentally strong Singapore REITs if there is a knee jerk sell off in the Singapore REITs sector. Come and learn how to spot these gems and identify how to time an good entry in the coming Singapore REIT Investing course.

Original post from https://mystocksinvesting.com