Singapore REIT Monthly Update (September 3rd 2022)

Happy 20th anniversary to S-REITs!

Back in 17th July 2002, CapitaMall Trust was listed on the Singapore exchange. Today, there are 38 S-REITs, with a combined market cap of over S$100 Billion.

Technical Analysis of FTSE ST REIT Index (FSTAS351020)

FTSE ST Real Estate Investment Trusts (FTSE ST REIT Index) decreased from 828.74 to 792.62 (4.36%) compared to last month’s update. The REIT Index broke the 800 psychological support and current testing the trend support at about 792. The 20-day and 50-day Simple Moving Average (20 SMA and 50 SMA) are about to crossover, the 20 SMA dropping sharply in the past month. The REIT Index failed to break the 200 SMA Resistance in August, and is now on a short-term downtrend.

- Support Lines: Blue

- Resistance Lines: Red

- Short-term direction: Down

- Medium-term direction: Down

- Long-term direction: Sideways

- Immediate Support at 792 (Blue Line)

- Immediate Resistance at 200 SMA

Technically, FTSE ST REIT Index is currently at a very crucial support level at 792. Breaking this support will start the bear trend for Singapore REIT sector. If the REIT index is able to rebound from this level, it is expected the index will have short term bullish momentum towards 830 (200D SMA resistance).

Normal Timeframe chart (~2 years)

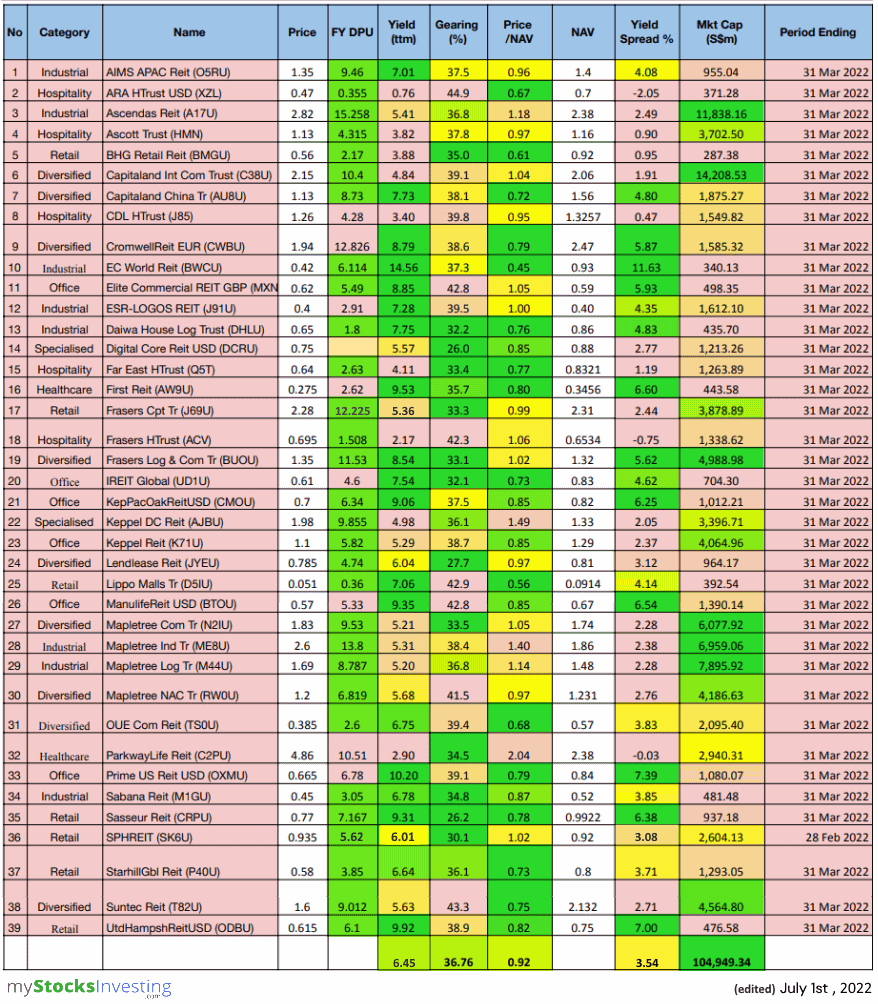

Previous chart on FTSE ST REIT index can be found in the last post: Singapore REIT Fundamental Comparison Table on August 7th, 2022.

