The market landscape in April 2026 has shifted. Between geopolitical tensions in the Middle East and a “higher-for-longer” interest rate environment, retail investors are facing a critical turning point. Is your passive income safe, or are you holding a “Yield Trap”?

In this recorded webinar with Tiger Brokers, Kenny Loh (Founder of REITsavvy and SGX Academy Trainer) breaks down the “Yield Defense” strategy. Learn how to move past headline yields and identify REITs with the pricing power to survive and thrive in 2026.

Key Takeaways

✅ Pricing Power: Why Suburban Retail and Data Centres are outrunning inflation.

✅ Debt Management: How to check if a REIT can afford its interest payments.

✅ Yield Spread: Calculating the “Margin of Safety” against 10-year SGS yields.

About Kenny Loh

Kenny Loh is the Founder of REITsavvy.com and REIT Specialist of SGX Academy S-REITs Trainer. With over 20 years of experience, he helps retail investors build resilient, income-generating portfolios using a data-driven approach.

SPECIAL PROMOTION BY TIGER BROKERS (Valid for 30 days only)

Tiger Brokers has deposit rewards ready today — pick your gift directly, no luck needed!

🟢Deposit USD 2,000+, choose any one of four exclusive items!

🟢Deposit USD 10,000+, get the coffee mug and colour-changing umbrella, plus a USD 30 trading voucher after 60 days!

🟢Deposit USD 100,000+, all previous tiers stack up, vouchers up to USD 150!

🟢Deposit USD 300,000+, the grand prize Million Milestone Dream Edition is yours outright — plus Tiger Coins, vouchers, and every tier’s merchandise!

🟢And there’s more — Total Assets Rewards stack on top, claim both!

🟢USD 30,000+ total assets: Elite Membership upgrade, 6,000 Tiger Coins, full professional privileges!

🟢USD 500,000+ total assets: dedicated VIP manager, 10,000 Tiger Coins, and premium exclusive benefits!

👉 Join me on Tiger Trade! Sign up with my invite and we both get USD 300*! You’ll also unlock up to SGD 1,000 in welcome perks. https://tigr.link/s/80FVmEQ

Kenny Loh is a distinguished Wealth Advisory Director (RNF# LKK300389588 Representing Financial Alliance) with a specialization in holistic investment planning and estate management. He excels in assisting clients to grow their investment capital and establish passive income streams for retirement. Kenny also facilitates tax-efficient portfolio transfers to beneficiaries, ensuring tax-efficient capital appreciation through risk mitigation approaches and optimized wealth transfer through strategic asset structuring.

In addition to his advisory role, Kenny is an esteemed SGX Academy trainer specializing in S-REIT investing and regularly shares his insights on MoneyFM 89.3. He holds the titles of Certified Estate & Legacy Planning Consultant and CERTIFIED FINANCIAL PLANNER (CFP).

With over a decade of experience in holistic estate planning, Kenny employs a unique “3-in-1 Will, LPA, and Standby Trust” solution to address clients’ social considerations, legal obligations, emotional needs, and family harmony. He holds double master’s degrees in Business Administration and Electrical Engineering, and is an Associate Estate Planning Practitioner (AEPP), a designation jointly awarded by The Society of Will Writers & Estate Planning Practitioners (SWWEPP) of the United Kingdom and Estate Planning Practitioner Limited (EPPL), the accreditation body for Asia.

Arrange for a non-obligatory one-to-one free consultation here!

Singapore REITs: Are They Unlocking Value or Diluting Your Returns?

The recent news of First REIT’s S$471.5 million divestment of its Indonesian healthcare assets has sparked a heated debate: Is this a smart strategic pivot, or are unitholders being left with a “watered-down” investment?

While divestments can feel like a retreat, they are often necessary recalibrations designed to protect long-term distributions from volatile currency swings and credit risks.

The “Why” Behind the Indonesia Exit

To understand the move, we have to look at the numbers that aren’t usually in the headlines:

The Forex Trap: Over the last five years, while IDR-denominated revenue grew by 23%, the IDR plummeted approximately 28% against the SGD. This effectively wiped out operational gains, hurting both the DPU (Distribution Per Unit) and the Net Asset Value (NAV).

Macro Headwinds: Concerns raised by international rating agencies like Fitch and Moody’s regarding the Indonesian investibility landscape made holding these assets a riskier bet for a Singapore-listed REIT.

