Money and Me: REIT Opportunity & the Mid-Cap Alpha Hunt (April 2026)

Singapore REITs: Are They Unlocking Value or Diluting Your Returns?

The recent news of First REIT’s S$471.5 million divestment of its Indonesian healthcare assets has sparked a heated debate: Is this a smart strategic pivot, or are unitholders being left with a “watered-down” investment?

While divestments can feel like a retreat, they are often necessary recalibrations designed to protect long-term distributions from volatile currency swings and credit risks.

The “Why” Behind the Indonesia Exit

To understand the move, we have to look at the numbers that aren’t usually in the headlines:

- The Forex Trap: Over the last five years, while IDR-denominated revenue grew by 23%, the IDR plummeted approximately 28% against the SGD. This effectively wiped out operational gains, hurting both the DPU (Distribution Per Unit) and the Net Asset Value (NAV).

- Macro Headwinds: Concerns raised by international rating agencies like Fitch and Moody’s regarding the Indonesian investibility landscape made holding these assets a riskier bet for a Singapore-listed REIT.

The Case for “Unlocking Value”

First REIT isn’t just dumping assets; it’s selling from a position of strength:

- Selling at a Premium: The sale price is 2.1% higher than the latest valuation. This is a crucial “sanity check” for investors, proving that the REIT’s book value is backed by real-world demand.

- Immediate Rewards: The manager plans to distribute S$9.7 million of the proceeds as a special dividend—putting cash directly back into unitholders’ pockets.

- Building a “War Chest”: Post-divestment, leverage will plunge from 42.1% to a lean 16.7%. This saves S$18.8 million in annual interest costs and provides massive “dry powder” to hunt for new deals without needing to borrow in a high-interest-rate environment.

The “Dilution” Concern: What’s the Catch?

The strategy isn’t without its growing pains:

- The Yield Gap: Indonesian assets are high-yield because they are high-risk. Moving into stable, developed markets like Japan and Australia inevitably means lower immediate yields, which could lead to a temporary dip in DPU.

- Execution Risk: With a gearing of 16.7%, the REIT is currently “cash-rich but asset-light.” The burden is now on the manager to deploy that S$470 million quickly and wisely. If the cash sits idle for too long, it drags down overall returns.

Investor FAQ: Fact vs. Fiction

Q: Is First REIT becoming a “Zombie REIT” by selling its crown jewels? A: Far from it. This is about resilience over raw yield. The “crown jewels” in Indonesia came with heavy currency volatility and tenant concentration risk. By selling at a premium, the manager is “crystallizing” profits to pivot toward stable currencies. The key metric to watch now is the re-investment rate—how efficiently they can swap IDR risk for JPY or AUD stability.

Q: Is 16.7% gearing too conservative? Should they give more cash back? A: In a “higher-for-longer” rate environment, low gearing is a competitive superpower. It allows First REIT to pounce on distressed healthcare opportunities in full cash. Think of it as a war chest strategy rather than being overly cautious; it ensures they won’t have to go back to shareholders for more capital when the right deal comes along.

The Bottom Line:

First REIT is trading immediate high-risk yield for long-term balance sheet strength. For the patient investor, this “recalibration” may be the very thing that saves the portfolio from future currency shocks.

Mid-Cap Gems & Blue-Chip Moves: Where is the Alpha in S-REITs?

While the market giants offer a sense of security, the real excitement in the Singapore REIT (S-REIT) space is happening just beneath the surface. From the high-growth potential of mid-caps to strategic fund-raising by industry leaders, here is how to navigate the current landscape.

1. Unlocking Alpha: Why Mid-Caps are Outperforming the Giants

If the “Giant” REITs are for safety, the Mid-Caps (specifically those in the iEdge Next50 index) are where the growth—or “Alpha”—is currently hiding. According to recent DBS insights, the valuation gap has become too wide to ignore.

- The Growth Gap: Mid-cap REITs are projected to deliver a DPU growth rate of 4.2% (FY26-27). To put that in perspective, that is nearly 2.5x higher than the large-cap STI REITs.

- Deep Value: Mid-caps are trading at an average Price-to-NAV (P/NAV) of 0.8-0.9x, while large-caps sit at 1.1x. You are essentially buying these assets at a 10-20% discount, whereas you pay a premium for the “big boys.”

- Superior Yields: The yield play is clear. While large-caps offer between 4.5% and 6.5%, small and mid-cap REITs are dangling yields between 7% and 9.5%.