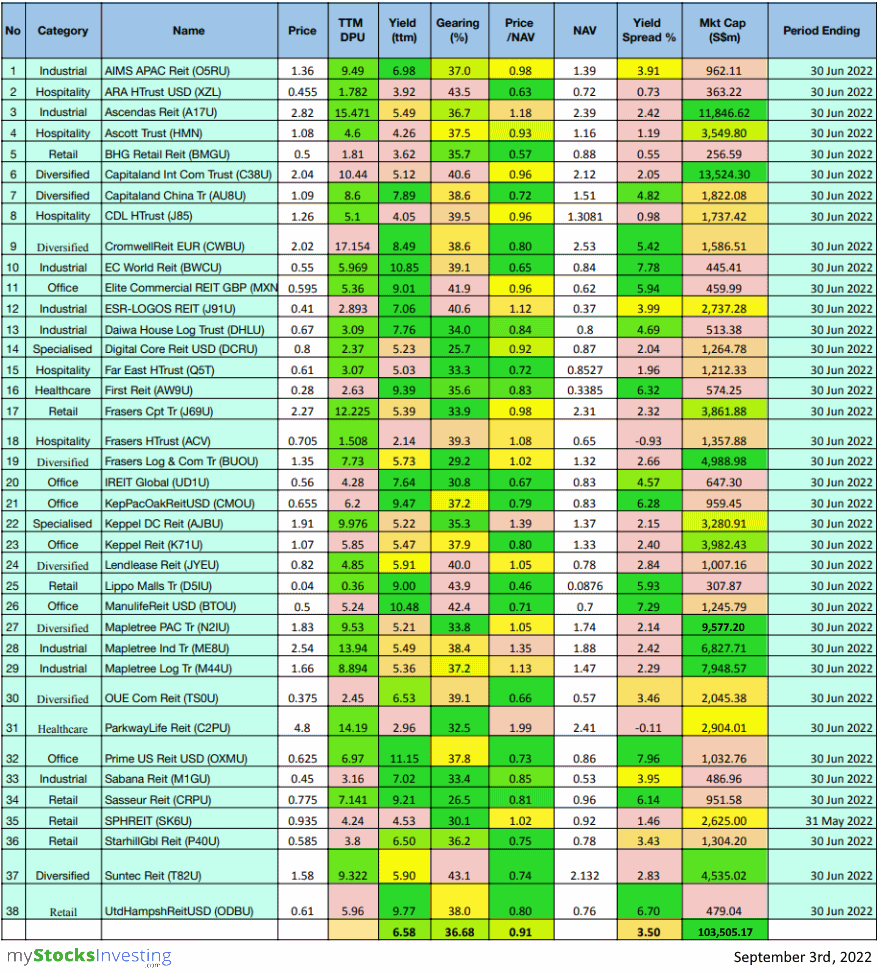

Fundamental Analysis of 38 Singapore REITs

The following is the compilation of 38 Singapore REITs with colour-coding of the Distribution Yield, Gearing Ratio and Price to NAV Ratio.

- The Financial Ratios are based on past data and there are lagging indicators.

- This REIT table takes into account the dividend cuts due to the COVID-19 outbreak. Yield is calculated trailing twelve months (ttm), therefore REITs with delayed payouts might have lower displayed yields, thus yield displayed might be lower for more affected REITs.

- All REITs are now updated with the latest Q2 2022 business updates/earnings.

- Since MPACT started trading, values shown below (except price and market cap) are of MCT.

- MNACT has been removed.

Data from StocksCafe REIT Screener. https://stocks.cafe/kenny/advanced

What does each Column mean?

- FY DPU: If Green, FY DPU for the recent 4 Quarters is higher than that of the preceding 4 Quarters. If Lower, it is Red.

- Most REITs are green since it is compared to FY20/21 as the base (during the pandemic)

- Yield (ttm): Yield, calculated by DPU (trailing twelve months) and Current Price as of September 3rd, 2022

- Digital Core REIT: Yield calculated from IPO Prospectus.

- Daiwa House Logistics Trust: Yield calculated from trailing six months distribution.