The Case for “Unlocking Value”

First REIT isn’t just dumping assets; it’s selling from a position of strength:

Selling at a Premium: The sale price is 2.1% higher than the latest valuation. This is a crucial “sanity check” for investors, proving that the REIT’s book value is backed by real-world demand.

Immediate Rewards: The manager plans to distribute S$9.7 million of the proceeds as a special dividend—putting cash directly back into unitholders’ pockets.

Building a “War Chest”: Post-divestment, leverage will plunge from 42.1% to a lean 16.7%. This saves S$18.8 million in annual interest costs and provides massive “dry powder” to hunt for new deals without needing to borrow in a high-interest-rate environment.

The “Dilution” Concern: What’s the Catch?

The strategy isn’t without its growing pains:

The Yield Gap: Indonesian assets are high-yield because they are high-risk. Moving into stable, developed markets like Japan and Australia inevitably means lower immediate yields, which could lead to a temporary dip in DPU.

Execution Risk: With a gearing of 16.7%, the REIT is currently “cash-rich but asset-light.” The burden is now on the manager to deploy that S$470 million quickly and wisely. If the cash sits idle for too long, it drags down overall returns.

Investor FAQ: Fact vs. Fiction

Q: Is First REIT becoming a “Zombie REIT” by selling its crown jewels?A: Far from it. This is about resilience over raw yield. The “crown jewels” in Indonesia came with heavy currency volatility and tenant concentration risk. By selling at a premium, the manager is “crystallizing” profits to pivot toward stable currencies. The key metric to watch now is the re-investment rate—how efficiently they can swap IDR risk for JPY or AUD stability.

Q: Is 16.7% gearing too conservative? Should they give more cash back?A: In a “higher-for-longer” rate environment, low gearing is a competitive superpower. It allows First REIT to pounce on distressed healthcare opportunities in full cash. Think of it as a war chest strategy rather than being overly cautious; it ensures they won’t have to go back to shareholders for more capital when the right deal comes along.

The Bottom Line:

First REIT is trading immediate high-risk yield for long-term balance sheet strength. For the patient investor, this “recalibration” may be the very thing that saves the portfolio from future currency shocks.

Mid-Cap Gems & Blue-Chip Moves: Where is the Alpha in S-REITs?

While the market giants offer a sense of security, the real excitement in the Singapore REIT (S-REIT) space is happening just beneath the surface. From the high-growth potential of mid-caps to strategic fund-raising by industry leaders, here is how to navigate the current landscape.

1. Unlocking Alpha: Why Mid-Caps are Outperforming the Giants

If the “Giant” REITs are for safety, the Mid-Caps (specifically those in the iEdge Next50 index) are where the growth—or “Alpha”—is currently hiding. According to recent DBS insights, the valuation gap has become too wide to ignore.

The Growth Gap: Mid-cap REITs are projected to deliver a DPU growth rate of 4.2% (FY26-27). To put that in perspective, that is nearly 2.5x higher than the large-cap STI REITs.

Deep Value: Mid-caps are trading at an average Price-to-NAV (P/NAV) of 0.8-0.9x, while large-caps sit at 1.1x. You are essentially buying these assets at a 10-20% discount, whereas you pay a premium for the “big boys.”

Superior Yields: The yield play is clear. While large-caps offer between 4.5% and 6.5%, small and mid-cap REITs are dangling yields between 7% and 9.5%.

The “Catch”: Aren’t they riskier? Smaller REITs are often seen as more vulnerable to interest rate shocks. However, the valuation discount acts as a “margin of safety.” Furthermore, many mid-caps, have fortified their positions with high fixed-rate debt proportions (often above 75%), mirroring the stability of blue chips.

The Catalyst: The Equity Market Development Program (EQDP) This isn’t just about fundamentals; it’s about liquidity. The MAS/SGX EQDP is pushing institutional “passive” money into these mid-sized names. As they gain weight in indices like the iEdge Next50, fund managers are increasingly “forced” to buy, which could trigger a massive price re-rating.

