Money and Me: Are Hospitality REITs the clear way to play the reopening trade in Singapore?

Michelle Martin finds out if there is reason for cautious optimism in the S-REIT space given last month’s data on the sector. We survey the possible winners with impressive Price/NAV ratios and discuss if Industrial REITs could be a contrarian bet in this conversation with Kenny Loh, REITs Specialist and Independent Financial Advisor.

Timestamps

0:18 Intro

1:40 How is the Retail Sector doing?

2:22 Which REITs are looking like clear winners?

3:31 How will Rising Inflation Rates Impact REITs? How will different sectors be impacted differently?

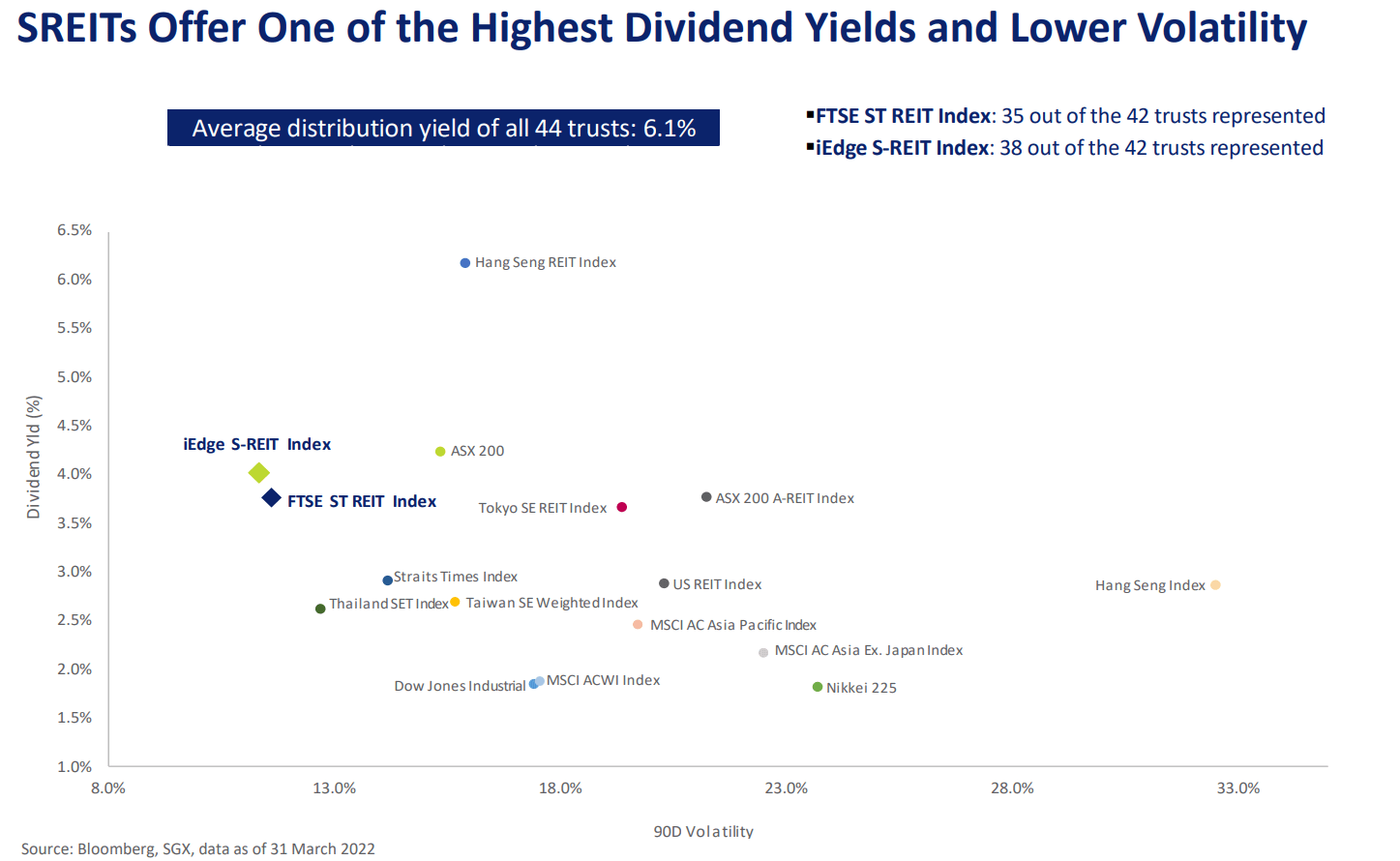

5:45 Do you see any particularly attractive sectors?