- Gearing (%): Leverage Ratio.

- Price/NAV: Price to Book Value. Formula: Current Price (as of September 3rd, 2022) over Net Asset Value per Unit.

- Yield Spread (%): REIT yield (ttm) reference to Gov Bond Yields. REITs trading in USD is referenced to US Gov Bond Yield, everything else is referenced to SG Gov Bond Yield.

Price/NAV Ratios Overview

- Price/NAV decreased to 0.91.

- Decreased from 0.95 from August 2022.

- Singapore Overall REIT sector is undervalued now.

- Take note that NAV is adjusted upwards for some REITs due to pandemic recovery.

- Most overvalued REITs (based on Price/NAV)

- Parkway Life REIT (Price/NAV = 1.99)

- Keppel DC REIT (Price/NAV = 1.39)

- Mapletree Industrial Trust (Price/NAV = 1.35)

- Ascendas REIT (Price/NAV = 1.18)

- Mapletree Logistics Trust (Price/NAV = 1.13)

- ESR-LOGOS REIT (Price/NAV = 1.12)

- No change to the Top 6 compared to last month’s update.

- Most undervalued REITs (based on Price/NAV)

- Lippo Malls Indonesia Retail Trust (Price/NAV=0.46)

- BHG Retail REIT (Price/NAV = 0.57)

- ARA Hospitality Trust (Price/NAV = 0.63)

- EC World REIT (Price/NAV = 0.65)

- OUE Commercial REIT (Price/NAV = 0.66)

- IREIT Global (Price/NAV = 0.67)

Distribution Yields Overview

- TTM Distribution Yield Increased to 6.58%.

- Increased from 6.32% in August 2022.

- 15 of 40 Singapore REITs have distribution yields of above 7%. (1 more than last month’s update)

- Do take note that these yield numbers are based on current prices taking into account the delayed distribution/dividend cuts due to COVID-19, and economic recovery. The recent sell-off contributed to the increase in average yield.

- Highest Distribution Yield REITs (ttm)

- Prime US REIT (11.15%)

- EC World REIT (10.85%)

- Manulife US REIT (10.48%)

- United Hampshire REIT (9.77%)

- Keppel Pacific Oak US REIT (9.47%)

- First REIT (9.39%)

- Reminder that these yield numbers are based on current prices taking into account delayed distribution/dividend cuts due to COVID-19.

- Some REITs opted for semi-annual reporting and thus no quarterly DPU was announced.

- A High Yield should not be the sole ratio to look for when choosing a REIT to invest in.

- Yield Spread tightened to 3.50%.

- Decreased from 3.67% in August 2022.

Gearing Ratios Overview

- Gearing Ratio increased slightly to 36.68%.

- Decreased from 36.52% in August 2022.

- Gearing Ratios are updated quarterly. Therefore some of the following REITs have updated gearing ratios compared to last month.

- Highest Gearing Ratio REITs

- Lippo Malls Indonesia Retail Trust (43.9%)

- ARA Hospitality Trust (43.5%)

- Suntec REIT (43.1%)

- Manulife US REIT (42.4%)

- Elite Commercial REIT (41.9%)

- ESR-LOGOS REIT (40.6%)