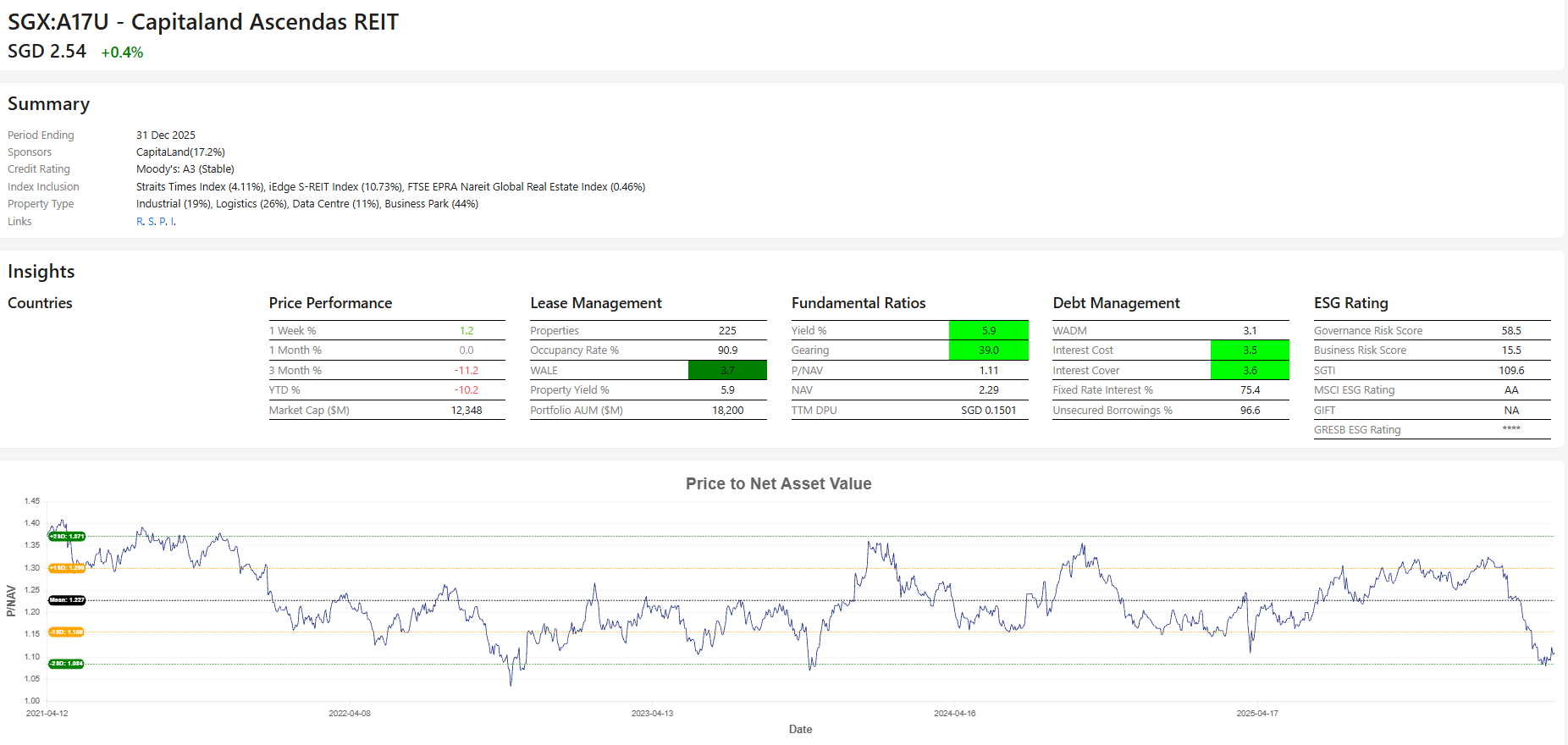

CapitaLand Ascendas REIT (CLAR): A Strategic “Buy the Dip”?

CapitaLand Ascendas REIT (CLAR) recently announced a S$900 million Equity Fund Raising (EFR). While “fund raising” often worries investors, this move is a classic blend of defense and offense.

The Deal at a Glance:

The Offer: 28 new units for every 1,000 held.

The Price:S$2.35. This represents a significant 7.5% discount to the last trading price of $2.54.

Why Unitholders Should Pay Attention:

Valuation Sweet Spot: CLAR’s P/NAV is currently at 1.1x, which is two standard deviations below its 5-year average. With a current DPU yield of 5.9% (vs. the 5-year mean of 5.5%), the entry point is historically attractive.

Source: REITsavvy.com

Technical Support: The stock is currently trading at a key technical support level, making the $2.35 offer price look even more robust.

