The Retirement Roadmap: How to Build a Portfolio That Outlasts the Market

Building a diversified retirement portfolio is less about “winning” the stock market and more about ensuring that when you’re ready to stop working, your money hasn’t stopped working for you.

As Nobel laureate Harry Markowitz, the father of Modern Portfolio Theory, famously said:

“Diversification is the only free lunch in investing.”

In 2026, the “free lunch” looks a bit different than it did a decade ago. With the rise of AI-driven market shifts and higher-for-longer interest rates, a simple “set it and forget it” approach may no longer suffice. Here is how to build a resilient, diversified portfolio for your retirement.

1. The Core Pillars of Asset Allocation

The foundation of diversification is spreading your capital across different asset classes that don’t move in lockstep.

- Equities (Stocks): These are your growth engine. Even in retirement, you likely need some stock exposure to outpace inflation.

- Fixed Income (Bonds): These act as the “ballast” of your ship. In 2026, high-quality corporate and government bonds are offering the most attractive yields in years, providing reliable income.

- Cash & Equivalents: This includes high-yield savings accounts and Money Market Funds. This is your “liquidity bucket” for immediate expenses.

2. Diversifying Within Asset Classes

True diversification goes deeper than just “stocks vs. bonds.” You must ensure you aren’t over-concentrated in one area.

Geographic Diversification

The U.S. market has dominated for years, but 2026 market outlooks suggest looking toward International Developed Markets and Emerging Markets (specifically in Asia). This protects you if the U.S. economy faces a localized downturn.

Sector & Style Diversification

Don’t just own “Big Tech.” A well-rounded portfolio balances:

- Growth Stocks: High-potential companies (e.g., AI infrastructure).

- Value Stocks: Established companies that pay dividends (e.g., healthcare, utilities).

- Market Cap: A mix of Large-cap (stable giants) and Small-cap (high-growth potential) companies.

3. The “Glide Path” Strategy

As you approach your retirement date, your “risk budget” changes. This is often managed through a Glide Path.

| Life Stage | Common Allocation (Equity/Bond) | Focus |

| Early Career | 90% Equity / 10% Bond | Maximum Growth |

| Mid Career | 70% Equity / 30% Bond | Balanced Growth |

| Near Retirement | 50% Equity / 50% Bond | Capital Preservation |

| In Retirement | 30% Equity / 70% Bond | Income Generation |

Pro Tip: Many investors use Target-Date Funds (TDFs), which automatically handle this rebalancing for you as you get closer to your target retirement year.

4. Modern Tools: Active ETFs and Alternatives

In the current 2026 investment landscape, “passive” investing is being complemented by Active ETFs. These funds allow professional managers to navigate market volatility in real-time—specifically useful in fixed income where interest rate shifts can be unpredictable.

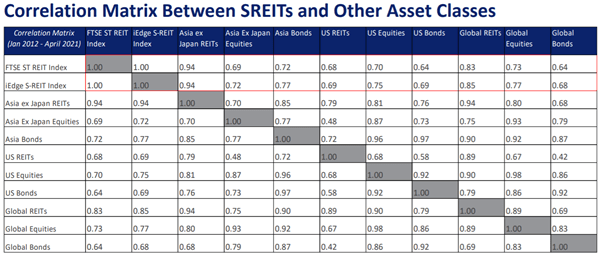

Additionally, seasoned investors are increasingly looking at Alternative Assets like Real Estate Investment Trusts (REITs) or Commodities (Gold) to hedge against stubborn inflation.

5. The Golden Rule: Rebalance Annually

Market movements will naturally “drift” your portfolio. If stocks have a great year, they might grow to represent 80% of your portfolio when your target was 60%.

Rebalancing involves selling a portion of your winners and buying more of your underperformers. It feels counterintuitive, but it is the most disciplined way to “buy low and sell high” while maintaining your risk profile.

Partner With a Professional to Secure Your Future

Navigating the complexities of the 2026 financial landscape requires more than just a “buy and hold” mentality—it requires a strategic partner who understands the nuance of modern market cycles. With years of experience specializing in retirement glide paths and tax-efficient wealth preservation, I help investors bridge the gap between their current savings and their long-term lifestyle goals. Whether you are looking to optimize your ETF selection or need a rigorous rebalancing strategy tailored to your specific risk tolerance, my evidence-based approach ensures your portfolio remains resilient against volatility. Let’s move beyond the guesswork and build a data-driven roadmap for your retirement together.

Click below “Contact Me” to start our discussion today!

Important: The information and opinions in this article are for general information purposes only. They should not be relied on as professional financial advice. Readers should seek unbiased financial advice that is customised to their specific financial objectives, situations & needs. This advertisement or publication has not been reviewed by the Monetary Authority of Singapore.

Kenny Loh is a distinguished Wealth Advisory Director with a specialization in holistic investment planning and estate management. He excels in assisting clients to grow their investment capital and establish passive income streams for retirement. Kenny also facilitates tax-efficient portfolio transfers to beneficiaries, ensuring tax-efficient capital appreciation through risk mitigation approaches and optimized wealth transfer through strategic asset structuring.

In addition to his advisory role, Kenny is an esteemed SGX Academy trainer specializing in S-REIT investing and regularly shares his insights on MoneyFM 89.3. He holds the titles of Certified Estate & Legacy Planning Consultant and CERTIFIED FINANCIAL PLANNER (CFP).

With over a decade of experience in holistic estate planning, Kenny employs a unique “3-in-1 Will, LPA, and Standby Trust” solution to address clients’ social considerations, legal obligations, emotional needs, and family harmony. He holds double master’s degrees in Business Administration and Electrical Engineering, and is an Associate Estate Planning Practitioner (AEPP), a designation jointly awarded by The Society of Will Writers & Estate Planning Practitioners (SWWEPP) of the United Kingdom and Estate Planning Practitioner Limited (EPPL), the accreditation body for Asia.

罗国强(Kenny Loh) 是一位杰出的财富咨询总监,专长于综合投资规划与遗产管理。他擅长协助客户实现投资资本增值,并建立退休被动收入来源。同时,他通过税务优化的方式帮助客户将投资组合高效转移给受益人,运用风险缓释策略确保资本增值的税务效率,并通过战略性资产配置实现财富传承的最优化。

除咨询工作外,罗国强是新加坡交易所学院(SGX Academy)的特聘讲师,专注于新加坡房地产投资信托(S-REIT)投资领域,并定期在MoneyFM 89.3电台分享专业见解。他拥有认证遗产与传承规划顾问(Certified Estate & Legacy Planning Consultant)及国际认证财务规划师(CFP)资格。

在逾十年的综合遗产规划经验中,他独创“遗嘱、持久授权书与备用信托三合一”解决方案,兼顾客户的社会责任、法律义务、情感需求及家庭和谐。他持有工商管理硕士与电气工程硕士双学位,并获英国遗嘱撰写及遗产规划从业者协会(SWWEPP)与亚洲认证机构遗产规划从业者有限公司(EPPL)联合授予副遗产规划从业师(AEPP)专业资格。

Arrange for a non-obligatory one-to-one free consultation here!

立即预约免费一对一咨询(无需承担任何义务)!