Welcome to Kenny Loh Holistic Legacy Planning. Securing your family’s future is a journey, not a single transaction. As a certified estate planner, I provide a comprehensive, four-step approach designed to organize your wealth, protect your beneficiaries, and ensure your legacy is passed on exactly as you intend.

Here is the holistic process we will navigate together:

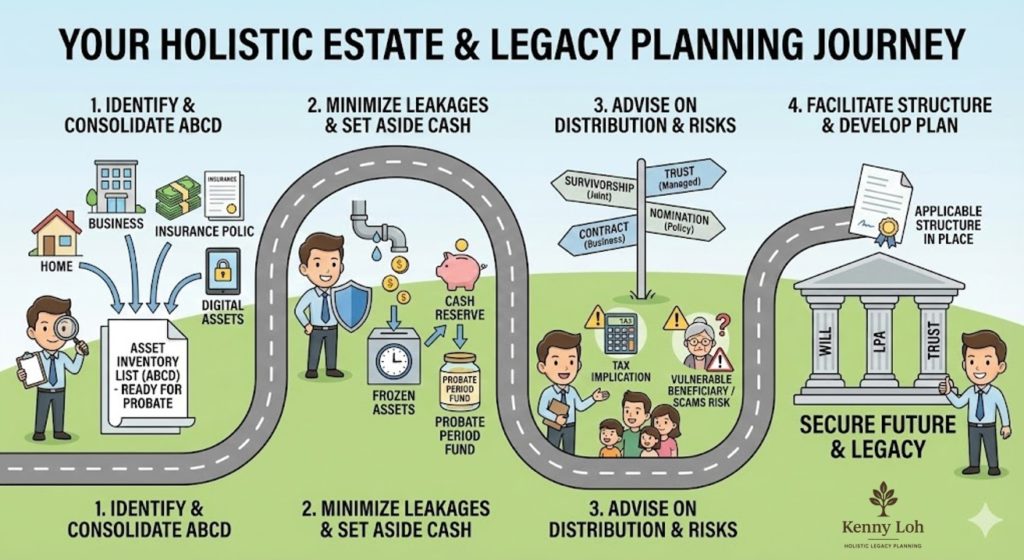

Step 1: Identify & Consolidate Your Assets (The ‘ABCD’)

Our journey begins with clarity. We work together to conduct a thorough examination of your entire financial landscape. This involves identifying and consolidating all asset types, often referred to as the ‘ABCD’ of your estate: your physical Assets (like your home), Business interests, Cash and Insurance policies, and increasingly important Digital Assets.

My goal during this phase is to help you create a comprehensive “Asset Inventory List”. By having this list organized and “Ready for Probate,” we significantly reduce the administrative burden and confusion for your executors in the future.

Step 2: Minimize Leakages & Ensure Liquidity

A common challenge during estate administration is that assets can become temporarily “frozen” while legal processes take place. Without proper planning, this can leave your loved ones without access to funds when they need them most.

In this step, we develop strategies to act as a shield, minimizing potential estate value leakages. Crucially, we plan to set aside a dedicated “Cash Reserve” to serve as a “Probate Period Fund,” ensuring immediate liquidity is available to bridge the gap while other assets are frozen.

Step 3: Advise on Distribution Methods & Assess Risks

Determining how your assets are transferred is vital. I will advise you on the various distribution channels available and which best suit your specific assets and goals. These methods may include Joint Survivorship, managed Trusts, Business Contracts, or Policy Nominations.

This phase also involves a critical risk assessment. We will examine potential tax implications of your distribution plan. Furthermore, we will address the human element by highlighting potential risks, such as protecting vulnerable beneficiaries who may not be financial literate or are at risk of falling victim to scams.

Step 4: Facilitate Structure & Develop the Plan

The final stage is bringing your customized plan to life by building the necessary legal foundation. I facilitate the development of the applicable structures tailored to address your unique needs.

