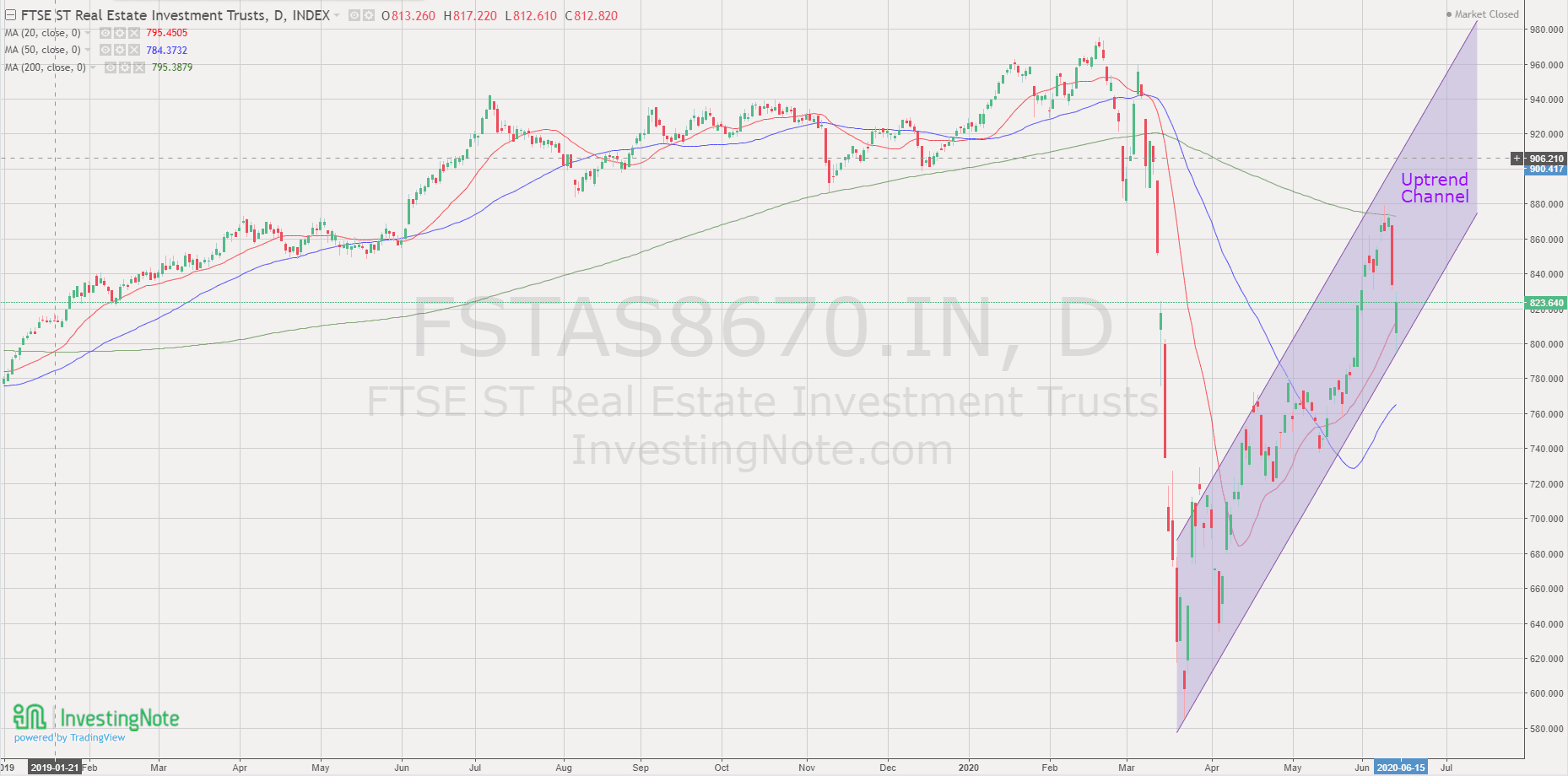

Technical Analysis of FTSE ST REIT Index (FSTAS8670)

FTSE ST Real Estate Investment Trusts (FTSE ST REIT Index) changes from 745.45 to 823.64 (+10.49%) compared to last month update. REIT Index has rebounded c41% as of June 12 closed after hitting the recent high of 878 (c.50% rebound from the bottom).

Currently the REIT index is currently trading in a uptrend channel but have a minor correction back to uptrend channel support and 20D SMA support, after rejected by 200D SMA resistance at about 870. Any rebound from this level is a bullish sign to continue the uptrend. Immediate support at about 800 (channel support) followed by 770-780 (previous resistance turned support and also 50D SMA)

If the REIT index can clear the 200D SMA resistance, the REIT index will enter into a full Bull territory and have a chance to break new high. Current bullish momentum is very strong. Short term direction: Up.

Previous chart on FTSE ST REIT index can be found in the last post Singapore REIT Fundamental Comparison Table on May 17, 2020.

Fundamental Analysis of 40 Singapore REITs

The following is the compilation of 41 REITs in Singapore with colour coding of the Distribution Yield, Gearing Ratio and Price to NAV Ratio. This gives investors a quick glance of which REITs are attractive enough to have an in-depth analysis. DPU Yield for Elite Commercial REIT, United Hampshire REIT are projections based on the IPO prospectus.

- Note 1: The Financial Ratio are based on past data and there are lagging indicators.

- Note 2: This REIT table takes into account the dividend cuts due to COVID-19 outbreak. Yield is calculated trailing twelve months (ttm), therefore REITs with delayed payouts might have lower displayed yields.

- Noted 3: Distribution Yield, NAV, Gearing Ratio would probably be adjusted moving forward.

