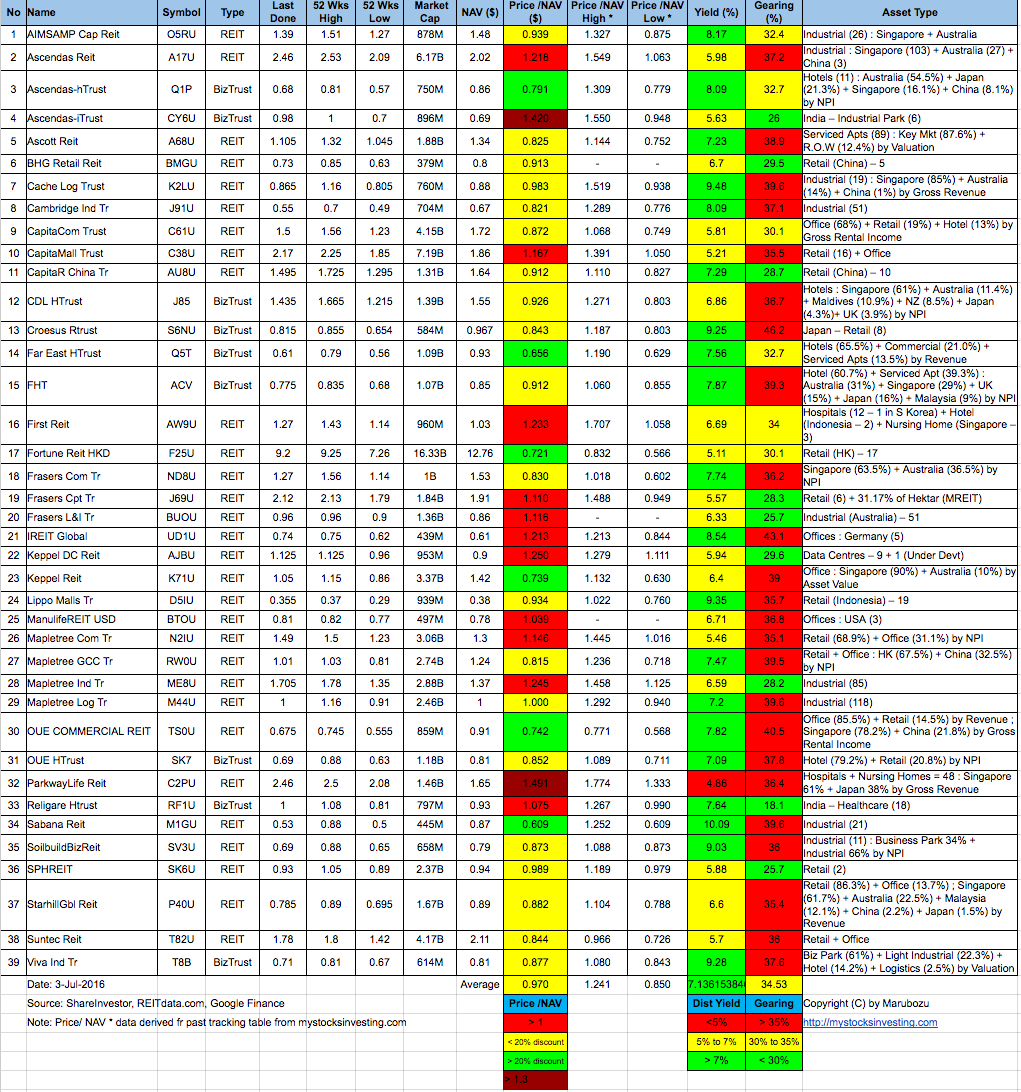

Singapore REIT Fundamental Analysis Comparison Table – 8 August 2016

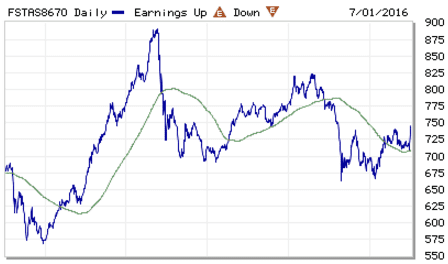

FTSE ST Real Estate Investment Trusts (FTSE ST REIT Index) increases from 745.33 to 756.17 (+1.45%) compare to last post on Singapore REIT Fundamental Comparison Table on July 3, 2016. The index broke out from Rectangle consolidation chart pattern and is currently forming a “Higher High, Higher Low” uptrend chart pattern. 200D SMA also starts to trend upward. This is the bullish sign and technically Singapore REIT sector is in bullish territory. SGX S-REIT (REIT.SI) Index increases from 1141.99 to 1162.02 (+1.05%)

- Price/NAV increases from 0.97 to 1.003 (Singapore Overall REIT sector at FAIR value now)

- Distribution Yield decreases from 7.14% to 6.96% (take note that this is lagging number). More than half of Singapore REITs (19 out of 39) have Distribution Yield > 7%. Current yield is attractive (for certain REITs only) but it is dangerous to make investing decision purely base on the yield. Past performance does NOT equal to future performance.

