Singapore REITs 2026 Market Outlook

(1) Review of 2025 Singapore REITs Performance (The Wrap-Up)

Key Takeaway: A Strong Rebound driven by rate stabilization and the start of SORA decline.

- Overall Performance: 2025 is shaping up to be the best year for S-REITs since 2019, with total returns (price gain + dividend) projected to be around 12-15% YTD (as of Dec 2025). This marks a significant rebound from the challenging high-rate environment of 2023/2024.

- Driver: The primary catalyst has been the stabilisation and decline of borrowing costs. The 3-month Compounded SORA in Singapore has trended down (e.g., from a peak near 4.5% to around $1.28% by late 2025), significantly easing the refinancing burden.

- Fundamental Stability: Most S-REITs demonstrated stable operating performance in 2025, with resilient occupancy rates and positive rental reversions across Retail, Industrial, and Office sectors.

- Valuation: Despite the price recovery, the sector is generally still trading at an attractive valuation, with the average P/NAV (Price-to-Net Asset Value) around 0.85 (simple average) and a trailing 12-month yield around 5.5%.

(2) Projected US and Singapore Interest Rates

Key Takeaway: The “Lower-for-Longer” narrative is shifting to a rate-cutting cycle, providing a strong tailwind for 2026.

| Rate Benchmark | 2025 Year-End Estimate | 2026 Outlook (Consensus) | Impact on S-REITs |

| US Fed Funds Rate | 3.50% – 3.75% (Following cuts in late 2025) | Further cuts expected in H1 2026, reaching a terminal rate potentially in the 3.00% – 3.25% range end of 2026. | Drives global capital flows and sentiment. Lower US rates support global growth and ease the cost of capital for S-REITs with US/overseas assets. |

| Singapore Interest Rate (SORA) | 1.25% – 1.50% (3-months) | Expected to remain low and stable or track further down as US rates ease and global liquidity improves. | Directly lowers the cost of debt for S-REITs, which directly translates to DPU savings. Will benefit S-REITs with borrowing in SGD. |

(3) How the Interest Rate Shift Will Affect REIT DPU and Valuation

Key Takeaway: Lower rates are the most significant positive catalyst for DPU and valuation compression in 2026.

- Direct Impact on DPU (Distribution Per Unit):

- Lower SORA/cost of debt directly reduces interest expense for REITs with floating-rate debt or upcoming refinancing. This saving is immediately accretive to Distributable Income and, thus, DPU.

- Analysts have noted that even a 25-50 basis point decline in debt cost can visibly improve DPU for REITs with shorter debt maturity profiles.

- Unlikely for all the REITs to benefit fully from the interest rate cut as majority of the REITs have extend the debt maturity profile with higher fixed rate previously. Only REITs with shorter WADM (Weighted Debt Maturity Profile) and low percentage of fixed rate will benefit the most.

- Indirect Impact on Valuation (NAV):

- Yield Compression: As bond yields fall, the required yield on S-REITs becomes less competitive. Investors shift from lower-risk bonds to REITs for yield, driving up REIT prices. This narrows the Yield Spread (REIT Yield minus Government Bond Yield).

- Capitalisation Rates: Lower borrowing costs are expected to lead to a compression of cap rates in the private real estate market, driving up the valuation of the physical properties (Net Asset Value – NAV), especially for prime assets. This will support the REIT’s share price and P/NAV ratio.

- Historical Parallel: Historically, REITs have often performed strongly in the 12 months following the commencement of an easing cycle, as lower rates enhance their appeal as an income-generating asset.

(4) Key Financial Ratios for REIT Selection in 2026

Given the shift in the interest rate cycle, investors should focus on ratios that signal stability and capacity for growth.

| Ratio | Rationale for 2026 Selection | Current MAS Guideline/Target |

| Gearing Ratio (Aggregate Leverage) | Indicates debt capacity for accretive acquisitions. Lower is safer in a volatile market. | <50% (Regulatory Limit) |

| Interest Coverage Ratio (ICR) | Measures the ability to service interest payments from earnings. Must be high enough to satisfy MAS requirements if gearing is close to the limit. | >1.5x (New MAS threshold) |

| Weighted Average Lease Expiry (WALE) | Predictability of income stream. Longer WALE (e.g., >3.5$ years) signals stable cash flow, favoured in a transition period. | N/A |

| Price-to-NAV (P/NAV) | Valuation metric. REITs trading at a significant discount (P/NAV < 1.0) with strong fundamentals may offer the greatest capital upside as valuations recover. However, some REITS always traded at premium or discount. Thus, it is important to compare the current P/NAV with the historical P/NAV range. | N/A |

| Distribution Yield Spread | Measures REIT yield relative to the Singapore 10Y Government Bond. Wider spread suggests better value proposition compared to risk-free assets. | N/A |