High-Quality Pivot: This isn’t “survival” money. The funds are being used to acquire New Economy assets: a Tier III Data Centre in Osaka, logistics in Loyang, and a stake in a Singapore Science Park office.

Strategic Tip: Use It or Lose It This preferential offering is non-renounceable. Unlike some rights issues, you cannot sell your entitlement on the open market. If you don’t subscribe, you simply get diluted by the institutional investors. If you have the cash, applying for excess units is a savvy move, as many retail investors will miss the deadline, leaving extra shares on the table.

Final Thought: Growth or Stability?

The S-REIT market is bifurcating. If you are hunting for capital appreciation and high yield, the Mid-Cap iEdge Next50 space is your hunting ground. If you prefer a blue-chip anchor for your portfolio, the CLAR Preferential Offering provides a rare opportunity to accumulate a market leader at a deep discount.

Kenny Loh is a distinguished Wealth Advisory Director (RNF# LKK300389588 Representing Financial Alliance) with a specialization in holistic investment planning and estate management. He excels in assisting clients to grow their investment capital and establish passive income streams for retirement. Kenny also facilitates tax-efficient portfolio transfers to beneficiaries, ensuring tax-efficient capital appreciation through risk mitigation approaches and optimized wealth transfer through strategic asset structuring.

In addition to his advisory role, Kenny is an esteemed SGX Academy trainer specializing in S-REIT investing and regularly shares his insights on MoneyFM 89.3. He holds the titles of Certified Estate & Legacy Planning Consultant and CERTIFIED FINANCIAL PLANNER (CFP).

With over a decade of experience in holistic estate planning, Kenny employs a unique “3-in-1 Will, LPA, and Standby Trust” solution to address clients’ social considerations, legal obligations, emotional needs, and family harmony. He holds double master’s degrees in Business Administration and Electrical Engineering, and is an Associate Estate Planning Practitioner (AEPP), a designation jointly awarded by The Society of Will Writers & Estate Planning Practitioners (SWWEPP) of the United Kingdom and Estate Planning Practitioner Limited (EPPL), the accreditation body for Asia.

Arrange for a non-obligatory one-to-one free consultation here!

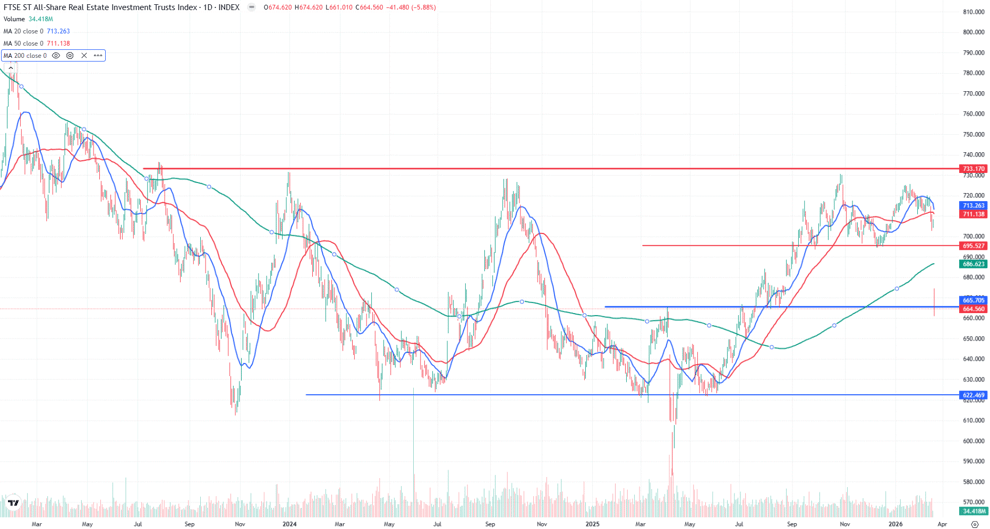

Technical Analysis of FTSE ST REIT Index (FSTAS351020)

FTSE ST Real Estate Investment Trusts (FTSE ST REIT Index) declined sharply from 721.34 to 664.56 (-7.87%) compared to the previous update, marking a decisive breakdown below the previous support at ~695.

Over this period, the index has transitioned from consolidation into a clear downside impulse within 2 days, with price slicing through prior 695 support that had held multiple times since Sep 2025, likely due to the volatility brought about from the Iran war.

On the downside, the next key support lies around 622, which previously acted as a base during earlier cycles. If selling momentum persists, these levels are likely to be tested.