The “Catch”: Aren’t they riskier? Smaller REITs are often seen as more vulnerable to interest rate shocks. However, the valuation discount acts as a “margin of safety.” Furthermore, many mid-caps, have fortified their positions with high fixed-rate debt proportions (often above 75%), mirroring the stability of blue chips.

The Catalyst: The Equity Market Development Program (EQDP) This isn’t just about fundamentals; it’s about liquidity. The MAS/SGX EQDP is pushing institutional “passive” money into these mid-sized names. As they gain weight in indices like the iEdge Next50, fund managers are increasingly “forced” to buy, which could trigger a massive price re-rating.

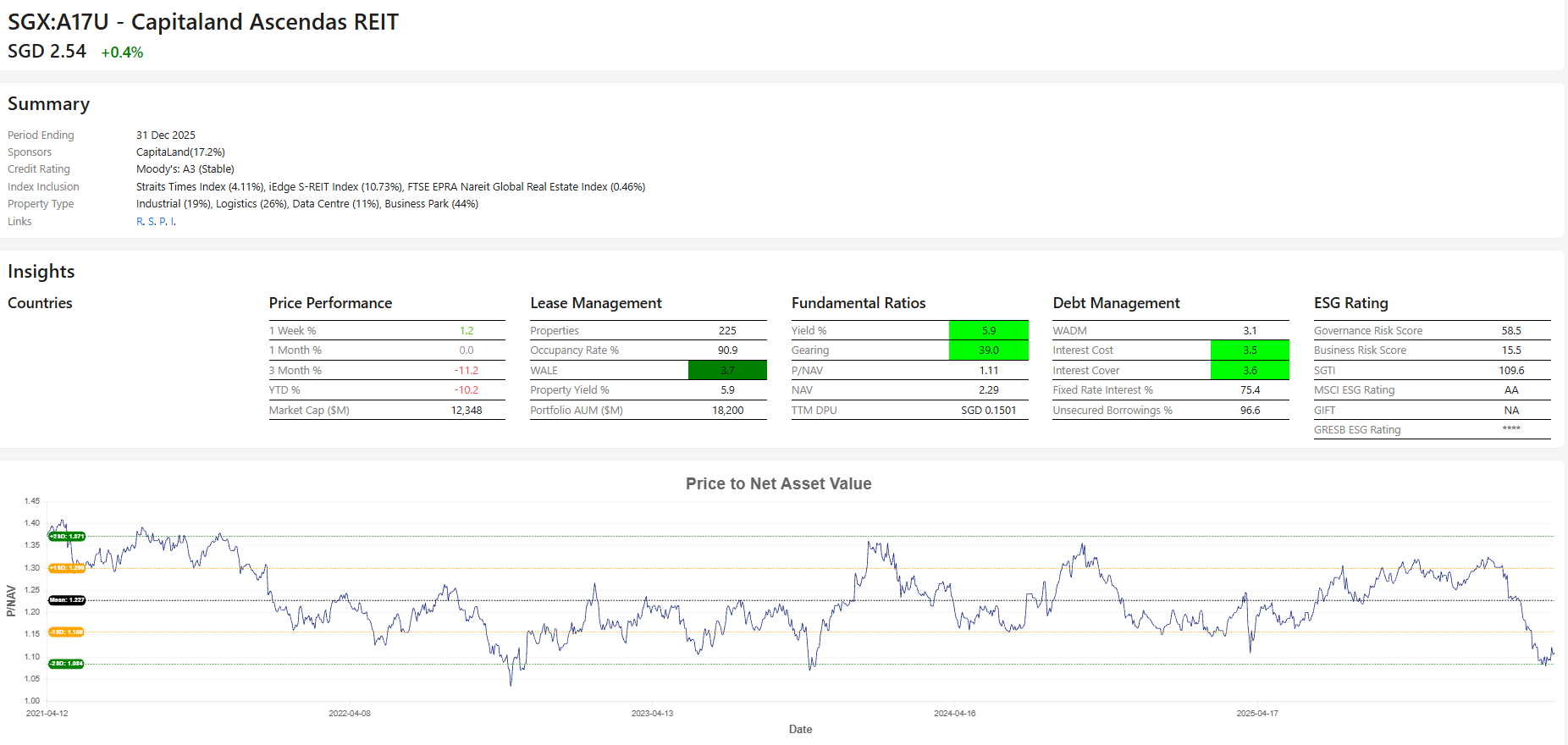

CapitaLand Ascendas REIT (CLAR): A Strategic “Buy the Dip”?