7:12 Thoughts on Mapletree Investment Trust’s recent divestment of a Data Centre

7:57 Near-term challenges for S-REITs

9:21 Listener Question: Investing in REIT ETFs vs in REITs (Pros and Cons)

12:22 Outro

Listen to his previous market outlook interviews here:

Kenny Loh is an Associate Wealth Advisory Director and REITs Specialist of Singapore’s top Independent Financial Advisor. He helps clients construct diversified portfolios consisting of different asset classes from REITs, Equities, Bonds, ETFs, Unit Trusts, Private Equity, Alternative Investments, Digital Assets and Fixed Maturity Funds to achieve an optimal risk adjusted return. Kenny is also a CERTIFIED FINANCIAL PLANNER, SGX Academy REIT Trainer, Certified IBF Trainer of Associate REIT Investment Advisor (ARIA) and also invited speaker of REITs Symposium and Invest Fair.

Technical Analysis of FTSE ST REIT Index (FSTAS351020)

FTSE ST Real Estate Investment Trusts (FTSE ST REIT Index) decreased from 853.56 to 820.69(-3.85%)compared to last month’s update. FTSE REIT Index is currently trading within the 800-822 range.

The following is the compilation of 39 Singapore REITs with colour-coding of the Distribution Yield, Gearing Ratio and Price to NAV Ratio.

The Financial Ratios are based on past data and there are lagging indicators.

This REIT table takes into account the dividend cuts due to the COVID-19 outbreak. Yield is calculated trailing twelve months (ttm), therefore REITs with delayed payouts might have lower displayed yields, thus yield displayed might be lower for more affected REITs.

All REITs are updated with the latest Q1 2022 business updates/earnings.

Digital Core REIT’s yield is extracted from the IPO Prospectus, calculated based on *Estimated DPU (calculated from the Prospectus) / Current Price.

ESR REIT and ARA LOGOS Logistics Trust has merged to form ESR-LOGOS REIT. ALOG REIT is no longer shown, shown values are for ESR REIT.

FY DPU: If Green, FY DPU for the recent 4 Quarters is higher than that of the preceding 4 Quarters.If Lower, it isRed.

Most REITs are green since it is compared to FY20/21 as the base (during the pandemic)

Yield (ttm): Yield, calculated by DPU (trailing twelve months) and Current Price as of June 3rd, 2022

Digital Core REIT: Yield calculated from IPO Prospectus.

Gearing (%): Leverage Ratio.

Price/NAV: Price to Book Value. Formula: Current Price (as of June 3rd, 2022) over Net Asset Value per Unit.

Yield Spread (%): REIT yield (ttm) reference to Gov Bond Yields. REITs trading in USD is referenced to US Gov Bond Yield, everything else is referenced to SG Gov Bond Yield.

Price/NAV Ratios Overview

Price/NAV decreased to 0.95.

Decreased from 0.99 from May 2022.

Singapore Overall REIT sector is undervalued now.

Take note that NAV is adjusted upwards for some REITs due to pandemic recovery.

Most overvalued REITs (based on Price/NAV)

Parkway Life REIT (Price/NAV = 2.08)

Keppel DC REIT (Price/NAV = 1.54)

Mapletree Industrial Trust (Price/NAV = 1.34)

Ascendas REIT (Price/NAV = 1.17)

Mapletree Logistics Trust (Price/NAV = 1.12)

Elite Commercial REIT (Price/NAV = 1.11)

No change to the Top 3 compared to the March to May updates.

Most undervalued REITs (based on Price/NAV)

BHG Retail REIT (Price/NAV = 0.58)

Lippo Malls Indonesia Retail Trust (Price/NAV = 0.58)

EC World REIT (Price/NAV = 0.67)

OUE Commercial REIT (Price/NAV = 0.69)

ARA Hospitality Trust (Price/NAV = 0.70)

Starhill Global REIT (Price/NAV = 0.74)

No change to the Top 3 compared to the May updates.

Distribution Yields Overview

TTM Distribution Yield increased to 6.30%

Increased from 6.00% in May 2022.

14 of 40 Singapore REITs have distribution yields of above 7%. (Same as last month’s update)

Do take note that these yield numbers are based on current prices taking into account the delayed distribution/dividend cuts due to COVID-19, and economic recovery.