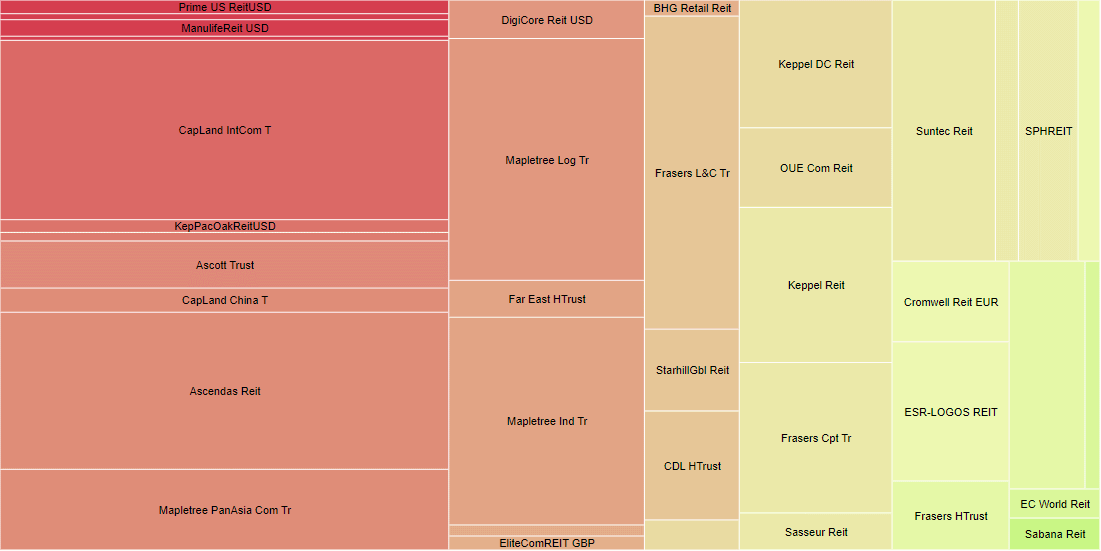

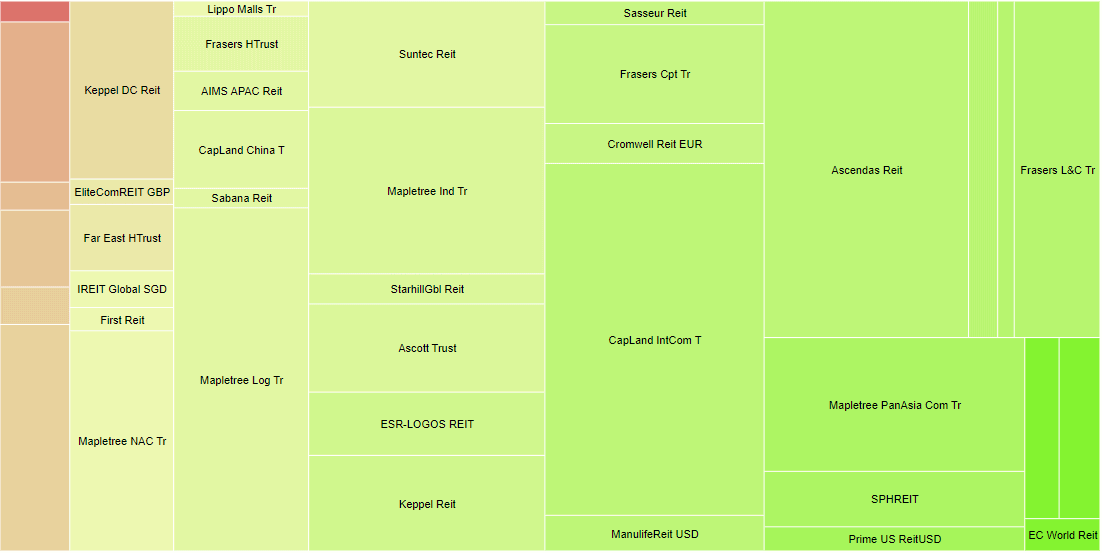

Market Capitalisation Overview

- Total Singapore REIT Market Capitalisation decreased by 4.69% to S$103.51 Billion.

- Decreased from S$108.60 Billion in August 2022.

- Biggest Market Capitalisation REITs:

- Capitaland Integrated Commercial Trust ($13.52B)

- Ascendas REIT ($11.85B)

- Mapletree Pan Asia Commercial Trust ($9.58B)

- Mapletree Logistics Trust ($7.95B)

- Mapletree Industrial Trust ($6.83B)

- Frasers Logistics & Commercial Trust ($4.99B)

- MPACT (formerly MCT) moved from 5th to 3rd rank since its merger with MNACT.

- Smallest Market Capitalisation REITs:

- BHG Retail REIT ($257M)

- Lippo Malls Indonesia Retail Trust ($308M)

- ARA Hospitality Trust ($363M)

- EC World REIT ($445M)

- Elite Commercial REIT ($460M)

- United Hampshire REIT ($479M)

Disclaimer: The above table is best used for “screening and shortlisting only”. It is NOT for investing (Buy / Sell) decision. If you want to know more about investing in REITs, here’s a subsidised 2-day course with all you need to know about REITs and how to start investing in them.

