I was recently interviewed by The New Paper in Singapore. Hope to share the article with you.

If you’ll like to learn more about the simple and short courses for beginners that I conduct, please click here.

“Chai Hung Yin, The New Paper, Monday, Jan 11, 2016

He started in 2009 with an investment capital of $100,000 from his savings, but lost most of it in about two years.

But investment coach and financial blogger Kenny Loh, 45, was undaunted.

He says: “If I keep thinking about the $100,000, I cannot start again.

“I cannot give up. I realised that to be a successful trader, I need to be disciplined. Everyone has a different risk profile and goals.

“I continued to convince myself that there is no shortcut or quick fix – I need time and experience. In an environment of low interest rates, we have to invest.”

Mr Loh, who previously held a senior management position in a multinational corporation, said his mistakes were costly, but they helped him devise his own approach in investment.

This approach combines fundamental analysis, technical analysis, real estate investment trusts (Reits) assessment and analysis of the global economy for passive income generation.

He says: “You need to go through the whole cycle before you know how to anticipate.”

Mr Loh started accumulating stocks after reading investment books in February 2009 during the global financial crisis.

He says: “At that time, stocks were cheap. Counters like OCBC and KepCorp were at about $4. I didn’t have any financial knowledge, so I just looked at price.”

He realised he couldn’t just rely on books so he enrolled in a course, which cost him $4,000.

He says: “After four days, I still couldn’t invest because I was still blur and confused due to an information overload.

“From zero knowledge to so much knowledge… I couldn’t absorb it.”

BLOG

Mr Loh decided to blog about his investment journey because “if I don’t practise, I will lose the $4,000 (in course fees)”.

He says: “I force myself to do analysis before I post.

“I also use the blog as my library – I can be trading anywhere in the world, and yet I can still refer to my blog entry.”

He started accumulating S-chips – Chinese companies listed on the Singapore Exchange.

Says Mr Loh: “After you know the tactic, you feel that it is so easy to invest. That was how I got burned. Theory and action are different.”

One of the S-chips he bought into was sportswear-maker China Hongxing Sports. He bought $50,000 worth of stocks.

But the stock was suspended from trading in February 2011 after external auditors flagged financial irregularities in the company’s accounts. It remains suspended as of Jan 4 this year.

Mr Loh says: “Back then, it passed all the criteria – all ratios looked good. So I started accumulating the stock. Now, I cannot trade the stock. My money is stuck there. Once it resumes trading, people will sell. I assume the investment is gone. Otherwise it will affect me.

“This is something investors will not know. Whatever is in the financial statement can be manipulated. It can be fake. There is no chance for us (investors) to run.

“Because of this, I don’t trade in penny stocks even though the entry level is easy and cheap.”

Through his costly mistakes, Mr Loh learnt invaluable skills, which “you cannot learn from a textbook”.

“Everyone won’t share how they lose money,” he adds.

He is now teaching his 16-year-old son how to invest.

“I learnt all these skills but it was too late for me. At a certain age, you can’t take too much risk. I am more defensive now.”

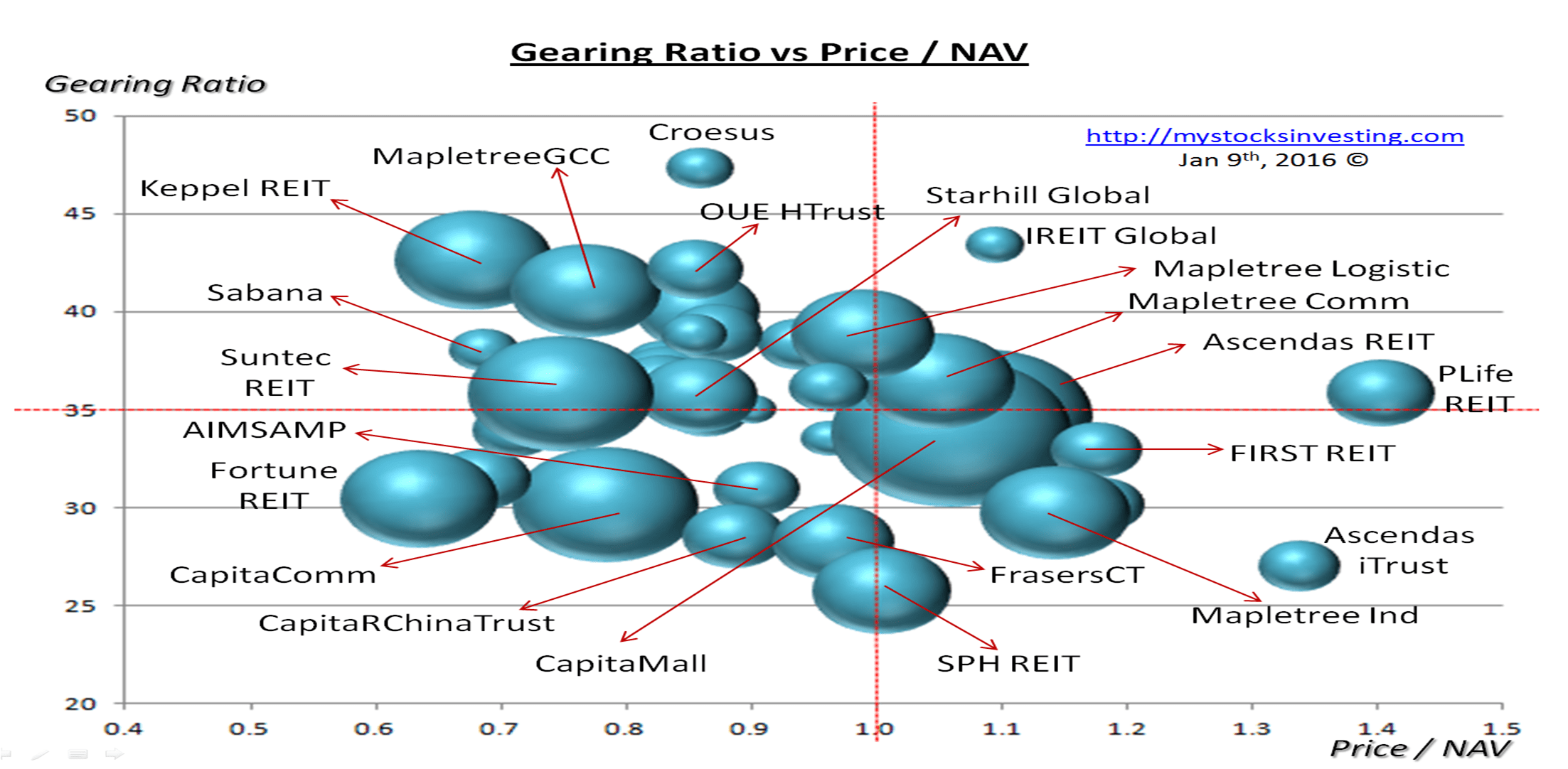

He now invests in Reits, which give him a consistent passive income as he builds up his retirement portfolio.

He has about tens of thousands invested and is keeping the majority of his assets in cash, in anticipation of a market crash, where he plans to pick up stocks on the cheap.

Despite the threat of rising interest rates affecting the real estate industry, Mr Loh looks for Reits that are not affected, such as those that do not need refinancing in the next few years so that income is protected.

– See more at: http://business.asiaone.com/news/big-loss-didnt-deter-investment-coach

If you’ll like to learn more about the simple and short courses for beginners that I conduct, please click here.