Exclusive Insights: Interview with ALOG REIT CEO, Ms Karen Lee

In this coverage of the ESR-REIT and ARA LOGOS Logistics Trust merger, I had the opportunity to speak to Ms Karen Lee, CEO of ALOG REIT on the 8 November 2021.

Proposed merger of ESR REIT with ARA LOGOS Logistics Trust: Resources

- Proposed merger with ARA LOGOS Logistics Trust Presentation Slides – ESR REIT

- Proposed merger with ESR REIT Presentation Slides – ARA LOGOS Logistics Trust

- MoneyFM 89.3 Radio Interview covering the REIT mergers

- Frequently Asked Questions – Proposed Merger Of ESR-REIT And ARA LOGOS Logistics Trust By Way Of A Trust Scheme Of Arrangement

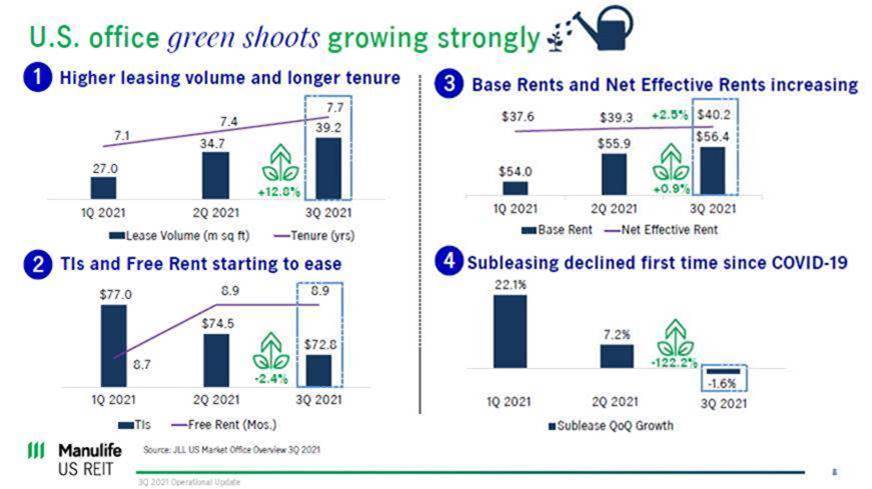

- ARA LOGOS Logistics Trust Third Quarter Business Updates for Period Ending 30 September 2021

Cold Storage Logistics

[Editors note: Cold Storage Facilities are facilities that store frozen or chilled goods, such as frozen food, chilled food and pharmeceuticals. Demand for such facilities around the world is high, especially nowadays since the COVID-19 Vaccines are in high demand and most of them require such facilities.]

Kenny: I heard that Cold Storage Logistics are a new asset class, just like Data Centres. What do you think about the future growth of this sector, and would there be any rerating of the REIT as this asset class is added into your portfolio?

Karen: I wouldn’t say Cold Storage and Data Centres are the same, but they are both specialised sectors. If you look across the other Industrial REITs in Singapore, not many of them have dedicated Cold Storage facilities. ALOG has one such facility (ALOG Cold Centre at 2 Fishery Port Road). Depending on industrial requirements, these facilities can be configured accordingly (freezer, chiller, ambient etc.). Right now, especially because of COVID, there is a shortage of Cold Storage facilities islandwide, meaning our facility has an occupancy close to 100%.

However, landlords typically do not build such facilities because the capex is very high. Some dedicate only a portion of their property to have Cold Storage facilities. Since our current sponsor is a logistics developer (LOGOS), they have experience in building specialised facilities such as Cold Storage.

Kenny: For Cold Storage Facilities, which countries have higher demand for such facilities?

Karen: All countries have high demand for such facilities. Due to COVID and the supply chain disruption, there’s a shortage in Cold Storage. You’ll be surprised at how much frozen food and pharmaceutical products are being stored in the event of future supply chain disruptions.

Kenny: So in the near term, is ALOG planning for acquisitions of Cold Storage Facilities (or conversion to such facilities) or only when the Merger with ESR–REIT is complete?

Karen: Right now we are at a standstill (due to the ongoing merger) but we do have tenants who are enquiring about converting to Cold Storage facilities and, we are still exploring those on a case-by-case basis.

Merger of ESR REIT and ARA LOGOS Logistics Trust

Kenny: Regarding the Merger, is there a Plan B for ALOG, in case the merger with ESR REIT does not go through?

Karen: If the merger doesn’t go through, it’ll be business as usual for ALOG. Having said that, we are quite confident the merger will go through, as we have articulated the merits of the merger for both REITs. On our own, we can still grow, albeit at a slower pace. ALOG, as a relatively small REIT, can’t possibly acquire large transactions at one go, we’ll have to break it up. However, a larger REIT will benefit from the economies of scale. Investors need to see that scale is very important for REITs to grow.