- Note 4: Historical Price/NAV High and Low information is available here.

- Note 5: Additional financial ratio such as WALE, WADM, All in Interest Cost, Interest Coverage Ratio, Unsecured Loan %, Fixed Interest %, Geographical location of the properties, etc have been compiled and updated monthly in Kenny’s Enhance REIT table.

- Note 6: Some REITs opted for semi-annual reporting.

- Note 7: MAS has raised the Gearing Limit from 45% to 50% on April 16. The implementation of Interest Coverage Ratio (ICR) > 2.5x has been deferred to Jan 1, 2022. See the announcement Higher Leverage Limit and Deferral of Interest Coverage Requirement by MAS.

- Price/NAV increased from 0.84 to 0.92 (Singapore Overall REIT sector is very undervalued now).

- Distribution Yield decreased from 7.68% to 6.45% (take note that this is lagging number). About 39% of Singapore REITs (16 out of 41) have Distribution Yield > 7%. Do note that these yield numbers are based on current prices taking into account delayed distribution/dividend cuts due to COVID-19.

- Gearing Ratio maintains at 36.47%. In general, Singapore REITs sector gearing ratio is healthy. Note: Gearing may be affected (ie. potential increase) as the valuation of the portfolio would be reduced.

- The most overvalued REITs are Keppel DC REIT (Price/NAV = 2.15), followed by Parkway Life (Price/NAV = 1.74), Mapletree Industrial Trust (Price/NAV = 1.65), Mapletree Logistic Trust (Price/NAV = 1.56) and Ascendas REIT (Price/NAV = 1.44).

- The most undervalued REITs (based on NAV) are Eagle Hospitality Trust* (Price/NAV =0.15), followed by Lippo Malls Indonesia Retail Trust (Price/NAV = 0.51), ARA Hospitality Trust (Price/NAV = 0.48), Far East HT (Price/NAV = 0.61) and Starhill Global (Price/NAV = 0.61)

- The Highest Distribution Yield (TTM) is Lippo Malls Indonesia Retail Trust (12.59%), First REIT (11.87%), ARA Hospitality Trust (10.14%) and Soilbuild Business Trust (10.14%) and ARA Logos Logistic Trust (9.45%). Reminder that these yield numbers are based on current prices taking into account delayed distribution/dividend cuts due to COVID-19. Some REITs opted for semi annual reporting and thus no quarterly DPU was announced.

- The Highest Gearing Ratio REITs are Lippo Malls Trust (42.1%), ESR REIT (41.7%), ARA Hospitality Trust (41.0%) and ARA Logos Log Trust (40.8%) (previously Cache Log Trust) and OUE Commercial REIT (40.2%)

- Top 5 REITs with biggest market capitalisation are Ascendas REIT ($11.2B), Mapletree Logistics Trust ($7.2B), CapitaMall Trust ($7.6B), Mapletree Commercial Trust ($6.8B) and Capitaland Commercial Trust ($6.8B)

- The bottom 3 REITs with smallest market capitalisation are Eagle Hospitality Trust ($119M), ARA Hospitality Trust ($235.4M) and Elite Commercial REIT ($234M)

- Singapore REITs which have been included in key Global REIT Indices and STI Index can be found here. Mapletree Industrial Trust would be included into STI on June 22, 2020.

- *Eagle Hospitality Trust is currently suspended

Disclaimer: The above table is best used for “screening and shortlisting only”. It is NOT for investing (Buy / Sell) decision. To learn how to use the table and make investing decision, Sign up next REIT Investing Workshop here to learn how to choose a fundamentally strong REIT for long term investing for passive income generation.

Top 20 Performance of the Month

Singapore SIBOR Rate Watch

- 1 month decreases from 0.31500% to 0.24925%

- 3 month decreases from 0.62325% to 0.54516%

- 6 month decreases from 0.81225% to 0.71788%

- 12 month decreases from 1.26166% to 1.03013%

Summary

Fundamentally the whole Singapore REITs is undervalued now based on simple average on the Price/NAV. The big cap REITs rebounded quickly after the huge REIT crash. Valuation for some big cap REITs are stretch now and some of them are back to pre-COVID19 market crash level. Retail & Hospitality sectors, small & medium cap REITs are very attractive based on the NAV. However, do take note that NAV would probably be adjusted downward caused by the devaluation of property value. We have already seen the NAV of some REITs are adjusted downward and the increase of gearing ratio, from the latest earning release or business update.

Yield spread (reference to 10 year Singapore government bond of 0.981%) has tightened from 6.97% to 5,47%. The risk premium are still attractive to accumulate Singapore REITs in stages to lock in the current price and long term yield after the recovery.

Technically the REIT Index is currently on uptrend and have further upside if the 200D SMA resistance is overcome. REIT sector outperforms the financial sector and STI since the bottom on Mar 23, 2020.

Note: This above analysis is for my own personal research and it is NOT a buy or sell recommendation. Investors who would like to leverage on my extensive research and years on REIT investing experience can approach me separately for REIT Portfolio Consultation.

See other relevant posts here:

- 3 Singapore REITS which have completed V Shape Recovery.

- Money and Me: Will revenge spending help REITs?

- Money and Me: What REITs to Look out for?

- Money and Me: Crazy REIT Sales

- COVID19 Crash: Risk or Opportunity to hold REITs?

- Singapore REITs Black Monday Crash

My Next REIT Online Course is planned on July 18, 2020 (Saturday). Do take note that I only conduct REIT course for retail investors once a quarter as I am busying conducting training for Singapore Exchange (SGX) and Institute Banking and Finance (IBF) Singapore in addition to my financial advisory works.

You can find the registration detail here. https://mystocksinvesting.com/course/singapore-reits-investing/