Base on the chart, Osim is still trading on an long term uptrend with a resistance at $1.08. However, Osim may be pulled back in to the uptrend support at about $0.86 which is also a 78.6% FR level in the near term. Fundamentally OSIM financial performance is average.

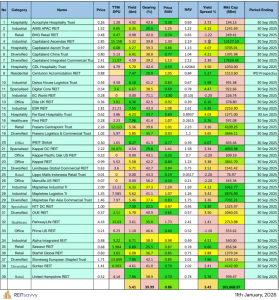

Base on FY2009 Financial Result:

- Current PE = 28 at $0.975 (Overvalue)

- Sales Renevue YOY is degrading since 2006 (Big Concern to me as OSIM may be facing fierce competition and losing its competitive advantage!)

- Net Profit Margin = 4.9% (This is bad for a company that sell BRAND!)

- ROA = 10.1 % (OK)

- ROE = 24.2% (Good)

- Current Ratio = 1.3 (OK)

OSIM does not meet my stock selection criteria and I view the OSIM stock price may plunge if the competive advantages cannot be sustained. We can see quite a number of competing brands in Singapore and definitely in China and price competition definitely is a headache to Osim. Osim has to reinvent itself to continue to push out more innovative products to otherwise they cannot survive in this market place. Things to watch out for: Osim has to constantly push out innovative and “WOW” products every quarter, otherwise their profit margin and sales revenue may be further eroded.

in Adam Khoo’s book, he calculated osim IV value is 1.70 leh.

Your view that OSIM stock price may plunge could be justified by the divergence in the MACD wrt the price.

Hi Amy,

Stock analysis is TIME SENSITIVE.

Adam did the OSIM intrinsic value in 2003 and his book was first released sometime in 2006/2007. Today is already Aug 2010. The business environment has changed compared to 7-8 years ago. You can just compare what would be the competition to OSIM back then and the current situation. How many competing brands to OSIM back in 2003 and now?

In addition, OSIM is no longer in Adam’s portfolio.

I hope my questions probably have answered your question.

Marubozu