CapitaLand Ascendas REIT (CLAR) recently announced a S$900 million Equity Fund Raising (EFR). While “fund raising” often worries investors, this move is a classic blend of defense and offense.

The Deal at a Glance:

- The Offer: 28 new units for every 1,000 held.

- The Price: S$2.35. This represents a significant 7.5% discount to the last trading price of $2.54.

Why Unitholders Should Pay Attention:

- Valuation Sweet Spot: CLAR’s P/NAV is currently at 1.1x, which is two standard deviations below its 5-year average. With a current DPU yield of 5.9% (vs. the 5-year mean of 5.5%), the entry point is historically attractive.

Source: REITsavvy.com

- Technical Support: The stock is currently trading at a key technical support level, making the $2.35 offer price look even more robust.

- High-Quality Pivot: This isn’t “survival” money. The funds are being used to acquire New Economy assets: a Tier III Data Centre in Osaka, logistics in Loyang, and a stake in a Singapore Science Park office.

Strategic Tip: Use It or Lose It This preferential offering is non-renounceable. Unlike some rights issues, you cannot sell your entitlement on the open market. If you don’t subscribe, you simply get diluted by the institutional investors. If you have the cash, applying for excess units is a savvy move, as many retail investors will miss the deadline, leaving extra shares on the table.

Final Thought: Growth or Stability?

The S-REIT market is bifurcating. If you are hunting for capital appreciation and high yield, the Mid-Cap iEdge Next50 space is your hunting ground. If you prefer a blue-chip anchor for your portfolio, the CLAR Preferential Offering provides a rare opportunity to accumulate a market leader at a deep discount.

Reference News:

From divestments to fund raising – Are Singapore REITs unlocking value – or diluting returns?

https://www.businesstimes.com.sg/companies-markets/first-reit-proposes-s471-5-million-divestment-indonesia-assets

Singapore REITs: Unlocking alpha within the mid-cap S-REITs

CapitaLand Ascendas REIT Preferential Offering – What should unitholders do?https://growbeansprout.com/capitaland-ascendas-reit-preferential-offering-2026