This involves implementing the core pillars of a robust estate plan, which typically include a Will, a Lasting Power of Attorney (LPA), and Trusts. With the correct structure in place, you gain the peace of mind that comes with a secure future and a well-protected legacy.

Ready to begin your Holistic Estate & Legacy Planning Journey? Contact Kenny Loh today.

Readers should seek independent, unbiased financial advice that is customised to their specific financial objectives, situation, and needs. This publication has not been reviewed by the Monetary Authority of Singapore.

The narrative for 2026 is one of recovery and transition. After two years of “restrictive” interest rates, the sector is entering what analysts call a two-year earnings upgrade cycle (2026–2027). 3 Key Turning Points Below:

Rate Cut Impact: With the US Fed and domestic 3M SORA rates projected to settle around 1.2%–1.3% in 2026, the “cost-of-debt” drag is finally reversing.

Dividend Uplift: Markets are forecasting low single digit uplift in DPU (Distribution Per Unit) as REITs replace maturing high-interest loans with cheaper financing.

Price Potential: I anticipate a potential 10-15% price upside across the sector as yields normalize and the spread over Singapore 10-year government bonds remains healthy (approx. 3.7–3.9 percentage points).

2. Refinancing Risks & Management

While the outlook is positive, the “refinancing wall” remains a hurdle for those with poor capital structures.

Most Exposed: Watch REITs with gearing ratios above 40% or those with significant debt maturing in early 2026.

High Risk: Manulife US REIT (56% Gearing) and Prime US REIT (US office exposure) – 46% Gearing and EC World REIT (71% Gearing) continue to face structural gearing challenges.

Management Strategies:

Fixed-Rate Hedging: REITs probably will start reducing the percentage of fixed rate hedge to ride on the immediate impact of lower interest rate. Leaders like Frasers Centrepoint Trust (FCT) have over 80% of their debt on fixed rates with 3.2 Years WADM, is unlikely to have huge and surprise uplift in term of DPU.

Asset Recycling: REITs are divesting non-core assets to pay down debt.

Proactive Refinancing: Many are securing “green loans” early to lock in sustainability-linked discounts.

3. Which property sub-sectors (e.g., industrial, retail, office, hospitality, data centers, healthcare) do you believe have the strongest fundamentals and growth prospects for 2026, and which remain challenged?

Sub-Sector

2026 Outlook

Key Fundamentals

Industrial / Data Centers

Strongest

Driven by AI, cloud computing, and supply chain resilience. High rental reversions.

Suburban Retail

Defensive

High occupancy (~98%) and “necessity spending” keep cash flows stable.

Healthcare

Stable

Master leases with 20+ year terms (e.g., ParkwayLife) provide “inflation-proof” income.

Hospitality

Growth

Tourism recovery and higher room rates (RevPAR) support a 2026 rebound.

Office

Challenged / Mixed

Central Singapore is resilient, but US and China office markets remain under pressure from high vacancies, due to layoff and job obsolescence driven by wide adoption of AI in next 2 years.

4. Valuations: Is it an Entry Point?

Yes, for long-term investors.

Price-to-NAV: The S-REIT sector is trading at roughly 0.86 P/NAV, which is below the 10-year average of 1.0x with 5.4% DPU Yield

Caution vs. Opportunity: While the market is no longer “dirt cheap” compared to 2023, it is currently “fairly valued to slightly undervalued.” The market has likely priced in some caution regarding global growth, leaving room for surprises on the upside if rate cuts are more aggressive than expected.

Not all the REITs are cheap now:

CICT is trading at +2 standard deviation of 5 Years Average P/NAV.

Keppel DC REIT is trading slightly below 5 Years Average P/NAV.

Frasers Centerpoint is trading at fair value of 5 Years Average P/NAV.

Digital Core REIT is trading at -1 standard deviation of 3 Years Average P/NAV.

