Money & Me: Further Interest Rate Hikes, FHT’s failed Privatization bid

16 September 2022

Money and Me: What could unitholders responsible for FHT’s failed privatisation bid be holding out for?

Frasers Hospitality Trust, suffered a 24 percent dip in share prices after a $1.35 billion proposal to take the trust private fell through.. The privatisation offer seemed generous enough,– at a 7 per cent premium to net asset value (NAV) But earlier this week, the global hotel and serviced residence trust clocked in 74.88 percent of shareholder votes who were in favour of the proposal, narrowly missing the 75 per cent needed for the resolution to pass. Many market watchers were surprised including our guest Kenny Loh, REIT Specialist and Independent Financial Advisor.

We find out why and ask if hospitality Reits listed in Singapore – which have seen a remarkable revival in fortunes- can continue their march forward. Michelle Martin and Kenny Loh also take a closer look at the S-reit landscape month-on-month performance across sectors.

The article version (transcribed) of the interview can be found below.

Transcription:

Introduction

We’re surveying the REIT universe. Frasers Hospitality Trust suffered a 24% dip in its share price, after a 1.35 billion proposal to take the trust private fell even though the offer seemed generous. Cash offering of 70 cents per stapled security, a 7% premium to its net asset value by sponsor Fraser’s Property.

But the global hotel and service resident clocked in 74.88% of shareholder votes, just missing 75% that it needed for that resolution to pass. So we’ll take a closer look at that. Also scanning Mapletree Pan Asia commercial trust, seeing a bullish call by DBS on its share price. And in just a while, we’ll also take a look at Parkway Life REIT and their move to further expand their Healthcare REITs portfolio over in Japan.