Highest Distribution Yield REITs (ttm)

United Hampshire REIT (10.08%)

EC World REIT (9.86%)

Prime US REIT (9.48%)

First REIT (9.19%)

Keppel Pacific Oak REIT (9.06%)

Manulife US REIT (8.81%)

Reminder that these yield numbers are based on current prices taking into account delayed distribution/dividend cuts due to COVID-19.

Some REITs opted for semi-annual reporting and thus no quarterly DPU was announced.

A High Yield should not be the sole ratio to look for when choosing a REIT to invest in.

Yield Spread increased to 3.47%.

Increased from 3.44% in May 2022.

Gearing Ratios Overview

Gearing Ratio decreased to 36.83%.

Decreased from 37.05% in May 2022.

Gearing Ratios are updated quarterly. Therefore all REITs have Q1 2022 updates which have updated gearing ratios.

In general, Singapore REITs sector gearing ratio is healthy but increased due to the reduction of the valuation of portfolios and an increase in borrowing due to Covid-19.

Highest Gearing Ratio REITs

ARA Hospitality Trust (44.9%)

Suntec REIT (43.3%)

Lippo Malls Indonesia Retail Trust (42.9%)

Manulife US REIT (42.8%)

Elite Commercial REIT (42.8%)

Frasers Hospitality Trust (42.3%)

No change to the Top 3 compared to the April and May update.

Market Capitalisation Overview

Total Singapore REIT Market Capitalisation decreased by 2.75% to S$109.16 Billion.

Decreased from S$112.25 Billion in May 2022.

Biggest Market Capitalisation REITs:

Capitaland Integrated Commercial Trust ($14.65B)

Ascendas REIT ($11.71B)

Mapletree Logistics Trust ($7.95B)

Mapletree Industrial Trust ($6.67B)

Mapletree Commercial Trust ($5.96B)

Frasers Logistics & Commercial Trust ($4.94B)

No change in Top 5 rankings since August 2021.

Smallest Market Capitalisation REITs:

BHG Retail REIT ($272M)

ARA US Hospitality Trust ($383M)

Lippo Malls Indonesia Retail Trust ($408M)

United Hampshire REIT ($466M)

Sabana REIT ($492M)

EC World REIT ($502M)

No change in Top 4 rankings compared to March to May updates.

Disclaimer: The above table is best used for “screening and shortlisting only”. It is NOT for investing (Buy / Sell) decision. If you want to know more about investing in REITs, here’s a subsidised 2-day course with all you need to know about REITs and how to start investing in them.

S-REITs Earnings Season for the Period Ending 31 Mar 2022 has wrapped up

A total of 39 S-REITs have released their earnings/business updates for the Period Ending 31 Mar 2022 (28 Feb 2022 for SPH Reit).

MCT, MNACT shareholders approved merger

THE BUSINESS TIMES: Unit holders of Mapletree Commercial Trust (MCT) and Mapletree North Asia Commercial Trust (MNACT) have voted in favour of a merger to create one of Asia’s 10 largest real estate investment trusts (Reits).

The merged entity, to be named Mapletree Pan Asia Commercial Trust (MPACT), will have a theoretical market capitalisation of approximately $10.5 billion – ranking it among the top three Reits listed in Singapore, behind CapitaLand Integrated Commercial Trust and Ascendas Reit.

At separate extraordinary general meetings (EGMs) on Monday (May 23), all resolutions to pave the way for the merger were duly passed. At MCT’s EGM in the morning, some 91.7 per cent of MCT unit. Read More

ESR-LOGOS REIT starts trading

ESR-Logos Reit : J91U +1.22% ended its first day of trading on Thursday (May 5) on the Singapore Exchange at S$0.395, unchanged from its opening price.

The units were trading 1.3 per cent or S$0.005 higher than the last closing price of the counter, when it was previously known as ESR-Reit, with 476,000 units changing hands at the open. ESR-Reit had closed flat on Wednesday at S$0.39, on an ex-distribution basis.

On Thursday, the counter hit an intra-day high of S$0.40 at 9.09am, before easing to trade at an intra-day low of S$0.39 at 2.39pm. It ended the day at S$0.395, down S$0.005 or 1.3 per cent, with some 8.7 million units changing hands.

E-Log Reit was formed after a merger between ESR-Reit and Ara Logos Logistics Trust (ALog Trust), following the merger between the 2 Reits’ sponsors – ESR Cayman and ARA Asset Management. Read More

Summary

Fundamentally, the whole Singapore REITs landscape is undervalued based on the average Price/NAV value of the S-REITs. Below is the market cap heat map for the past 1 month. Generally, S-REITs in the past month have decreased in market cap.