5. Primary Downside Risks

Beyond interest rates, the “Gray Swans” for 2026 include:

Slower Economic Growth: Singapore’s GDP is projected to moderate to 1.0%–3.0%, which could dampen tenant demand.

Trade & Geopolitics: Potential US tariff policies and trade tensions could impact industrial/logistics REITs tied to global trade.

Consumer Sentiment: If inflation remains sticky, discretionary spending in high-end retail (like Orchard Road) may soften, even as suburban malls stay strong.

6. Recommended Strategy: The “Barbell” Approach

For a retail investor in 2026, a Balanced Approach is safest:

The Core (60-70%): Focus on Defensive Income. Look for blue-chip REITs with high-pedigree sponsors (CapitaLand, Frasers, Mapletree). DPU Yield Between 4-5%.

The Satellite (30%): Chase Structural Growth in Data Centers or recover-themed such as Hospitality REITs, REITs with oversea portfolio to capture capital appreciation as rates fall.

S-REITs on the “Watchlist” (2026 Selection)

CapitaLand Integrated Commercial Trust (CICT): The “blue chip” for core stability.

Keppel DC REIT: To play the AI and digital infrastructure theme.

Frasers Centrepoint Trust (FCT): Best-in-class for defensive suburban retail.

ParkwayLife REIT: For long-term, recession-proof healthcare income.

United Hampshire US REIT: A US Retail Grocery Malls which trading at discount and attractive DPU yield of 8%, relatively short WADM of 1.6 years.

Kenny Loh is a distinguished Wealth Advisory Director with a specialization in holistic investment planning and estate management. He excels in assisting clients to grow their investment capital and establish passive income streams for retirement. Kenny also facilitates tax-efficient portfolio transfers to beneficiaries, ensuring tax-efficient capital appreciation through risk mitigation approaches and optimized wealth transfer through strategic asset structuring.

In addition to his advisory role, Kenny is an esteemed SGX Academy trainer specializing in S-REIT investing and regularly shares his insights on MoneyFM 89.3. He holds the titles of Certified Estate & Legacy Planning Consultant and CERTIFIED FINANCIAL PLANNER (CFP).

With over a decade of experience in holistic estate planning, Kenny employs a unique “3-in-1 Will, LPA, and Standby Trust” solution to address clients’ social considerations, legal obligations, emotional needs, and family harmony. He holds double master’s degrees in Business Administration and Electrical Engineering, and is an Associate Estate Planning Practitioner (AEPP), a designation jointly awarded by The Society of Will Writers & Estate Planning Practitioners (SWWEPP) of the United Kingdom and Estate Planning Practitioner Limited (EPPL), the accreditation body for Asia.

If you need any financial advice, please contact kennyloh@fapl.sg

As an SME owner, you’ve spent years—perhaps decades—building your business from the ground up. You’ve weathered market shifts, hiring challenges, and economic crashes. But there is one risk that most founders keep on the back burner, even though it’s the single biggest threat to their legacy: BusinessSuccession Planning.

A recent article in The Business Times highlighted a sobering reality that I see far too often in my work as a legacy and estate planner: When a founder delays succession planning, the business doesn’t just stall—it bleeds value.

If you aren’t there tomorrow, what happens to your business in the first 90 days? That window usually decides whether your company survives for the next generation or becomes a cautionary tale.

The 5 Immediate Risks of “Waiting Until Later”

When a founder passes away or becomes incapacitated without a structured plan, five things tend to happen simultaneously, creating a “perfect storm” for the business:

The Cashflow Freeze: Shares and personal assets often get locked in probate for months. While your accounts are frozen, your obligations aren’t. Payroll, suppliers, and bank loans remain due. Many businesses simply don’t have the liquidity to survive this window.

Operational Legal Limbo: Without a clear successor or legal authority, the “engine room” stops. Bank mandates stall, new contracts can’t be signed, and existing clients may hesitate to renew, fearing the business is unstable.

Internal Disputes: In the absence of a written roadmap, even the most tight-knit families and business partners can fall into conflict. When no one knows the “right” way forward, decision-making becomes paralyzed.