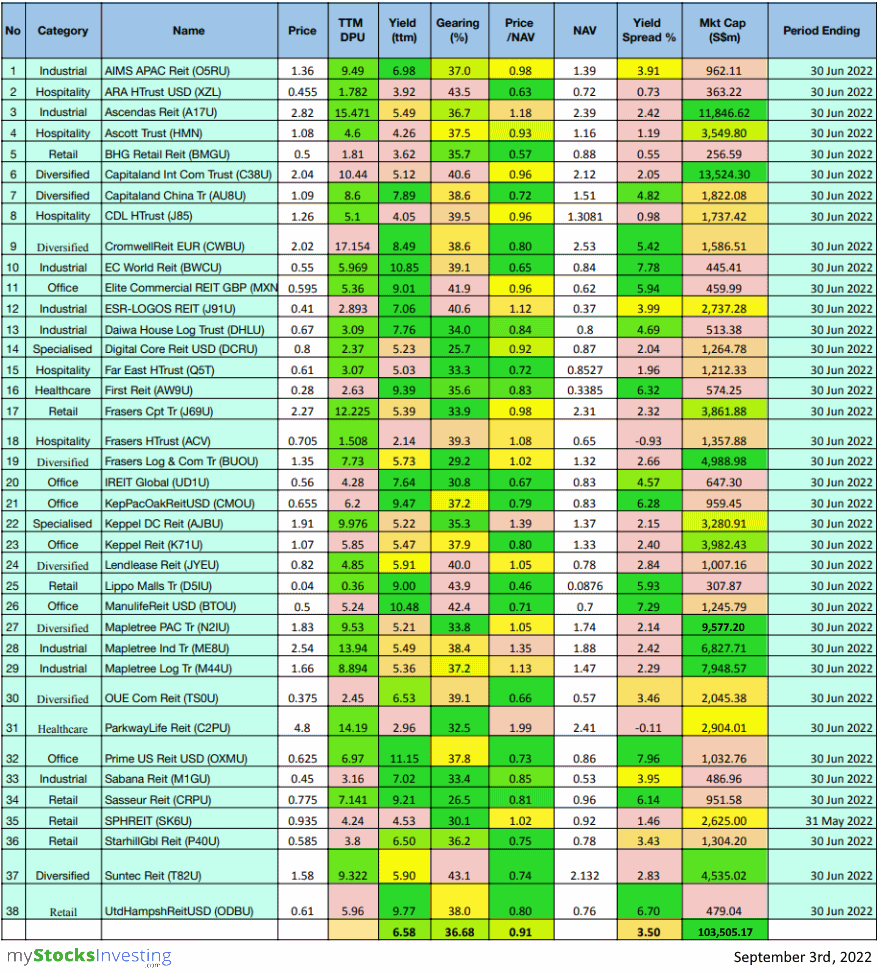

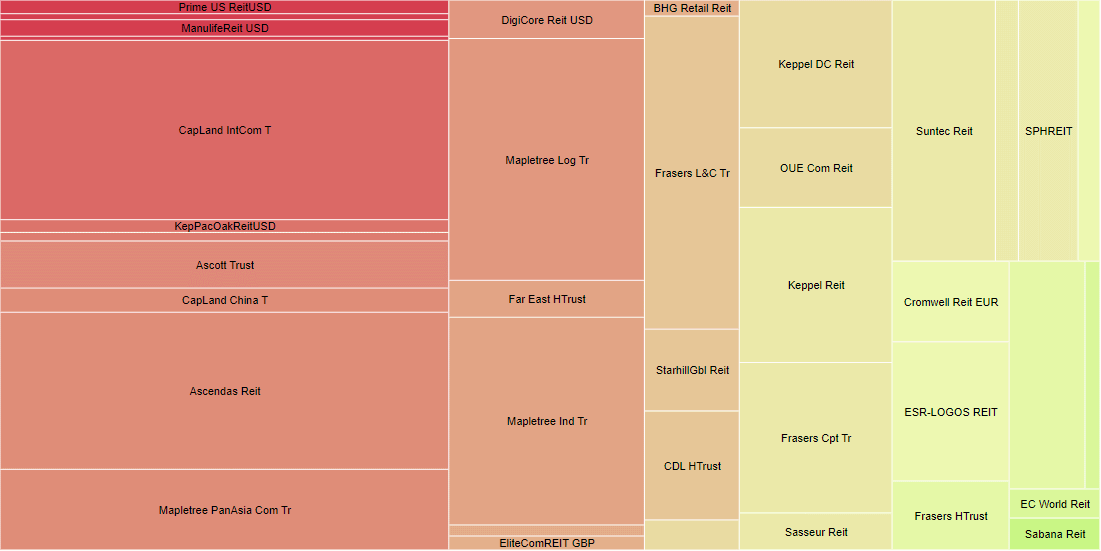

Q. Can you give us a sense of an overview of how REITs have performed the past month? I understand that the year’s best performers are hospitality trusts and the worst performers are REITs with 100% overseas assets.

Right based on the latest month of performance, actually, there’s a sell off across the board for the whole REIT universe in Singapore. And based on last week, with inflation data coming out, there was a sell off in the US Stock market, and Singapore REITs are not spared too. And if we are looking at a whole index itself, the REIT index is really forming some sort of bearish chart pattern, the falling wedge. This I don’t like as an investor, as the breaking down the support of this may result in a larger sell off of the Singapore itself.

So, last month was a pretty bad month for Singapore REITs. And at a present moment, the REIT index is holding at the critical support level.

Q. For the failed Frasers Hospitality Trust privatisation bid, why do you think unitholders rejected this privatisation bid, despite the attractive offer?

I was surprised unitholders rejected this privatization. I thinkthe offer is pretty good based on past performance. I think why the unit holder they rejected the offer, I think is all down to the price. Because if you look at a price chart, historically Frasers Hospitality Trust used to trade between 63 cents to 86 cents.

And close to 70% of the time, they are trading above 70 cents value, which means that most investors who invested in Fraser Hospitality Trust, basically they’re losing money. And coupled with a dividend, maybe some of them probably would breakeven with the share price and also the dividend from a total return perspective.

So I think that mainly on a price perspective, but however, It is actually a narrow miss of 75% mark because the 74.88% who voted for the prioritization is only 0.12%, which a small number. So I think that with the adjustment of the share price during the next attempt, probably you’ll swing these unitholders to vote for the privatisation.

Q. What would privatization mean for unitholders of FHT?

There are two scenarios. One scenario is a privatisation does not go through. Based on the current portfolio, I think there are a lot of challenges for FCT to turn around because there will be too much uncertainty, e.g. Rate hike and inflation. Also by looking at their debt portfolio they may have to face the refinancing risk pretty soon, because they currently have a high gearing ratio of 39.3%. And at the same time, they have a decreasing DPU trend, even during pre-COVID. So is the NAV/Unit value.

This means that fundamentally, I think the current portfolio is not a fundamentally strong portfolio. Coupled with all these uncertainties, if shareholders continue to hold onto FHT and FHT faces refinancing risks, they will then have to issue additional rights. And that will further dilute the DPU and also the share price. Although the sentiment in the Hospitality REITs recovery is good, there are better choices out there.

For example, CDL Hospitality Trusts, Far East Hospitality Trust and Ascott Residence Trust. If you look at the offering price itself, they are offering 1.07 times of the NAV (book value), which is pretty high at the present moment. Ascott is only trading at 0.94, FEHT at 0.7 and CDLHT at 0.97. The principal is much higher than those relatively better Hospitality trusts out there.

