SINGAPORE — BHG Retail Real Estate Investment Trust (REIT), the biggest initial public offering (IPO) in Singapore this year, closed unchanged on its debut yesterday from the offer price of S$0.80 after the underwriter emerged to support the market as nervous investors chose to pare their holdings.

BHG Retail REIT units traded in a narrow range of S$0.80 to S$0.805, with 23.8 million shares changing hands to make it the fourth most actively traded counter on the Singapore Exchange despite trading for only about three hours in the session.

DBS Bank, the underwriter for the IPO, said in an aftermarket filing that it had purchased 1.24 million BHG Retail REIT units at S$0.80 to stabilise the price.

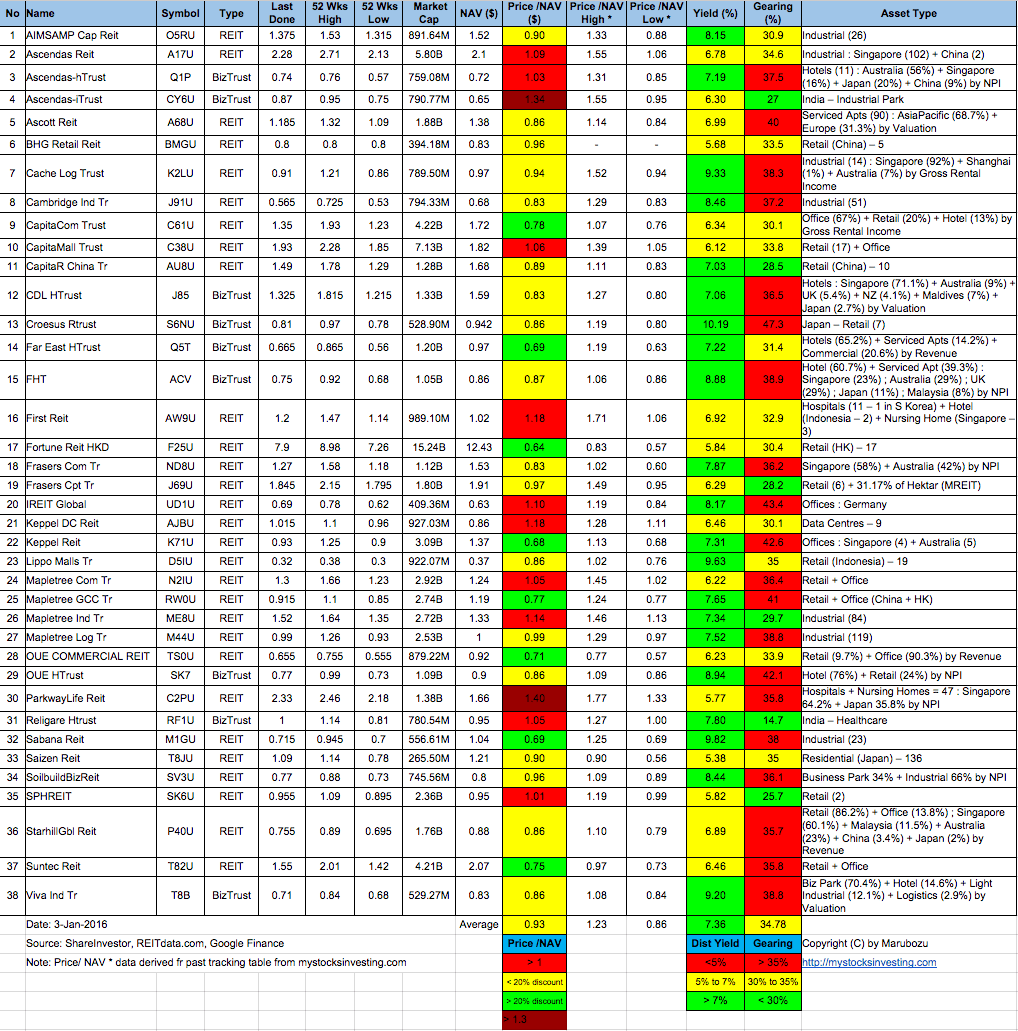

Retail demand for the IPO was lacklustre, suggesting little immediate upside potential. BHG Retail REIT’s public tranche of 8 million units had attracted applications for only 8.48 million or a coverage of just 1.06. All 143.2 million units in the placement tranche were taken up, but the trust manager did not reveal the number of units applied for. In all, BHG Retail REIT raised S$394.2 million from the IPO, after selling more than a third of the offering to cornerstone investors including China Life Insurance and billionaire Chanchai Ruayrungruang.

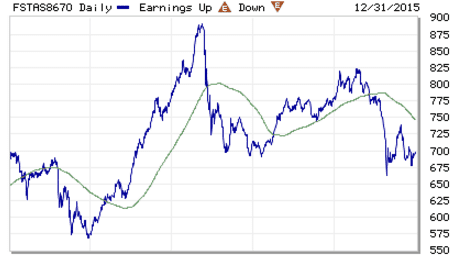

BHG Retail REIT, the first pure-play China retail REIT sponsored by a China-based group, has a portfolio comprising five retail properties in Beijing, Chengdu, Dalian, Hefei and Xining. It is backed by Beijing Hualian Department Store, which owns and manages 29 malls with another 14 malls under development.

Analysts said the newly launched REIT does not look attractive compared with its peers on the SGX, such as CapitaLand Retail China Trust (CRCT). “The REIT is unlikely a strong contender, due to relatively high valuations and artificially boosted distribution yields,” said Mr Ernest Lim, a remisier at CIMB Securities.

IG market analyst Bernard Aw said: “BHG Retail REIT has predicted distribution yields of 5.7 per cent and 6.3 per cent, respectively for 2015 and 2016. However, this was with the Beijing Hualian Group’s agreement to forego a portion of its share distributions from the REIT until 2020. If there was no such arrangement, the estimated distribution yields will fall to 4 per cent and 4.5 per cent.”

CRCT, a China shopping mall REIT sponsored by Singapore property giant CapitaLand, has a portfolio of 10 malls.

“BHG Retail REIT’s fiscal year 2016 forecast distribution yield and price-to-book valuation (P/BV) pale in comparison to CRCT. For example, BHG trades at approximately one time P/BV and 6.3 per cent distribution yield.

“This pales in comparison with CRCT’s P/BV of 0.9 and 7.4 per cent distribution yield. In addition, CRCT has a long listing track record of around nine years and a strong sponsor as well,” said Mr Lim.

BHG Retail REIT is the SGX’s only mainboard listing this year, with the other 12 listings all on the junior Catalist board. BHG Retail REIT is also the first REIT IPO on the SGX this year after several deals were pulled because of uncertain market conditions and concerns over interest-rate hikes.

Mr Francis Siu Wai Keung, chairman and independent director of the trust manager, said: “We felt that Singapore has got a very mature REIT market with robust investors … The investors in Singapore will probably appreciate the value of the REIT more than other places.”

See BHG Retail REIT IPO Analysis here.