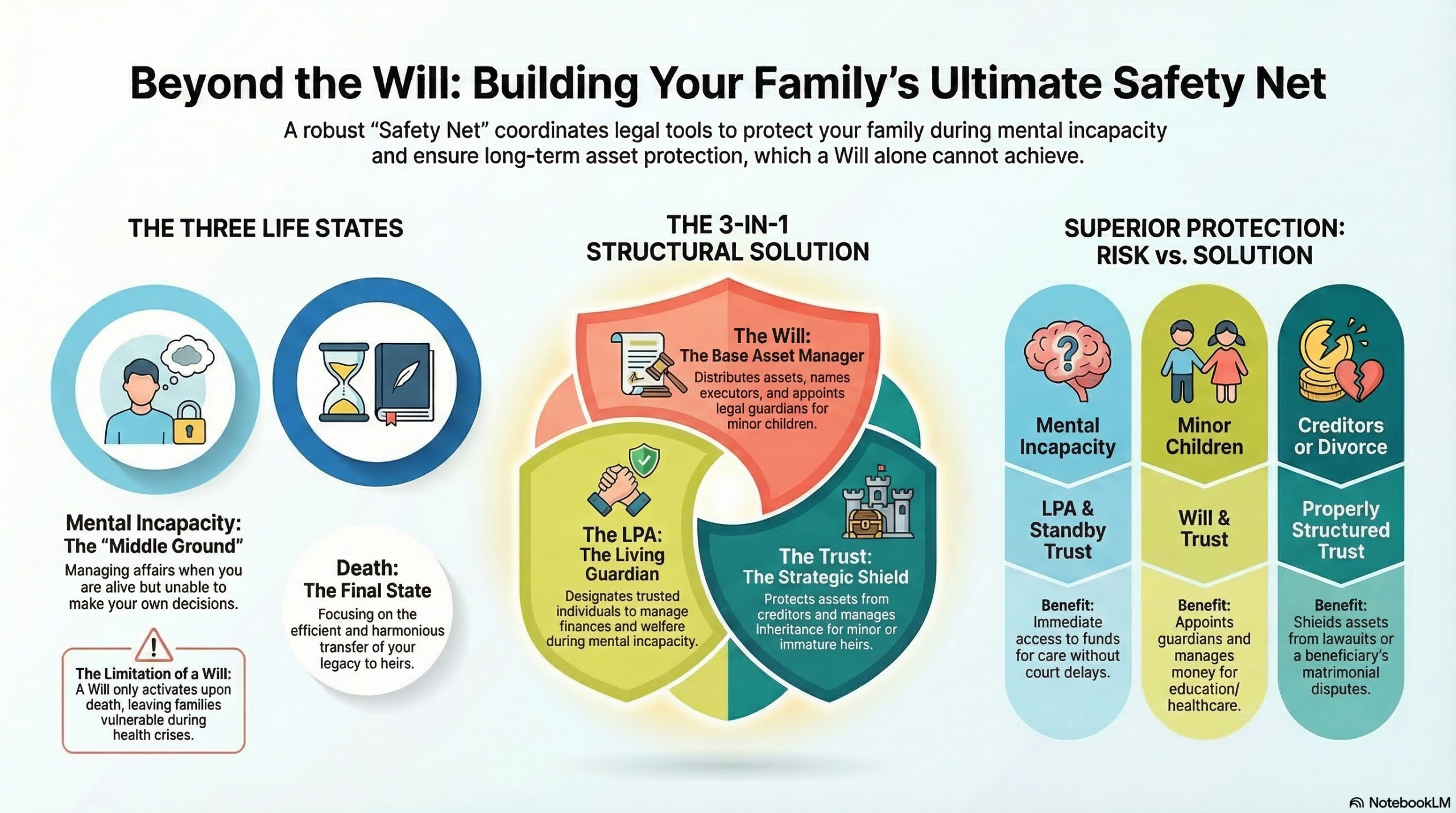

Kenny Loh is a distinguished Wealth Advisory Director (RNF# LKK300389588 Representing Financial Alliance) with a specialization in holistic investment planning and estate management. He excels in assisting clients to grow their investment capital and establish passive income streams for retirement. Kenny also facilitates tax-efficient portfolio transfers to beneficiaries, ensuring tax-efficient capital appreciation through risk mitigation approaches and optimized wealth transfer through strategic asset structuring.

In addition to his advisory role, Kenny is an esteemed SGX Academy trainer specializing in S-REIT investing and regularly shares his insights on MoneyFM 89.3. He holds the titles of Certified Estate & Legacy Planning Consultant and CERTIFIED FINANCIAL PLANNER (CFP).

With over a decade of experience in holistic estate planning, Kenny employs a unique “3-in-1 Will, LPA, and Standby Trust” solution to address clients’ social considerations, legal obligations, emotional needs, and family harmony. He holds double master’s degrees in Business Administration and Electrical Engineering, and is an Associate Estate Planning Practitioner (AEPP), a designation jointly awarded by The Society of Will Writers & Estate Planning Practitioners (SWWEPP) of the United Kingdom and Estate Planning Practitioner Limited (EPPL), the accreditation body for Asia.

Arrange for a non-obligatory one-to-one free consultation here!

You can join his Telegram channel #REITirement – SREIT Singapore REIT Market Update and Retirement related news. https://t.me/REITirement

If you need any financial advice, please contact kennyloh@fapl.sg

2026

2025

- Money and Me: Are S-REITs Still Worth the Climb? (October 2025)

- Money and Me: S-REITs vs Banks – Is It Time to Rotate? (August 2025)

- Money and Me: Are S-REITs Still Worth the Risk in 2025? (July 2025)

- Money and Me: REITs Among Upcoming IPO’s and what you need to know (June 2025)

- Money and Me: S-REITs Bounce Back? China’s REIT Game-Changer and the hunt for yield of up to 8% (May 2025)

- Money and Me: How are S-REIT’s doing amidst the Tariffs Turnaround? (April 2025)

- 𝗠𝗼𝗻𝗲𝘆 𝗮𝗻𝗱 𝗠𝗲: 𝗦-𝗥𝗘𝗜𝗧𝘀 𝗥𝗮𝗹𝗹𝘆, 𝗧𝗿𝗲𝗮𝘀𝘂𝗿𝘆 𝗬𝗶𝗲𝗹𝗱𝘀 𝗗𝗿𝗼𝗽, 𝗮𝗻𝗱 𝗖𝗗𝗟’𝘀 𝗙𝗮𝗺𝗶𝗹𝘆 𝗗𝗿𝗮𝗺𝗮 (March 2025)

- Money and Me: CPF Special Account Closure, Retirement Planning, and Investment Strategies with Kenny Loh (February 2025)

- Money and Me: What is your T-Bill to S-REIT allocation? (January 2025)

2024

- Money and Me: Trump’s Second Term, Bitcoin, Tesla, AI, and Suntec REIT Mandatory Cash Offer (December 2024)

- Money and Me: Data Centered S-REITs; here is what you need to know (November 2024)