Q. What are the possible headwinds for FHT that you see?

One would be the continual decrease of DPU. The other possible concern would be the resurgence of COVID around the world, which will dent the hospitality sector. And at the present moment, the ICR is also pretty low. I may have a concern that they may turn out to be the next Eagle Hospitality Trust, where they are not able to pay the dividends.

Q. Mapletree Pan Asia Commercial Trust is trading at a yield aboe 5%, at $0.89, with a bullish call by DBS. Do you think MPACT’s valuation is attractive right now?

I do agree with the DBS call because if you look at the present price to book value, it is trading below or close to minus one standard division of the five year average. In other words, it’s undervalued. And if you look at the forward earnings and the forward DPU, the forward DPU is expected to rise.

2 reasons: one attributed to the future easing of restrictions for Hong Kong and China. Eventually China will ease COVID restrtctions. And Festival Walk, one of the famous retail malls in Hong Kong, definitely will be benefit from this reopening and reduction on quarantine measures. Festival Walk contributed 21% of MPACT’s NPI. So a reopening of a China will help, uh, Hong Kong itself.

And at the same time, also we will help Singapore because right now we have very few Chinese tourists coming to Singapore due to all the restrictions. When the borders reopen, there’ll be revenge traveling. We have seen it for Singapore. Once it opens, everyone goes out. We don’t even care about air ticket prices. They’ll come here and perform revenge traveling and revenge spending. This will help VivoCity, which contributes close to 22% of the NPI.

So if you combine this two major properties, that is a 43% contribution to NPI benefitted from the reopening.

Q. When it comes to MPACT, do you see any possible risks ahead that investors should be aware of?

Yes. Yes, there, there are risks. After the merger. There are two risks in this expect. One of them is a fundamental risk. So the fundamental side, if we have a slower than expected reopening of China and Hong Kong, or we are entering into a severe recession because now everybody is talking about recession. A severe recession will defnitely impact DPU. That is more on the fundamental side.

The other aspect is the political aspect because we know that now tension is pretty high between US and China on the Taiwan issue. So if any incident creates a war, maybe they just fire the missile out to each other. Right. Or they have a sanction on China or sanction on Hong Kong or whatever thing, definitely you affect the sentiment of the investment community.

Q: Do you think these latest acquisitions are a positive for ParkwayLife REIT’s portfolio? PLREIT has recently acquired 3 Hokkaido nursing homes.

Yes. positive because with the current high price to book value, about 1.94 times, and also the low DPU yield of about 3%, any acquisition out there would be quite attractive because definitely it’ll be much better than the current valuation and also the DPU.

This acquisition actually is yield-accretive. They are getting 6.5% NPI yield. And at the same time, the valuation of this property is 12% below the valuation compared to the REIT valuation itself, it is pretty attractive. There definitely be a retating after the portfolio to be integrated into the REIT.

And at the same time, a very low cost of debt. You just imagine that you are borrowing with an interest rate of close to 0%, and you are investing in some properties generating 6.5%. The spread is huge. It’s really a no brainer.

Q. Can you help us understand how PLREIT has been performing compared to pre-COVID levels?

Yeah, it, it really depends on each investor. When was their investment time? Five years ago. Definitely. This is one, this is one of the best REITs. But if its only for just after COVID or maybe one year ago, probably performance is not so fantastic but still quite good.

So I’m just referring to the, the, before the COVID and also based on the past five year, if you come just purely come back to the previous high of the pre COVID at the present stock price, it has already surpassed the previous pre-COVID high up by 25%. Other REITs do not have this kind of performance.

Yeah, because REITs at the present moment is coming down, and subjected to sector rotation. At the same time, the DPU has been growing steadily over year since the IPO and PLREIT is unscathed during the COVID period, they continue to pay good dividend, continue to grow that dividend, due to the strength in the underlying portfolio that’s why they’re able to combine such a high premium to the book value at the same time that did not go to the correction during this period.

Q. What is your feel of the recessionary headwind? And what could this mean for REITs?

Investors need to be selective in this case because during the recession period, most of the companiesthey’ll be going through cost cutting measures. First of all, they’ll try to reduce expense. Secondly, they start to cut headcounts. Thirdly, they may shut down the facilities. Tenant profile is important. If the tenant profiles are very strong, they’re quite reputable and they are in essential industries, definitely they can tide through this recession pretty well.