Top 20 Worst Performers of the Month in August 2022

(Source: https://stocks.cafe/kenny/advanced)

SG 10 Year & US 10 Year Government Bond Yield

- SG 10 Year: 3.07% (decreased from 2.63%)

- US 10 Year: 3.19% (decreased from 2.83%)

Major REIT News in August 2022

S-REITs Earnings Season for the Period Ending 30 June 2022 has wrapped up

All S-REITs have finished reporting their earnings. Of the 37 REITs who reported their earnings for Q1 and/or Q2 (taking most recent DPU) (excl. DC REIT), the overview on Q-o-Q or H-o-H DPU change are as follows:

16 REITs have reported an increase in DPU,

7 REITs have reported no change in DPU, and

14 REITs have reported a decrease in DPU.

S-REITs are now 20 years old!

THE SMART INVESTOR: Time flies, and in the blink of an eye, it’s been 20 years since the first Singapore REIT (S-REIT) was listed on our shores.

The REIT Association of Singapore (Reitas) organised an event to celebrate this milestone, and Singapore Exchange’s (SGX: S68) CEO Loh Boon Chye noted that the S-REIT sector continues to be one of the fastest-growing in Asia.

S-REITs form the second-largest REIT market outside of Japan, with a total of 43 REITs (and Business Trusts) with a market value of more than S$111 billion, making up close to 12% of the market capitalisation of all SGX stocks.

The very first REIT, CapitaMall Trust, was listed on the Singapore market back on 17 July 2002.

It was later merged with CapitaCommercial Trust to form CapitaLand Integrated Commercial Trust (SGX: C38U). Read More

Lendlease Global Commercial REIT first S-REIT to attain net-zero carbon target

EDGEPROP: Lendlease Global Commercial REIT (LREIT) has achieved its net-zero carbon target ahead of its original target through energy-efficiency initiatives and reducing energy consumption within its Singapore assets, it announced on Aug 29.

“LREIT is poised to make strides in our decarbonisation journey to achieve absolute zero carbon by 2040, as the first S-REIT to attain net-zero carbon status,” says Kelvin Chow, the CEO of LREIT’s manager. “Besides adopting energy-efficiency measures, we are actively exploring new ways to reduce our energy consumption.” Read More

Summary

Fundamentally, the whole Singapore REITs landscape is undervalued based on the average Price/NAV value of the S-REITs. Below is the market cap heat map for the past 1 month. Generally, S-REITs in the past month have decreased in market cap. August has been a bearish month for S-REITs.

(Source: https://stocks.cafe/kenny/overview)

Yield spread (in reference to the 10 year Singapore government bond of 3.07% as of 3rd September 2022) tightened from 3.67% to 3.50%. The S-REIT Average Yield increased from 6.32% to 6.58%, while the increase in the Government Bond Yields more than offsets this Average S-REIT Yield increase. This resulted in the tightening of yield spread. The yield of the REITs sector needs to increase to maintain the average yield spread of 4%. Despite the bearish month of August, S-REITs have been resilient and have one of the highest risk-adjusted dividend yields compared to other stock exchanges.

Technically, FTSE ST REIT Index is currently at a very crucial support level at 792. Breaking this support will start the bear trend for Singapore REIT sector. If the REIT index is able to rebound from this level, it is expected the index will have short term bullish momentum towards 830 (200D SMA resistance).

Note: This above analysis is for my own personal research and it is NOT a buy or sell recommendation. Investors who would like to leverage my extensive research and years of Singapore REIT investing experience can approach me separately for a REIT Portfolio Consultation.

Kenny Loh is an Associate Wealth Advisory Director and REITs Specialist of Singapore’s top Independent Financial Advisor. He helps clients construct diversified portfolios consisting of different asset classes from REITs, Equities, Bonds, ETFs, Unit Trusts, Private Equity, Alternative Investments, Digital Assets and Fixed Maturity Funds to achieve an optimal risk adjusted return. Kenny is also a CERTIFIED FINANCIAL PLANNER, SGX Academy REIT Trainer, Certified IBF Trainer of Associate REIT Investment Advisor (ARIA) and also invited speaker of REITs Symposium and Invest Fair. You can join my Telegram channel #REITirement – SREIT Singapore REIT Market Update and Retirement related news. https://t.me/REITirement

{kind=link}