Post-merger, we have a clear path to grow ESR-LOGOS REIT. Our enlarged sponsor has over US$50 billion in New Economy AUM and US$10 billion in Development Work-in-Progress New Economy pipeline. It is a very large pipeline for any REIT sponsor to offer. I have also been communicating to investors that for ALOG holders, you are not selling out, but rather you are rolling over 90% of units to an enlarged platform, as well as capitalising on existing returns with the 10% cash.

Kenny: Only a little more than a year ago, you took over as ALOG’s CEO. Is this succession and the merger pre-planned?

Karen: Back when I took over as CEO of ARA LOGOS Logistics Trust (Formerly Cache Logistics Trust), the only transaction that happened was only ARA’s acquisition of LOGOS in March last year. The decision to merge with ESR REIT was as recent as 2 months ago, where Adrian and I discussed the merits of a potential merger between the two REITs after the proposed merger of ESR Cayman and ARA Asset Management was announced.

The biggest challenge moving forward is how quickly we can execute the plans and strategies we have been articulating to the unitholders, in terms of acquisitions.

Kenny: What do you think will be the biggest challenge that your team will face post-merger, and how will your team plan to resolve them?

Karen: We have been quite busy with the transaction, therefore we are still in the midst of discussions about the integration process. We need to evaluate the talents available on both sides and pick the best man for the job, for the new roles the enlarged REIT will have.

I would say the biggest challenge moving forward is how quickly we can execute the plans and strategies we have been articulating to the unitholders, in terms of acquisitions. We have not been given a timeline to do so but it will be important for us to execute them quickly so that we would be credible in delivering what we said we would do. We would also set out to be included in more indices in the future, improving trading liquidity and visibility to institutional investors, and in time to come, be in the same league as some of the bigger players.

Kenny: Investors and Analysts are looking at whether you can execute what you have promised.

Karen: I think Adrian and I have delivered what we have promised for our respective REITs. For ALOG, we articulated 3 key tasks we would do, namely Acquisitions, Divesting Non-Core Assets and AEIs. Once we delivered them, ALOG had a good re-rating after we carried out these corporate actions.

Kenny: Would you foresee immediate acquisitions to be carried out post merger?

Karen: Out of the over US$50 billion in New Economy AUM and US$10 billion in Development Work-in-Progress New Economy pipeline across 10 countries where the Sponsor has presence in, US$2 billion of these are core assets that are immediately visible and executable. Adrian and I will look at the c.S$2 billion of immediately visible and executable New Economy pipeline we have been talking about, to identify which assets are ready to be injected into the REIT.

Performance of ARA LOGOS Logistics Trust

In the past 18 months, we have maintained high portfolio occupancy rates, achieved positive rental reversion, divested non-core assets to rebalancing our portfolio, and managed to reduce leverage and lower our all-in financing costs. We executed Asset Enhancements to ensure our assets remain competitive and relevant to our tenants.

Kenny: I would like to congratulate you on the great performance of ALOG for the past year, beating other Industrial S-REITs. What do you think you have done right?

Karen: I must thank you for these kind words. When I took over in August 2020, the immediate task was to improve the performance of the REIT. Prior to me taking over, the rebranding of Cache Logistics Trust to ARA LOGOS Logistics Trust signified a fresh start, with a new sponsor (LOGOS) onboard. LOGOS demonstrated its commitment to grow the REIT, and alignment of interests with unitholders, via asset injection. We completed our first portfolio acquisition in Australia earlier this year, and LOGOS backstopped the entire preferential offering when we did the fund raising for that acquisition.

Coming from an operator background, it is really important to strengthen the portfolio operating metrics. In the past 18 months, we have maintained high portfolio occupancy rates, achieved positive rental reversion, divested non-core assets to rebalancing our portfolio, and managed to reduce leverage and lower our all-in financing costs. We executed Asset Enhancements to ensure our assets remain competitive and relevant to our tenants. The market can see that we have put in significant efforts to deliver these results, and the results have shown. I am proud of my team in helping us to deliver the stellar results of ALOG, creating value for our unitholders. Once again, being transparent to our unitholders and delivering what we have outlined is very critical. For the enlarged REIT itself, we would be following a similar strategy.

Kenny Loh is a Senior Financial Advisory Manager and REITs Specialist of Singapore’s top Independent Financial Advisor. He helps clients construct diversified portfolios consisting of different asset classes from REITs, Equities, Bonds, ETFs, Unit Trusts, Private Equity, Alternative Investments, Digital Assets and Fixed Maturity Funds to achieve an optimal risk adjusted return. Kenny is also a CERTIFIED FINANCIAL PLANNER, SGX Academy REIT Trainer, Certified IBF Trainer of Associate REIT Investment Advisor (ARIA) and also invited speaker of REITs Symposium and Invest Fair. You can join my Telegram channel #REITirement – SREIT Singapore REIT Market Update and Retirement related news. https://t.me/REITirement