Only 6 REITs increased in Market Cap the past month. They are ESR-LOGOS REIT (6.41%), Lendlease REIT (5.11%), ParkwayLife REIT (3.77%), Sabana REIT (1.11%), Keppel DC REIT (0.99%) and Mapletree NAC Trust (0.83%). Both ESR-LOGOS REIT and Mapletree NAC Trust’s growth can be attributed to their respective mergers, the enlarged ESR-LOGOS REIT started trading on 5th May, and for MNACT, the merger with MCT has been approved by shareholders.

Yield spread (in reference to the 10 year Singapore government bond of 2.82% as of 3rd June 2022) loosened slightly from 3.44% to 3.47%.The S-REIT Average Yield increased from 6.00% to 6.30%, but the increase in the Government Bond Yields offsets this Average S-REIT Yield increase. The yield of the REITs sector needs to increase to maintain the average yield spread of 4%. Amid all the negative news, S-REITs have been resilient and have one of the highest risk-adjusted dividend yields compared to other stock exchanges.

The risk premium has dropped, but still remains attractive (compared to other asset classes) to accumulate Singapore REITs in stages to lock in the current price and to benefit from long-term yield after the recovery, especially since the S-REIT Market is still at a fair value. Moving forward, it is expected that DPU will continue to increase due to the recovery of the global economy, as seen in the previous few earning updates, especially for Hospitality REITs. NAV is expected to be adjusted upward due to revaluation of the portfolio.

Upcoming Events

You may follow my coming REITs webinar and market updates:

Listen as I speak with Michelle Martin and discuss about the REIT space in Singapore, and the REIT Market Outlook. Simply tune in at 10am.

*For New Investors / those looking to invest in REITs*

Free Webinar: How to build your REIT portfolio into your retirement plan

June 13th 2022, 7pm

Participants will have insight on the characteristics of REITs as an Asset Class, and able to explore the benefits and suitability of REITs in building their retirement portfolio.

Participants will appreciate the important factors to consider when building their retirement portfolio to minimise their investment risks.

Participants will be guided to construct a diversified portfolio to attain their retirement objective.

Singapore REITs enjoyed a good first half of 2022. Can it continue?

US Fed will continue tightening monetary policy and is likely to raise interest rates by 0.5 percentage points in at least two more FOMC meetings. Will this be good or bad for REITs?

What should you do if you’re holding REITs or looking to buy now?

What are the ‘4 pains’ every REITs investor suffers from and how can you overcome them?

Note: This above analysis is for my own personal research and it is NOT a buy or sell recommendation. Investors who would like to leverage my extensive research and years of Singapore REIT investing experience can approach me separately for a REIT Portfolio Consultation.

Kenny Loh is an Associate Wealth Advisory Director and REITs Specialist of Singapore’s top Independent Financial Advisor. He helps clients construct diversified portfolios consisting of different asset classes from REITs, Equities, Bonds, ETFs, Unit Trusts, Private Equity, Alternative Investments, Digital Assets and Fixed Maturity Funds to achieve an optimal risk adjusted return. Kenny is also a CERTIFIED FINANCIAL PLANNER, SGX Academy REIT Trainer, Certified IBF Trainer of Associate REIT Investment Advisor (ARIA) and also invited speaker of REITs Symposium and Invest Fair. You can join my Telegram channel #REITirement – SREIT Singapore REIT Market Update and Retirement related news. https://t.me/REITirement

Based on the latest update, Gateway Plaza has -24% average rental reversion whereas The Pinnacle Gangnam has +44% average rental reversion. What are the reasons for such performance, are there structural changes on the underlying environment? Would this trend continue into the next few quarters, and how does it affect the DPU?

Gateway Plaza

In Beijing1, new supply in the central business district (“CBD”) with more affordable rental rates as well as relocations of tenants to decentralised office areas (such as Wangjing) to achieve cost savings, have resulted in rental declines in office districts such as Lufthansa. Gateway Plaza is an office building located in Lufthansa, a well-established commercial hub in Beijing.

The MNACT Manager had, and continues to prioritise high occupancy level at Gateway Plaza, to minimise downtime and ensure cash flow stability. As a result, occupancy rate improved from 92.9% as at 31 March 2021 to 94.3% as at 31 March 2022. However, rental rates were lower and an average rental reversion of negative 24% was recorded for FY21/22.

Looking ahead1, rents for Beijing office districts, such as Lufthansa, which are nearer to the CBD, are expected to remain stable in the near-term. Based on market views, rents are likely to rise in late 2022 or early 2023.