- Money and Me: Finding attractive S-REITs in a rate cutting environment (October 2024)

- Money and Me: What’s behind the S-REIT Rally? Fed Rate Cuts, and should Finfluencers be managed? (September 2024)

- Money and Me: Navigating S-REITs Amid Earnings Season and Potential US Rate Cuts (August 2024)

- Money and Me: Navigating Challenges for Mapletree REITs and REITs related to Changi Business Park

(June 2024) - Money and Me: Winners and Losers Among S-REITs, Frasers Property’s Profit Plunge, and the Impact of Sustained High Interest Rates (May 2024)

- Money and Me: Manulife US REIT where could it be heading? Are we at the tail end of the down cycle for S-Reits? (April 2024)

- Money and Me: Will more S-REIT’s suspend distributions? (March 2024)

- Money and Me: US Office Reits – the immediate outlook is bleak but there are opportunities for investors (February 2024)

- Money and Me: Why S-REIT investors are focused on valuations in 2024? (January 2024)

2023

- Money and Me: Can Manulife US REIT be saved? (December 2023)

- Money and Me: Finding bargains in the S-REITs sector today (November 2023)

- Money and Me: How a contrarian investor reads a sell-off (October 2023)

- Money and Me: Finding bargains in the S-REITs sector today (September 2023)

- Money and Me: S-REITs earning stars and landscape quakes (August 2023)

- Money and Me: 3 Singapore REITs to watch (July 2023)

- Money and Me: Are S-REITs in for a promising 2H2023? (June 2023)

- Money and Me: How might the expectations of an impending recession affect S-REITs? (May 2023)

- Money and Me: S-REITs’ 2023 1st quarter report card review (April 2023)

- Money and Me: S-REITs that will hold up well in an increasing interest rate environment (March 2023)

- Money and Me: Winners and losers of latest S-REITs earnings season (February 2023)

- Money and Me: S-REITs’ 2023 outlook (January 2023)

2022

- Money & Me: Is 2023 the year of recovery for S-REITs? (December 2022)

- Money & Me: What happens after the recent S-REIT crash? (November 2022)

- Money & Me: Further Interest Rate Hikes, FHT’s failed Privatization bid (September 2022)

- Money & Me: Q3 2022 SREIT winners (August 2022)

- Money and Me: REIT picking in an inflationary environment (July 2022)

- Money and Me: Are Hospitality REITs the clear way to play the reopening trade in Singapore? (June 2022)

- Money and Me: Can S-REITs maintain its upswing from Q1? (May 2022)

- Money & Me: The case for being bullish on S-REITs amid the Ukraine crisis (March 2022)

- Money & Me: Optimism for S-REIT’s given earnings signals and mapping the possibilities for shareholders in the Mapletree merger (February 2022)

- Money & Me: Mapletree merger, growth in commercial S-Reits and the potential return of Reit IPOs in 2022 (January 2022)

2021

- Money & Me: First Reit, CapitaLand, Daiwa, Digital Core Reit and the best of the S-Reit pivots (December 2021)

- Money and Me: VTL’s and hospitality and retail, a new Reit ETF and Making sense of offers for SPH (November 2021)

- Money and Me: Who benefits from the ESR – ARA Logos Logistics Trust merger? (October 2021)

- Money and Me: China’s Evergrande Group property and the spillover in the property market, breaking down what CapitaLand Invest means for the investor and global REITs to watch (September 2021)

- Money and Me: Are retail and hospitality aggressive plays given the pace of reopening? (August 2021)

- Money and Me: Which REITs have seen a limited impact on occupancy during COVID? (July 2021)

- Money and Me: An overview of the REIT performance (June 2021)

- Money and Me: S-REIT’s: which are most likely and which least likely to be affected by new social restrictions? (May 2021)

- Money and Me: What’s the link between bond yields and S-REITs? (April 2021)

2020

- Money and Me: REITS that did well in 2020 (December 2020)

- Money and Me: An overview of S-REITS, value rotations and REITS paying out higher dividends (November 2020)

- Money and Me: Yield Generating Asset Classes (October 2020)

- Money and Me: The REIT outlook within and beyond Singapore (August 2020)

- Money and Me: Ugly Duckling Earnings turning into Beautiful S- Reit swans? (July 2020)

- Money and Me: V for S-REITs? (June 2020)

- Money and Me: Will revenge spending help REITs? (May 2020)

- Money and Me: What REITs to Look out for? (April 2020)

- Money and Me: Crazy REIT Sales (March 2020)