On the upside, any rebound is expected to face strong resistance at ~695, followed by ~725, where prior consolidation and supply zones exist. A recovery back above 695 (previous support) is needed to stabilize price action.

Overall, the index has entered a short-term bearish trend with strong momentum, and the medium-term outlook has shifted to bearish bias following the breakdown of key support. The long-term structure is now at risk of rolling over if lower support levels fail to hold.

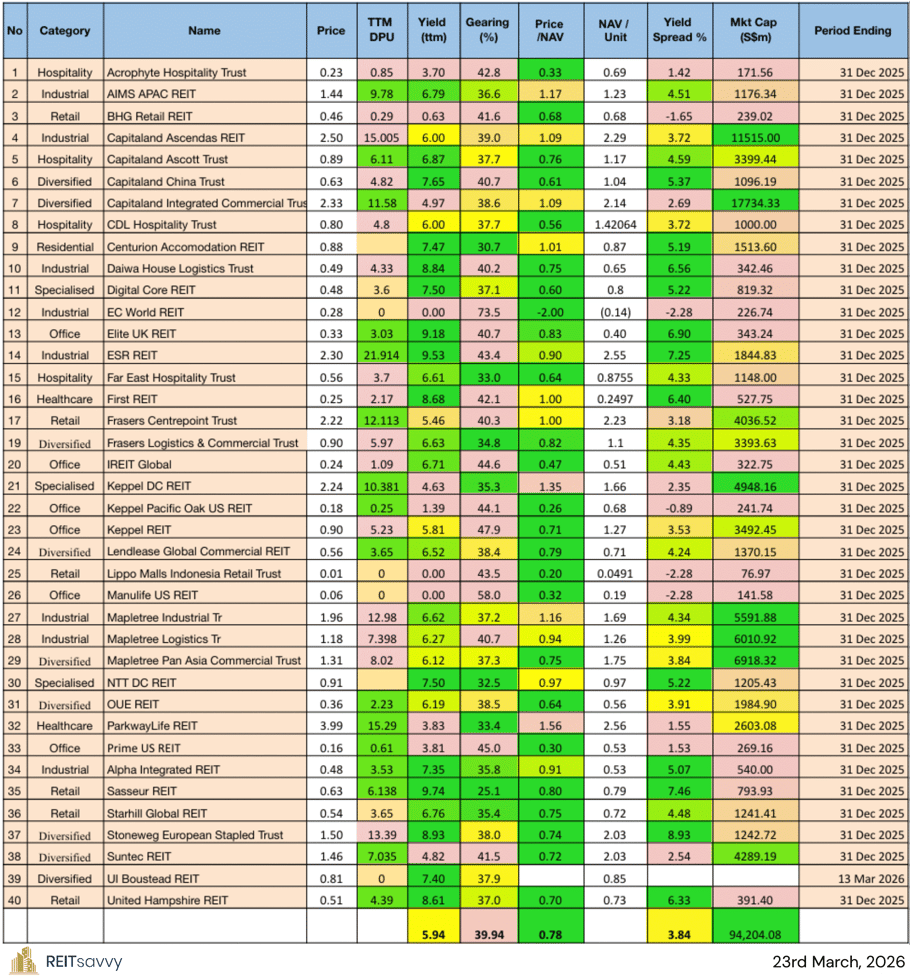

The following is the compilation of 40 Singapore REITs with colour-coding of the Distribution Yield, Gearing Ratio and Price to NAV Ratio.

The Financial Ratios are based on past data and these are lagging indicators.

All REITs have the latest Q3 2025 values, except Centurion Accommodation REIT where their values are based on their IPO Prospectuses.

I have introduced weighted average (weighted by market cap) to the financial ratios, in addition to the existing simple average ratios. This is another perspective where smaller market cap REITs do not disproportionately affect the average ratios. As of May 2025, I have removed EC World REIT from these calculations.

I have included Centurion Accommodation REIT in this latest update, using values from the IPO Prospectus.

FY DPU: If Green, FY DPU for the recent 4 Quarters is higher than that of the preceding 4 Quarters. If Lower, it is Red.

Yield (ttm): Yield, calculated by DPU (trailing twelve months) and Current Price as of March 23rd, 2026.

Gearing (%): Leverage Ratio.

Price/NAV: Price to Book Value. Formula: Current Price over Net Asset Value per Unit.