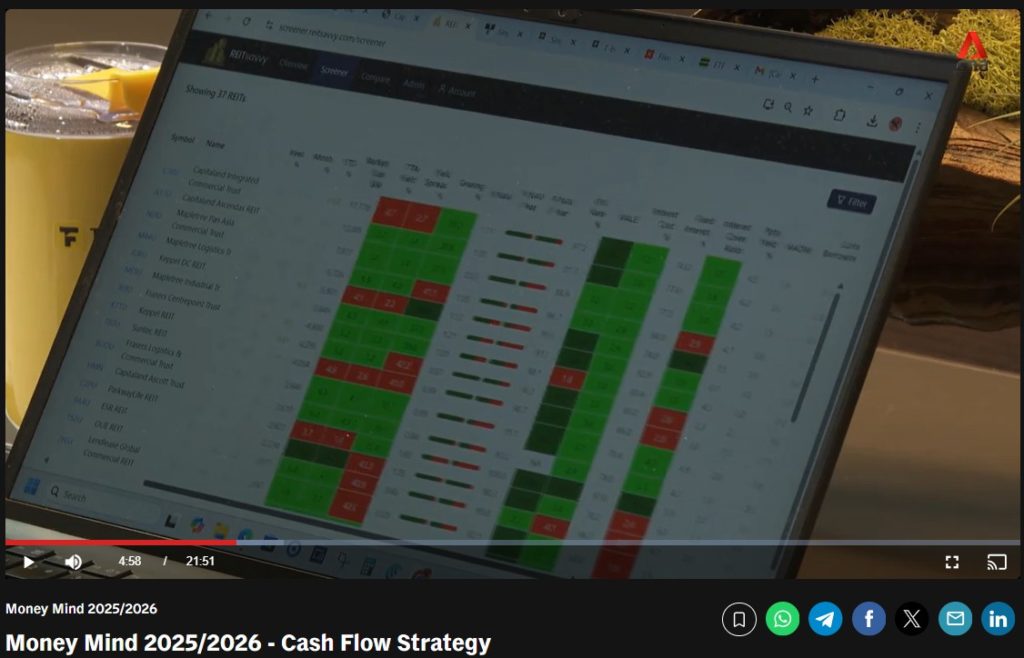

REITs ranked by the highest WALE (Source: REITsavvy.com)

REITs ranked by the highest Interest Coverage Ratio (Source: REITsavvy)

Expect Improvement in Gearing (decreased) and ICR (increase) for S-REITs in 2026 (Source: REITSavvy Overview)

(5) Sector Outlook

Key Takeaway: Industrial (Data Centre/Logistics) and Suburban Retail are positioned for continued strength, while Hospitality sees growth from tourism.

| Sector | Outlook for 2026 | Key Drivers / Headwinds |

| Industrial (Logistics/Data Centre) | Strongest Outlook. Structural growth and positive rental reversions. | Driven by e-commerce, AI adoption, and resilient demand for logistics. Data Centres are favoured for long-duration leases and secular growth. |

| Retail (Suburban) | Resilient. Positive rental reversions and strong footfall. | Supported by necessity spending, resilient domestic consumption, and limited new supply. |

| Office | Stable but Divergent. Prime CBD assets in Singapore remain resilient. US Commercial Office may see bottom and rebound with lower interest rate. | Flight to quality: High occupancy for modern, premium assets in core areas. Pressure on older, non-core assets. May see re-rating of the valuation of US commercial office. Probable resumption of dividend for US Office REITs. |

| Hospitality | Growth Recovery. Benefits from continued post-pandemic tourism boom. | Strong RevPAR (Revenue Per Available Room) growth driven by recovering international visitor arrivals. |

| Healthcare | Defensive/Stable. Long-term leases with rent escalations provide DPU stability. | Driven by aging demographics and defensive nature of the assets. Lower yields reflect lower risk profile. |

(6) Wrap Up: Summary of Outlook 2026

- The Pivot Year: 2026 is expected to be a pivotal recovery year for S-REITs, transitioning from a survival phase to a growth phase, primarily driven by a more accommodative lower interest rate environment.

- DPU Inflection: We expect DPU growth to inflect upwards for the sector as lower interest expenses translate directly to distributable income.

- The New Mantra: Investors should focus on Quality, Balance Sheet Strength, and Sector Exposure to secular growth trends (Data Centres, Logistics, Suburban Retail).

- Actionable Strategy: S-REITs are poised to be an attractive income play, with a potential to deliver both stable yield and capital appreciation as market valuations converge with private asset values.

Kenny Loh is a distinguished Wealth Advisory Director with a specialization in holistic investment planning and estate management. He excels in assisting clients to grow their investment capital and establish passive income streams for retirement. Kenny also facilitates tax-efficient portfolio transfers to beneficiaries, ensuring tax-efficient capital appreciation through risk mitigation approaches and optimized wealth transfer through strategic asset structuring.

In addition to his advisory role, Kenny is an esteemed SGX Academy trainer specializing in S-REIT investing and regularly shares his insights on MoneyFM 89.3. He holds the titles of Certified Estate & Legacy Planning Consultant and CERTIFIED FINANCIAL PLANNER (CFP).

With over a decade of experience in holistic estate planning, Kenny employs a unique “3-in-1 Will, LPA, and Standby Trust” solution to address clients’ social considerations, legal obligations, emotional needs, and family harmony. He holds double master’s degrees in Business Administration and Electrical Engineering, and is an Associate Estate Planning Practitioner (AEPP), a designation jointly awarded by The Society of Will Writers & Estate Planning Practitioners (SWWEPP) of the United Kingdom and Estate Planning Practitioner Limited (EPPL), the accreditation body for Asia.

You can join his Telegram channel #REITirement – SREIT Singapore REIT Market Update and Retirement related news. https://t.me/REITirement