In line with Beijing’s opening up of the services industry, tenants from these business services segments, in addition to the technology, media and telecommunications, as well as financial services and media sectors, are expected to form the bulk of leasing demand at Lufthansa and benefit Gateway Plaza1. In the second half of FY21/22, Gateway Plaza has also attracted new tenants from the environmental consulting and waste recycling sectors.

Occupancy rate at Gateway Plaza is expected to remain high, with active marketing and leasing of office space.

The Pinnacle Gangnam

South Korea’s Grade A office market1 has shown strong growth in 2021 despite the uncertainty caused by COVID-19, and benefits from attractive market dynamics including built-in rental escalations. Vacancy rates decreased in all major districts, including the strong performing submarket of Gangnam Business District (“GBD”), supported by high-growth tech companies that are still performing well despite COVID-191.

The Pinnacle Gangnam is an office building located in GBD, Seoul. Consequently, The Pinnacle Gangnam has achieved a positive rental reversion of 44% in FY21/22, coupled with a high occupancy rate of 97.3% as at 31 March 2022.

For the Seoul office market2, with limited supply, on-going demand for office spaces due to the expansion of technology and pharmaceutical companies is expected to persist for the next few years. The Pinnacle Gangnam is in a good position to benefit from the strong leasing demand from these high-growth sectors, and to deliver organic growth through the high proportion of leases with built-in rental escalation during the lease term.

Notes:

Source: Colliers International (Hong Kong) Limited, 30 March 2022 (link)

Source: Colliers, Seoul Quarterly, 21 January 2022 (link)

Update on China, Japan and Korea Properties (FY21/22 Results: Presentation)

Is there any Plan B (if the Merger does not go through) for MNACT?

Should the Merger not go through, MNACT will return to business as usual, remaining focused on safeguarding the long-term value for unitholders through proactive asset management, effective cost control and prudent capital management. At the same time, we will continue to source for yield accretive acquisitions to achieve greater diversification and growth of MNACT. MNACT has demonstrated its capabilities in driving inorganic growth through acquisitions of high quality properties spanning across multiple North Asian markets; including expanding beyond its IPO geographies and successfully acquiring nine office properties in Greater Tokyo (2018, 2020 and 2021) and one office property in Seoul (2020).

MNACT will return to business as usual, remaining focused on safeguarding the long-term value for unitholders through proactive asset management, effective cost control and prudent capital management.

The Merger, on the other hand, will harness and combine the respective strengths of both REITs to create a more resilient and diversified platform. Over the years, we have been focused on growing and enhancing the resilience of MNACT’s portfolio through accretive acquisitions that provide both geographical and income diversification. The Merged Entity, MPACT, will have an even higher financial capability and flexibility to pursue value-creating acquisitions and fast-track its growth trajectory. We remain confident in the merits of the Merger and the exciting future ahead.

Enlarged Portfolio of post-merger Mapletree Pan Asia Commercial Trust

What are your priorities for the next 1-2 year post Merger? How do you split the work with Ms Sharon Lim?

As announced on 21 March 2022, it is intended that Ms. Lim Hwee Li Sharon who currently holds the positions of Chief Executive Officer and Executive Director in the MCT Manager, will retain these positions in the manager of the Merged Entity following the completion of the Merger. On or about the completion of the Merger, it is intended that the MNACT Manager will retire as the manager of MNACT and the MCT Manager will be appointed as the manager of the Merged Entity.

Following the Merger, the MCT Manager intends to implement its proactive and tailored “4R” asset and capital management strategy to realise the benefits from the Merger. For more details on the “4R” asset and capital management strategy, you may refer to Paragraph 4.2 in Appendix B – Offeror’s Letter to MNACT Unitholders of the Scheme Document (link).

Kenny Loh is an Associate Wealth Advisory Director and REITs Specialist of Singapore’s top Independent Financial Advisor. He helps clients construct diversified portfolios consisting of different asset classes from REITs, Equities, Bonds, ETFs, Unit Trusts, Private Equity, Alternative Investments, Digital Assets and Fixed Maturity Funds to achieve an optimal risk adjusted return. Kenny is also a CERTIFIED FINANCIAL PLANNER, SGX Academy REIT Trainer, Certified IBF Trainer of Associate REIT Investment Advisor (ARIA) and also invited speaker of REITs Symposium and Invest Fair. You can join my Telegram channel #REITirement – SREIT Singapore REIT Market Update and Retirement related news. https://t.me/REITirement

{kind=link}