Yield Spread (%): REIT yield (ttm) reference to Gov Bond Yields. REITs are referenced to SG Gov Bond Yield.

As of May 2024, all REITs’ Yield Spread will be referenced to SG Gov Bond Yields, regardless of trading currency.

Price/NAV Ratios Overview

Price/NAV decreased to 0.78(Weighted Average: 0.93)

Decreased from 0.86 from January 2026. (Weighted Average was 1.02)

Singapore Overall REIT sector is slightly undervalued (or at fair value if weighted)

Most overvalued REITs (based on Price/NAV)

ParkwayLife REIT

1.56

Keppel DC REIT

1.35

AIMS APAC REIT

1.17

Mapletree Industrial Tr

1.16

Capitaland Ascendas REIT

1.09

Capitaland Integrated Commercial Trust

1.09

EC World REIT is currently suspended and has a N.M P/NAV value.

Most undervalued REITs (based on Price/NAV)

Lippo Malls Indonesia Retail Trust

0.20

Keppel Pacific Oak US REIT

0.26

Prime US REIT

0.30

Manulife US REIT

0.32

Acrophyte Hospitality Trust

0.33

IREIT Global

0.47

Distribution Yields Overview

TTM Distribution Yield increased to 5.94%. (Weighted Average increased to 5.62%)

Increased from 5.41% in January 2026. (Weighted Average was 5.17%)

13 of 40 Singapore REITs have ttm distribution yields of above 7%.

Highest Distribution Yield REITs (ttm)

Sasseur REIT

9.74

ESR REIT

9.53

Elite UK REIT

9.18

Stoneweg European Stapled Trust

8.93

Daiwa House Logistics Trust

8.84

First REIT

8.68

Reminder that these yield numbers are based on current prices.

Some REITs opted for semi-annual reporting and thus no quarterly DPU was announced.

A High Yield should not be the sole ratio to look for when choosing a REIT to invest in.

Yield Spreadincreased to 3.84%. (Weighted Average is 3.75%)

Increased from 3.42% in January 2026. (Weighted Average was 3.86%)

From May 2024 onwards, all my yield spread measurements are now in relation to SG Gov Bond Yields, no longer a mix with US Gov Bond Yields.

Gearing Ratios Overview

Gearing Ratio remained similar at 39.94%. (Weighted Average: 37.61%)

Remained similar at 39.94% in January 2026. (Weighted Average: 37.5%)

Gearing Ratios are updated quarterly. Therefore, no values changed and all values are based on the most recent Q2 2025 updates.

S-REITs Gearing Ratio has been on a steady uptrend. It was 35.55% in Q4 2019.

Highest Gearing Ratio REITs

EC World REIT

73.5

Manulife US REIT

58.0

Keppel REIT

47.9

Prime US REIT

45.0

IREIT Global

44.6

Keppel Pacific Oak US REIT

44.1

MUST and EC World REIT’s gearing ratio has exceeded MAS’s gearing limit of 50%. However, the aggregate leverage limit is not considered to be breached if exceeding the limit is due to circumstances beyond the control of the REIT Manager.

Market Capitalisation Overview

Total Singapore REIT Market Capitalisation decreased by 6.8% to S$94.20 Billion.

Decreased from S$101.07 Billion in January 2026.

Biggest Market Capitalisation REITs (S$m):

Capitaland Integrated Commercial Trust

17734.33

Capitaland Ascendas REIT

11515.00

Mapletree Pan Asia Commercial Trust

6918.32

Mapletree Logistics Tr

6010.92

Mapletree Industrial Tr

5591.88

Keppel DC REIT

4948.16

Smallest Market Capitalisation REITs (S$m):

Lippo Malls Indonesia Retail Trust

76.97

Manulife US REIT

140.40

Acrophyte Hospitality Trust

170.13

EC World REIT

226.74

BHG Retail REIT

239.02

Keppel Pacific Oak US REIT

239.72

Disclaimer: The above table is best used for “screening and shortlisting only”. It is NOT for investing (Buy / Sell) decision. If you want to know more about investing in REITs, scroll down for more information on the REITs courses.