Forced Sales and Control Loss: If surviving partners want to keep the business but can’t afford to buy out your deceased estate’s stake, they may be forced to bring in external buyers. This leads to “value leakage” and a loss of the original vision.

The Fire Sale: Without trusts or structured liquidity, a lifetime of work is often liquidated at a fraction of its true worth just to cover taxes or immediate debts.

How We Replace Chaos with Structure

My role as a Business Succession and Legacy Planner is to ensure that your business is an “evergreen” asset—one that can thrive independently of your day-to-day presence. We achieve this by addressing each risk factor with a concrete, legal, and financial solution.

To combat Asset Freezes, we establish immediate liquidity strategies—often through specialized insurance or business trusts—to ensure payroll and bills are met from Day 1. To solve Legal Limbo, we create clear governance frameworks and Power of Attorney structures so authority is transferred instantly and legally, keeping operations seamless.

When it comes to Partner Conflict, I facilitate and draft funded Buy-Sell Agreements. This ensures surviving partners have the immediate cash to buy out shares at a fair, pre-agreed price, preventing messy disputes. Finally, to prevent Legacy Erosion, we use trusts and estate structuring to ensure your family is provided for financially without the business needing to be dismantled or sold off to pay them out.

Preliminary Succession Risk Assessment

Are you prepared? Take a moment to answer these four questions honestly. If you answer “No” or “I’m not sure” to any of them, your business is currently at risk.

Liquidity: If you passed away tomorrow, does the business have a dedicated source of cash (separate from frozen bank accounts) to pay staff and suppliers for at least 3 to 6 months?

Authority: Is there a legal document currently in place that grants a specific person the immediate right to sign contracts and manage bank accounts in your absence?

The Buy-Out: If you have business partners, is there a legally binding agreement—and a dedicated fund—to buy out your shares so your family gets the cash and the partners keep the business?

Family Harmony: Have you sat down with your heirs and partners to document exactly who will lead and who will own the shares, or is it “assumed” everyone will just figure it out?

Secure Your Legacy Today

Business succession planning isn’t about “leaving” your business; it’s about strengthening it. It’s about ensuring that the values, culture, and financial success you’ve built can endure for decades to come.

Don’t leave your life’s work to chance or the slow grind of the probate courts. I specialize in helping SME owners navigate these complex emotional and financial waters to create a bulletproof estate and succession strategy.

Important: The information and opinions in this article are for general information purposes only. They should not be relied on as professional financial advice. Readers should seek unbiased financial advice that is customised to their specific financial objectives, situations & needs. This advertisement or publication has not been reviewed by the Monetary Authority of Singapore.

Kenny Loh is a distinguished Wealth Advisory Director with a specialization in holistic investment planning and estate management. He excels in assisting clients to grow their investment capital and establish passive income streams for retirement. Kenny also facilitates tax-efficient portfolio transfers to beneficiaries, ensuring tax-efficient capital appreciation through risk mitigation approaches and optimized wealth transfer through strategic asset structuring.

In addition to his advisory role, Kenny is an esteemed SGX Academy trainer specializing in S-REIT investing and regularly shares his insights on MoneyFM 89.3. He holds the titles of Certified Estate & Legacy Planning Consultant and CERTIFIED FINANCIAL PLANNER (CFP).

With over a decade of experience in holistic estate planning, Kenny employs a unique “3-in-1 Will, LPA, and Standby Trust” solution to address clients’ social considerations, legal obligations, emotional needs, and family harmony. He holds double master’s degrees in Business Administration and Electrical Engineering, and is an Associate Estate Planning Practitioner (AEPP), a designation jointly awarded by The Society of Will Writers & Estate Planning Practitioners (SWWEPP) of the United Kingdom and Estate Planning Practitioner Limited (EPPL), the accreditation body for Asia.

If you need any financial advice, please contact kennyloh@fapl.sg