- Gearing Ratio decreases from 34.53% to 34.50%. 20 out of 39 have Gearing Ratio more than 35%.

- Most overvalue is Ascendas iTrust (Price/NAV = 1.585), followed by Parkway Life (Price/NAV = 1.524).

- Most undervalue (base on NAV) is Sabana REIT (Price/NAV = 0.65), followed by Far East HTrust (Price/NAV = 0.656) and Keppel REIT (Price/NAV = 0.752).

- Higher Distribution Yield is Sabana REIT (9.52%), followed by VIVA Industrial Trust (9.51%) followed by Soilbuild Biz REIT (9.27%)

- Highest Gearing Ratio is Croesus Retail Trust (46.2%), iREIT Global(43.1%) and OUE Commercial Trust (40.2%)

Disclaimer: The above table is best used for “screening and shortlisting only”. It is NOT for investing (Buy / Sell) decision. To learn how to use the table and make investing decision, Sign up next REIT Investing Seminar here to learn how to choose a fundamentally strong REIT for long term investing for passive income generation.

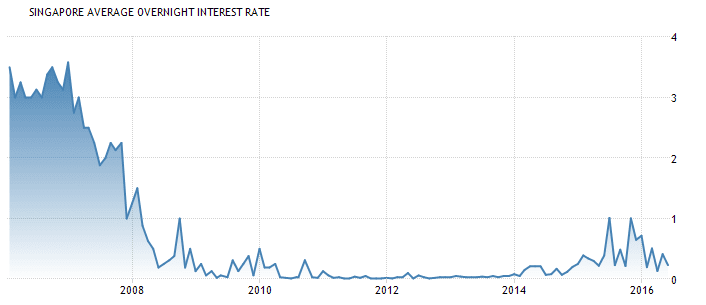

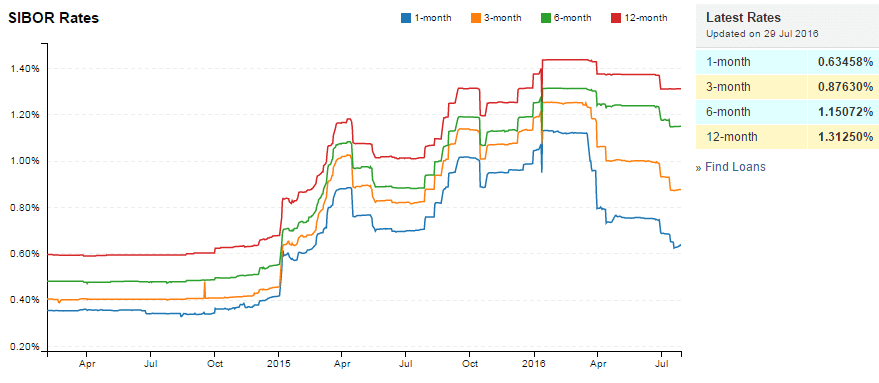

- Singapore Interest Rate increases from 0.23% to 0.37%

- 1 month decreases 0.75000% to 0.63458%

- 3 month decreases from 0.99463% to 0.87630%

- 6 month decreases from 1.23466% to 1.15072%

- 12 month decreases from 1.37375% to 1.31250%

The Singapore PMI decreased to 49.3 in July of 2016 from 49.6 in the previous month, as sluggish global demand continued to weigh on the economic performance. The reading pointed to the thirteenth consecutive month of contraction, as new orders fell further to 49.0 (from 49.2 in June), new exports orders declined to 48.8 (from 48.9 in June) and output went down to 49.3 (from 49.4 in June). Manufacturing PMI in Singapore averaged 50.13 from 2012 until 2015, reaching an all time high of 51.90 in October of 2014 and a record low of 48.30 in October of 2012. Manufacturing PMI in Singapore is reported by the Singapore Institute of Purchasing & Materials Management, SIPMM.

Fundamentally Singapore REITs in general, the valuation is at Fair Value but distribution yields are still attractive. Technically Singapore REITs sector is in bullish territory and on uptrend. US Fed may delay the interest rate hike as there are a lot of uncertainties due to Brexit. This may probably be the reason why Singapore REIT is coming back to life again! Come and Learn How to Find Good Value Singapore REIT steps by steps to Invest at Singapore REITs Investing class.

Original post from https://mystocksinvesting.com