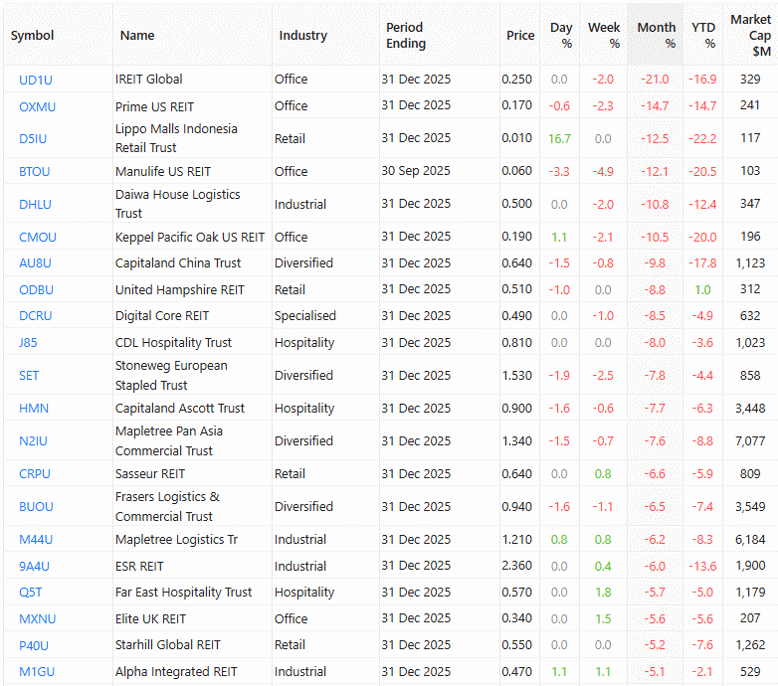

Top 20 Best/Worst Performers of February/March 2026

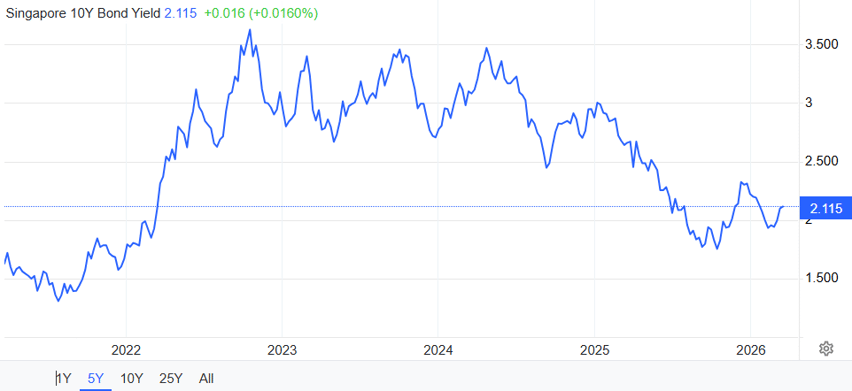

SG 10 Year Government Bond Yield

SG 10 Year: 2.12% (decreased from 2.20%)

Summary

The Singapore REIT sector has reversed its recent recovery, with the FTSE ST All-Share REIT Index declining from 721.34 to 664.56 (-7.87%)over the past two months, with most of the losses occurring in the past week, from 700 to 664.56. The index has broken decisively below the 695–700 support range, which had previously underpinned the recovery, signaling a clear deterioration in market structure.

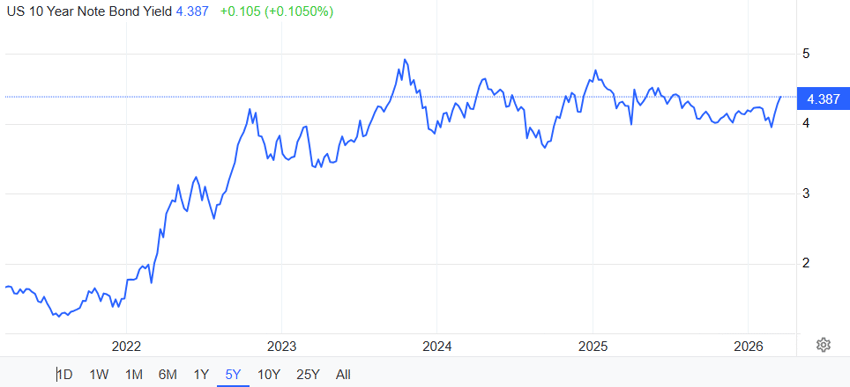

On the macro front, interest rate dynamics have turned less supportive at the margin. The US 10-year Treasury yield has risen to ~4.38%, breaking above recent consolidation levels (highest since mid-2025 levels) and indicating renewed upward pressure on global rates. This move represents a key headwind for REIT valuations, particularly after a period of relative stability.