The Logistics and Industrial sector probably is more defensive at this time. Healthcare is also defensive. I think Singapore should be able to avoid the recession. So retail malls in Singapore, they’re probably more resilient in nature because we cannot live without retail malls.

Nowhere to go, nowhere to eat, nothing to do. If we are entering a recession, everyone will be tightening their belts. The hospitality sector will be impacted. Tourism will be affected. But at the same time, there is a revenge spending phenomena when China reopens, because everyone there have been locked down for three years. Right? You, you just imagine the potential explosion of the needs to spend and to travel that may maybe kick start and help us in the recovery of the global economy.

Navigating Volatile Markets to Beat Inflation (Physical Seminar 1st October 2022)

Worried about the high inflation rates? Join us as we share tips on how to beat inflation, and our inflation outlook for the rest of the year and beyond. You will learn ways to edit your investment portfolio to beat the high inflation rates, in a SAFE way.

As this is a physcial seminar, seats are limited so sign up today.

Date: 1st October 2022 (Saturday)

Time: 10am – 12pm

Venue: Gateway West (150 Beach Road, #12-01/08, Singapore 189720)

How to Build a REIT Portfolio into a Retirement Plan? (SGX Academy Webinar, 5th October 2022)

Want to learn the fundamentals of what REITs are, and how can this asset class complement your investment portfolio? Why should you invest in this asset class with an average p.a. yield of 5-7% and $100 minimum investment amount? Tune in to learn how to kickstart/improve your REITs investing!

Date: 5th October 2022 (Wednesday)

Time: 7pm – 830pm

Venue: Online

Listen to his previous market outlook interviews here:

2022

- Money & Me: Q3 2022 SREIT winners (August 2022)

- Money and Me: REIT picking in an inflationary environment (July 2022)

- Money and Me: Are Hospitality REITs the clear way to play the reopening trade in Singapore? (June 2022)

- Money and Me: Can S-REITs maintain its upswing from Q1? (May 2022)

- Money & Me: The case for being bullish on S-REITs amid the Ukraine crisis (March 2022)

- Money & Me: Optimism for S-REIT’s given earnings signals and mapping the possibilities for shareholders in the Mapletree merger (February 2022)

- Money & Me: Mapletree merger, growth in commercial S-Reits and the potential return of Reit IPOs in 2022 (January 2022)

2021

- Money & Me: First Reit, CapitaLand, Daiwa, Digital Core Reit and the best of the S-Reit pivots (December 2021)

- Money and Me: VTL’s and hospitality and retail, a new Reit ETF and Making sense of offers for SPH (November 2021)

- Money and Me: Who benefits from the ESR – ARA Logos Logistics Trust merger? (October 2021)

- Money and Me: China’s Evergrande Group property and the spillover in the property market, breaking down what CapitaLand Invest means for the investor and global REITs to watch (September 2021)

- Money and Me: Are retail and hospitality aggressive plays given the pace of reopening? (August 2021)

- Money and Me: Which REITs have seen a limited impact on occupancy during COVID? (July 2021)

- Money and Me: An overview of the REIT performance (June 2021)

- Money and Me: S-REIT’s: which are most likely and which least likely to be affected by new social restrictions? (May 2021)

- Money and Me: What’s the link between bond yields and S-REITs? (April 2021)

2020

- Money and Me: REITS that did well in 2020 (December 2020)

- Money and Me: An overview of S-REITS, value rotations and REITS paying out higher dividends (November 2020)

- Money and Me: Yield Generating Asset Classes (October 2020)

- Money and Me: The REIT outlook within and beyond Singapore (August 2020)

- Money and Me: Ugly Duckling Earnings turning into Beautiful S- Reit swans? (July 2020)

- Money and Me: V for S-REITs? (June 2020)

- Money and Me: Will revenge spending help REITs? (May 2020)

- Money and Me: What REITs to Look out for? (April 2020)

- Money and Me: Crazy REIT Sales (March 2020)

Kenny Loh is an Associate Wealth Advisory Director and REITs Specialist of Singapore’s top Independent Financial Advisor. He helps clients construct diversified portfolios consisting of different asset classes from REITs, Equities, Bonds, ETFs, Unit Trusts, Private Equity, Alternative Investments, Digital Assets and Fixed Maturity Funds to achieve an optimal risk adjusted return. Kenny is also a CERTIFIED FINANCIAL PLANNER, SGX Academy REIT Trainer, Certified IBF Trainer of Associate REIT Investment Advisor (ARIA) and also invited speaker of REITs Symposium and Invest Fair.

You can join my Telegram channel #REITirement – SREIT Singapore REIT Market Update and Retirement related news. https://t.me/REITirement

{kind=link}