In contrast, the Singapore 10-year government bond yield remains subdued at ~2.1–2.2%, suggesting that domestic financing conditions are still relatively stable. However, the divergence between US and Singapore yields may limit the extent of local rate relief, especially given the global nature of capital flows.

Valuations remain attractive, with many REITs still trading below NAV, particularly within industrial, retail, and selected hospitality segments. Sector yields in the mid-5% to 6% range continue to offer a reasonable premium over risk-free rates. Yield spreads have tightened modestly as prices recovered, but remain supportive on a historical basis.

US 10 Year Risk Free Rate

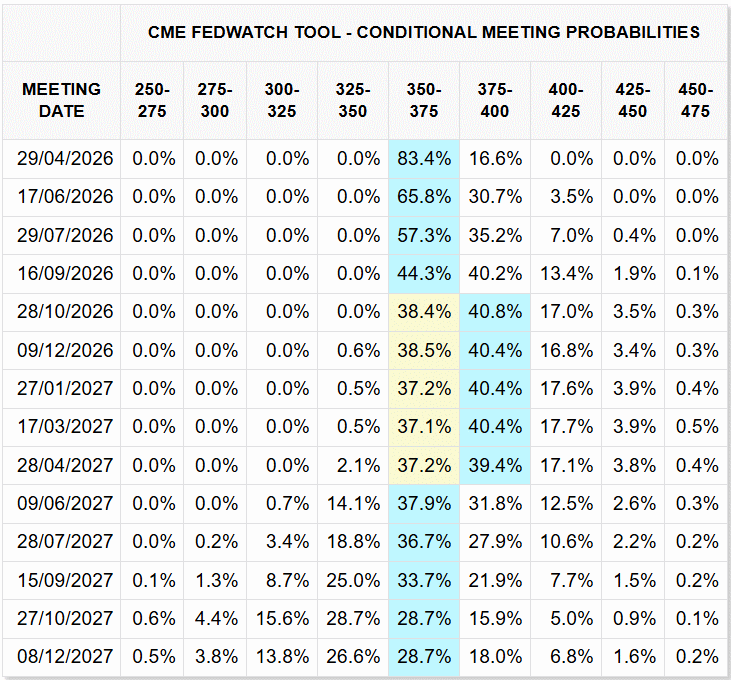

According to the CME FedWatch tool, markets continue to price a delayed and gradual easing cycle, with the highest probabilities centered around the 350–400 bps range through 2026, and only a slow progression towards lower rates into 2027. This reinforces the view that near-term rate relief is limited, and higher-for-longer conditions may persist.

Valuations have become more compelling following the recent correction, with many REITs trading at wider discounts to NAV. Sector yields have likely expanded back towards the mid-6% range, improving the relative attractiveness of income spreads versus risk-free rates.

However, the increase in bond yields partially offsets this benefit, and investor sensitivity to interest rate movements remains elevated. As such, valuation support alone may not be sufficient to drive a near-term rebound without stabilization in rates.

Kenny Loh is a distinguished Wealth Advisory Director (RNF# LKK300389588 Representing Financial Alliance) with a specialization in holistic investment planning and estate management. He excels in assisting clients to grow their investment capital and establish passive income streams for retirement. Kenny also facilitates tax-efficient portfolio transfers to beneficiaries, ensuring tax-efficient capital appreciation through risk mitigation approaches and optimized wealth transfer through strategic asset structuring.

In addition to his advisory role, Kenny is an esteemed SGX Academy trainer specializing in S-REIT investing and regularly shares his insights on MoneyFM 89.3. He holds the titles of Certified Estate & Legacy Planning Consultant and CERTIFIED FINANCIAL PLANNER (CFP).

With over a decade of experience in holistic estate planning, Kenny employs a unique “3-in-1 Will, LPA, and Standby Trust” solution to address clients’ social considerations, legal obligations, emotional needs, and family harmony. He holds double master’s degrees in Business Administration and Electrical Engineering, and is an Associate Estate Planning Practitioner (AEPP), a designation jointly awarded by The Society of Will Writers & Estate Planning Practitioners (SWWEPP) of the United Kingdom and Estate Planning Practitioner Limited (EPPL), the accreditation body for Asia.

Arrange for a non-obligatory one-to-one free consultation here!